Photo: Hdclipartall.com

January 20, 2023

- Markets skittish on Fed outlook.

- Canada retail sales expected to have fallen 0.5% m/m in November.

- US dollar closing week on a mixed note since Monday-CAD and JPY lose ground.

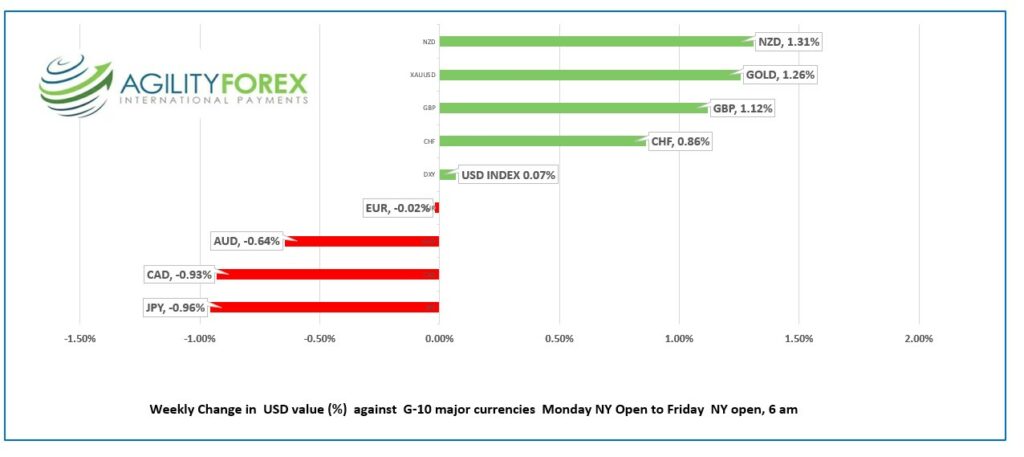

FX at a glance -Change since Monday open

Source: IFXA Ltd/RP

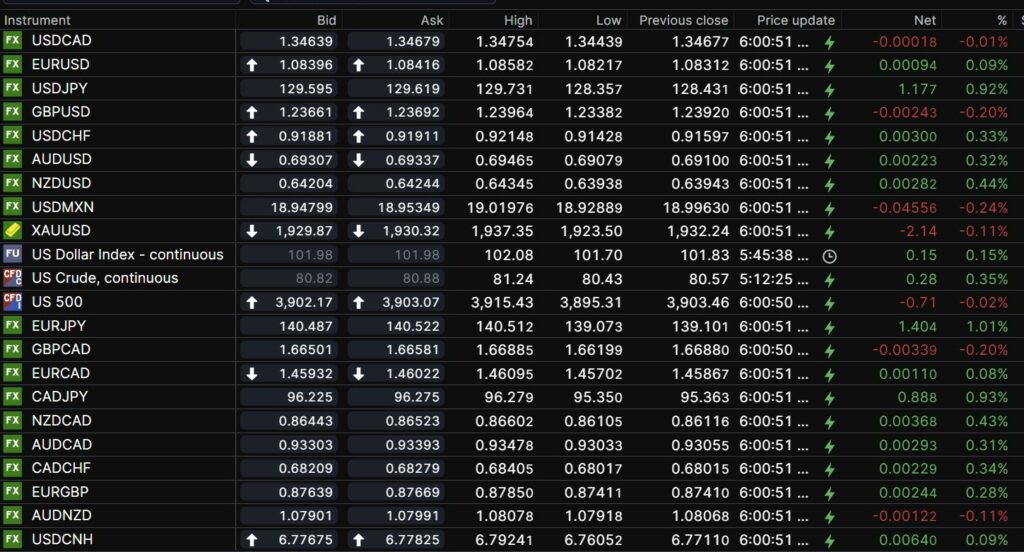

USDCAD Snapshot: open 1.3463-67, overnight range 1.3444-1.3475, close 1.3468

USDCAD rallied Wednesday, rising from 1.3353, coinciding with the S&P 500 index trading at 4014.16. When risk sentiment soured yesterday, the S&P 500 index fell to 3885.54 and USDCAD rallied to 1.3518.

S&P 500 futures are unchanged (as of 6:30 am) and USDCAD trading right where it closed. Traders do not know what to think, so are content to await more concrete signals from south of the border.

Oil prices recouped yesterday’s losses and WTI climbed from $80.43/barrel to $81.24/b in early NY trading. Traders are optimistic for increased demand from China which offset the EIA report that crude inventories rose 8.4 million barrels last week.

Canada retail sales fell 0.1%m/m in November, far better than the -0.5% decline that was expected but the results had zero impact on USDCAD trading. Traders are focused on external events while awaiting the BoC decision next Wednesday.

USDCAD Technical Outlook

The intraday USDCAD are modestly bullish while trading above 1.3450, looking for a move above 1.3520 to target 1.3560. A drop below 1.3440 suggests further downside to 1.3410 and 1.3380.

Longer term, the USDCAD uptrend line from June, which comes into play at 1.3310 is poised to converge with the downtrend line from October 10 which is sitting at 1.3630. A break either side of these levels leads to 1.3000 or 1.4500.

For today, USDCAD support is at 1.3440 and 1.3410. Resistance is at 1.3520 and 1.3560.

Today’s range 1.3440-1.3520

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Global markets are in flux. Bond traders are betting that Fed funds top out at 5.0% while FOMC officials deliver a contrarian view. Vice Chair Brainard said “Even with the recent moderation, inflation remains high, and policy will need to be sufficiently restrictive for some time to make sure inflation returns to 2% on a sustained basis.”

Her colleague, NY Fed President John Williams, parroted her comments saying ““With inflation still high and indications of continued supply-demand imbalances, it is clear that monetary policy still has more work to do to bring inflation down to our 2% goal on a sustained basis.”

But just in case you thought interest rates were the only issue, the deputy chair of Russia’s Security Council Dmitry Medvedev, put a nuclear war on the table. He is apparently irked at G-7 nations planning to send advanced weapons to Ukraine saying, “The defeat of a nuclear power in a conventional war may trigger a nuclear war.”

The seemingly annual/semi-annual US Debt Ceiling of the Absurd theatrics are another reason traders prefer to sit on the sidelines. The fear is that the US would default, and although it has never happened, the quality and calibre of the 2023 Congress certainly raises the risk.

Even so, global markets were ambivalent, at best. Asian equity indexes closed with gains across the board and European bourses are trading modestly higher in early NY trading. SP 500 futures are flat.

EURUSD see-sawed in a 1.0822-1.0858 range with prices underpinned by yesterday’s hawkish comments by ECB officials. The ECB remains on track for50 bp rate hikes in February and March.

GBPUSD traded in a 1.2336-96 range. Sentiment is positive due to the improving EU/UK dialogue over Northern Ireland border issues. GBPUSD shrugged off weak retail sales data.

USDJPY rallied from 128.36 to 129.99. Prices remain bid due to the BoJ pushback against speculation the YCC cap would increase to 0.75%. However, gains are limited after inflation rose to 4.0% y/y in December, higher than expected.

AUDUSD traded in a 0.6394-0.6435 range with price action tracking US dollar sentiment.

There are no US economic releases of note today.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

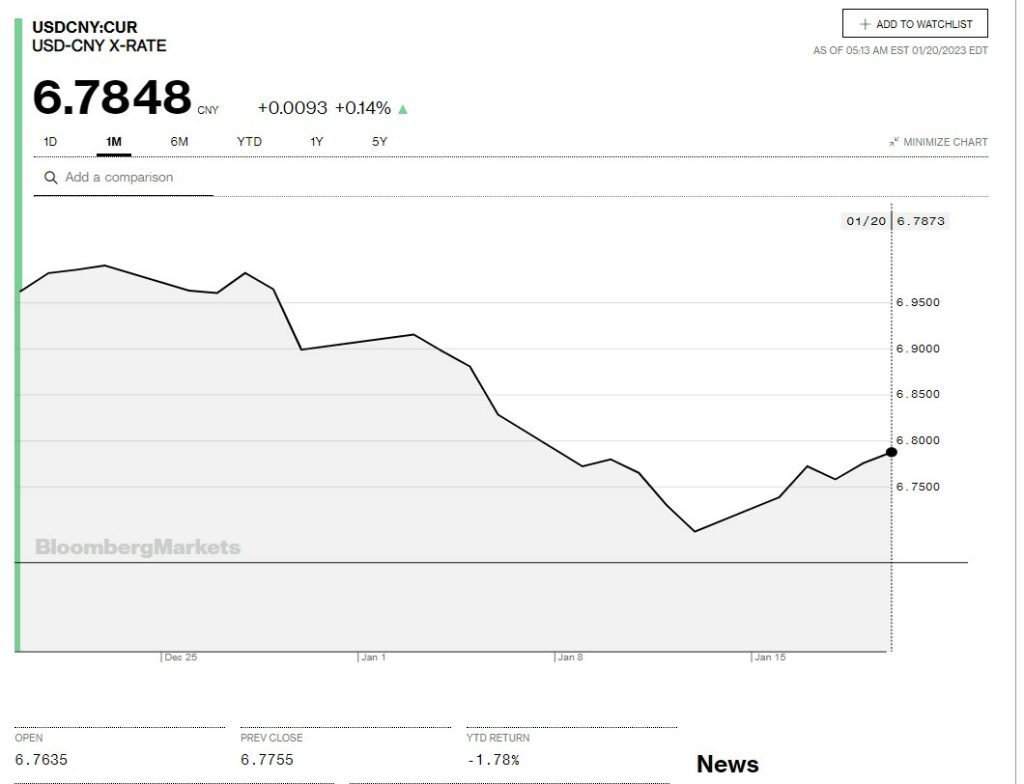

China Snapshot

Today’s Bank of China Fix: 6.7702, previous 6.7674

Shanghai Shenzhen CSI 300 rose 0.61% to 4181.53.

PboC leaves rates unchanged as expected. 1-Year Loan Prime Rate 3.65% and 5-Year Loan Prime Rate 4.30%.

Lunar New Year begins Sunday January 22. Mainland stock markets will be closed for the week.

Chart: USDCNY one month

Source: Bloomberg