Photo: Bing AI

October 24, 2023

- Treasury yields consolidating yesterday’s losses.

- Light US data calendar leaves bond traders to drive FX direction.

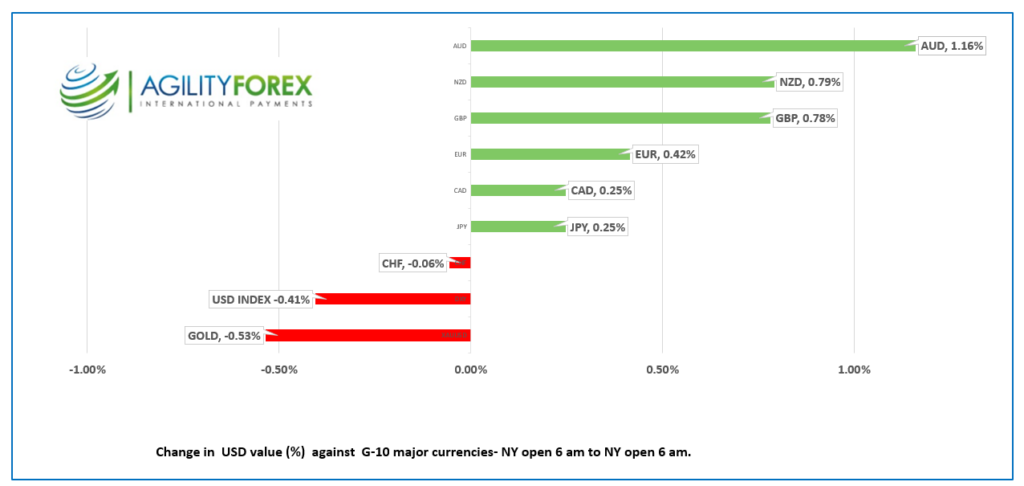

- US dollar opens with losses across the board-AUD outperforms.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3685-89, overnight range 1.3661-1.3700, close 1.3691

USDCAD came under pressure yesterday on the heels of broad US dollar weakness triggered when treasury yields went into free fall. Bill Ackman, CEO of Pershing Square Capital is credited with causing the turmoil when he said he closed his short bond position because there was too much risk in the world and that the US economy is weaker than it appears.

Oil prices failed to benefit from the softer US dollar. Instead, WTI dropped from $88.02 yesterday to $85.06/ today in a relief retreat because Israel has delayed its ground assault into Gaza. Traders are hoping that the delay reduces the risk of Middle East crude supplies being disrupted.

USDCAD traders are patiently awaiting the results of tomorrows Bank of Canada meeting.

USDCAD Technicals

The USDCAD technicals are bullish inside a 1.3550-1.3750 range that has contained price action since October 6.The uptrend from October 12 is intact above 1.3660 with a move above 1.3710 putting 1.3750 in play. A break below 1.3660 targets 1.3605, then 1.3550.

For today, USDCAD support is at 1.3660 and 1.3630. Resistance is at 1.3710 and 1.3750. Todays Range 1.3660-1.3750.

Chart: USDCAD 4 hour

Source: Daily FX

G-10 FX recap

Monday was a slow news day for financial markets until bond traders decided that a 5.0% 10-year Treasury yield was overdone and in need of a correction. It happened quickly, and the yield dropped to 4.838% by the close.

FX traders scrambled to cut US dollar long positions, and the US dollar index (DXY) plunged from 106.14 to 105.16 overnight before it rebounded to 105.62 in NY.

Wall Street closed on a mixed note. The S&P 500 and Dow Jones Industrial Average fell, while the Nasdaq rose. Asian equity indexes closed with modest gains. Japan’s Nikkei 225 index finished up 0.20%, while Australia’s ASX 200 gained 0.19%. European bourses are positive, led by a 0.54% rise in the French CAC-40 index, while the UK’s FTSE 100 is down 0.11%. S&P 500 futures are higher suggesting a positive open on Wall Street.

In geopolitical news, risk sentiment is marginally better after the US talked Israel out of launching a full-scale ground assault in Gaza. On a happier note, especially for Ukraine, Russian President Putin reportedly suffered a heart attack on Sunday. On the other hand, his replacement may be even more deranged.

Things won’t change much today as there isn’t any top-tier data, which leaves bonds and equity moves dictating the US dollar direction.

EURUSD soared from 1.0572 to 1.0670 with the plunge in the US 10-year Treasury yield from 5.01% to 4.85% on Tuesday. The gains were extended to 1.0696 in Europe overnight before prices dropped to 1.0635 in early NY trading following another weak Eurozone PMI report. Manufacturing PMI fell to 43 from 43.4 (forecast 43.7), Services PMI dropped to 47.8 from 48.7, and Composite PMI fell to 46.5 from 47.2. According to ING Bank analysts, the data raises the risk of a technical recession but also points to easing inflation pressures. The EURUSD technicals turned bullish after the move above 1.0610 snapped the July downtrend and suggests further gains to 1.0750. However, momentum is already slowing.

GBPUSD rallied from 1.2134 to 1.2247 yesterday, thanks to falling US Treasury yields, and then consolidated the gains in a 1.2234-1.2289 range overnight. UK employment fell by 82,000 (3m/Aug) while the unemployment rate rose 0.2% to 4.2%. The rally stalled just below 1.2300, the top of the downtrend channel from July. A topside break targets 1.2350 then 1.2560.

USDJPY chopped about in a 149.32-149.83 range with lower equity prices and softer Treasury yields weighing on prices. Japan’s preliminary October Manufacturing PMI was 48.5, below estimates but unchanged from September.

AUDUSD rode the coattails of improved risk sentiment and climbed from 0.6331 to 0.6380 before easing to 0.6362 in early NY trading. Softer than expected Judo Bank Manufacturing and Services PMI data helped to limit gains. RBA Governor Michelle Bullock said the RBA would not adopt a fixed target for full employment and also said, “Our focus remains on bringing inflation back to target within a reasonable timeframe while keeping employment growing.”

The US data calendar is empty except for the second tier S&P Global PMI data. Traders prefer ISM PMI reports.

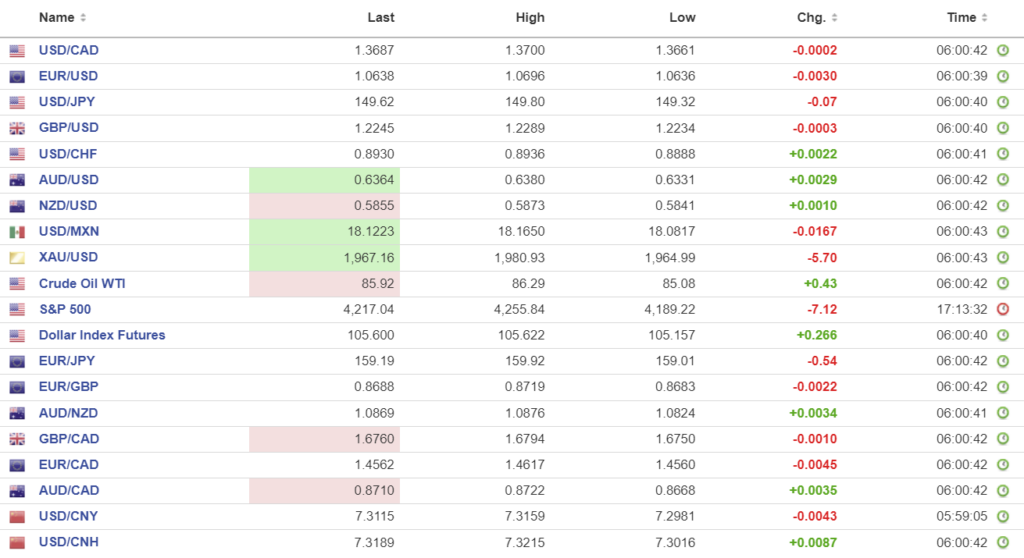

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1796, expected 7.2992, previous 7.1792.

Shanghai Shenzhen CSI 300 rose 0.37% to 3487.13.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com