July 17, 2024

- Data-rich, drama light day on tap.

- BoC rate cut on July 24 pretty much guaranteed.

- US dollar opens lower from Tuesday’s close but firmer compared to the open.

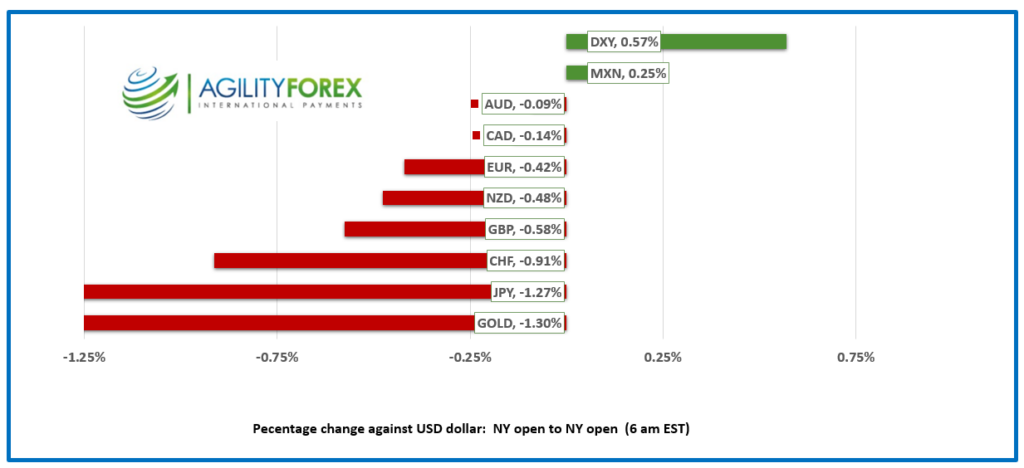

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3659, overnight range 1.3657-1.3686, previous close 1.3674

USDCAD is trading sideways and remains locked in its well-travelled trading band that has contained price movement since the beginning of May.

Yesterday’s soft Canadian inflation report (BoC CPI-medium 2.6%, compared to May 2.8%) combined with the weak Bank of Canada Business Oulook survey (BOS) gives Governor Tiff Macklem the green light to cut interest rates by 25 bps to 4.5% on July 24. He is pretty much guaranteed to do it, but without Fed Chair’s dovish comments on Monday, a rate cut would have been more of a toss-up. The BoC likes to say that they manage a “Made in Canada” monetary policy, which would be true if Canada was in a vacuum and didn’t trade or have any dealings with any other country.

WTI oil is suffering from fears of weak demand from China but garnering some support from the prospect of lower US interest rates jump-starting global growth. WTI traded in a 79.45-80.12 range.

USDCAD Technicals

The intraday technicals are neutral and just below the mid-point of its two month 1.3580-1.3880 range. While prices are below 1.3680, the risk is for a rest of the bottom of the band while a above the mid-point targets the top. Ho-hum.

Longer term. The move above the 100-day moving average at 1.3644 is guiding prices higher while guarding support from the 200 day moving average at 1.3590.

For today USDCAD support is at 1.3640 and 1.3610. Resistance is at 1.3710 and 1.3740. Today’s range is 1.3650-1.3750

Chart: USDCAD daily

Source: DailyFX

Biden Talking Tough (between naps) on Trade

Out-going US President Joe Biden is hoping to shore up his flagging re-election hopes by stealing pages from the Donny Trump Trade Manual. Bloomberg reports that the Biden administration is mulling over using a measure called the foreign direct product rule (FDPR). That’s a mechanism that lets “America impose controls over foreign-made products that contain even the tiniest bit of American technology.” They are reportedly threatening Japanese and Netherlands chip manufacturers for selling to China.

Trump Talking Tougher

Bloomberg published an interview with Donald Trump which was done a couple of weeks before he got shot in the ear. He said he would cut taxes and interest rates and promised a slew of new tariffs on friends and foes alike. He complained about the weak Japanese yen, which may have spurred today’s BoJ intervention. He also opined about making Taiwan pay for US protection, which makes sense as he is a “Don” although not a Corleone.

Fed-speak and 2nd Tier Data

Fed Chair Jerome Powell’s comments on Monday lifted the odds for a September rate cut to 91.6% according to the CME Fedwatch tool. His is the voice that counts. Yesterday, Fed Governor Adrian Kugler said it “would be appropriate to reduce rates later this year,” which traders translated to September. Her colleague Governor Christopher Waller is talking today and is likely to have a similar view. Today’s US data, Building Permits, Housing Starts, Capacity Utilization, and Industrial Production, won’t do anything to change traders’ outlook for US rates.

EURUSD

EURUSD is at the top of its 1.0896-1.0945 range despite Euro area inflation ticking down to 2.5% in June from 2.6% in May. The ECB monetary policy meeting is Thursday, and it should be uneventful with rates and guidance left unchanged.

GBPUSD

GBPUSD rallied from 1.2995 to 1.3045 after UK inflation data raised fears that the BoE could delay cutting interest rates. The data was largely as expected: Headline CPI rose 2.0% y/y in June, unchanged from May, while Core CPI was 3.5% and also unchanged from May. PPI prices ticked lower. Some analysts blamed Taylor Swift for inflation remaining sticky because her concerts led to elevated hotel demand and prices.

USDJPY

The Bank of Japan was at it again. USDJPY plummeted from 158.62 to 156.10 after likely, but unconfirmed BoJ FX intervention. Some analysts credit comments by soon-to-be President Trump suggesting that the yen was too weak, for sparking the BoJ action.

AUDUSD and NZDUSD

AUDUSD traded in a 0.6725-0.6755 range in line with broad-US dollar moves. Westpac’s Leading index was 0, unchanged from last month, and pointed to lacklustre growth in H2. NZDUSD rallied from 0.6037 to 0.6098 and is at the top of that band in NY trading. The gains coincided with New Zealand Q2 inflation rising less than expected by analysts and the RBNZ. Headline CPI rose 3.3% y/y compared to the forecast of 3.5% and Q1 at 4.0%. The NZDUSD rally occurred despite the data increasing the odds for earlier and deeper RBNZ rate cuts.

USDMXN

USDMXN chopped about in a 17.6481 to 17.8135 range, little changed from yesterday. Price action is conflicted by ongoing concerns about new President Claudia Sheinbaum’s economic policies, the return of Donald Trump to the White House, and hopes of Fed rate cuts.

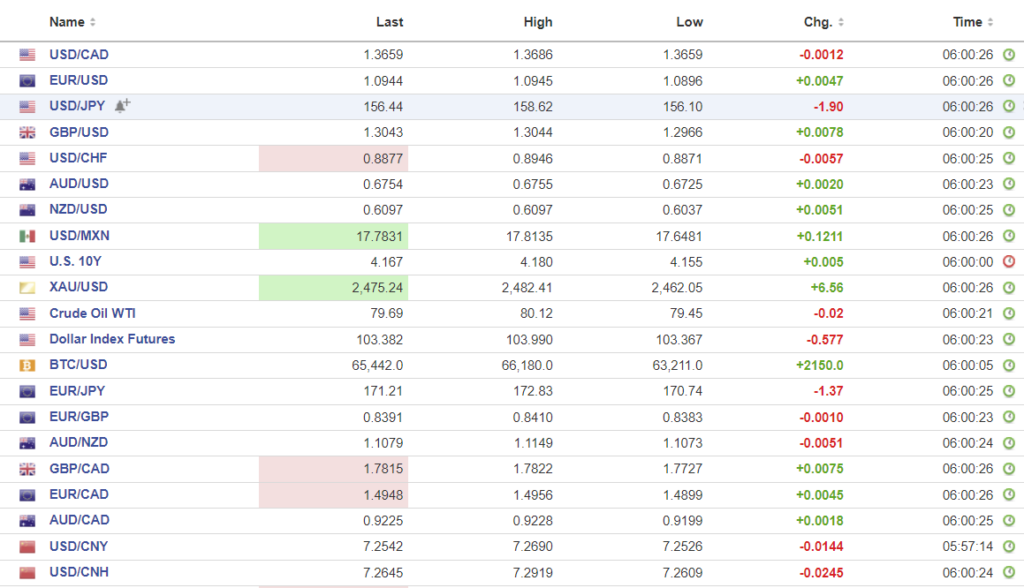

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1318 vs exp. 7.2630 (prev. 7.1328).`

Shanghai Shenzhen CSI 300 rose 0.09% to 3501.58.

Chart: USDCNY and USDCNH

Source: Investing.com