Photo: Bing AI

October 2, 2023

- US Government stays opens, traders just yawn.

- Fed Chair Powell speaks today.

- US dollar rallies compared to Friday’s open.

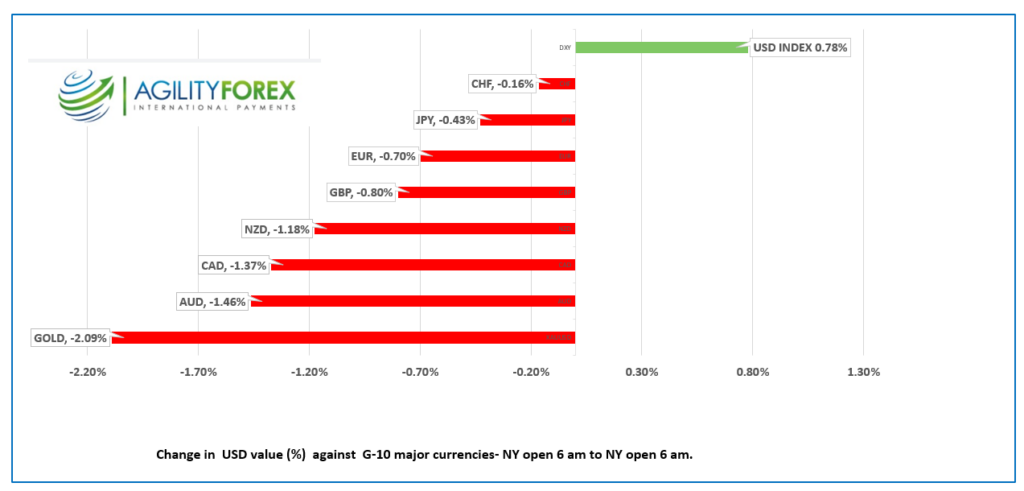

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3607-11, overnight range: 1.3562-1.3613, close 1.3579

USDCAD appeared to be setting up for a sharp drop on Friday, but it proved to be a head-fake when prices soared from 1.3417 through resistance at 1.3460 and 1.3510 to reach 1.3585 and closed near the top. The rally appears to be a late reaction to month and quarter-end portfolio rebalancing needs and than it was exacerbated by the surge in US Treasury yields.

Canada’s July GDP showed no growth and the August forecast of 0.1% suggests the Bank of Canada will leave interest rates unchanged on October 20. range

WTI oil prices are trading with a bid in a $90.61-$91.88 due to rising concerns that demand will outstrip supply. Opec is not expected to change production quotas at Wednesdays meeting.

It is a national holiday in Canada, depending upon where you live. Truth and Reconciliation Day is a statutory holiday for all federally regulated public and private sector employees. But not in all provinces. Only BC, Nova Scotia and PEI give people the day off.

USDCAD Technicals

The intraday USDCAD technicals turned bullish with Fridays breach of resistance at 1.3460. The following break above 1.3520, suggests that 1.3460 will be a short-term base and has ignited a new uptrend. The technicals are bullish above 1.3570, looking for a break above 1.3640 to extend gains to 1.3750. If broken, 1.4000 is in play.

For today, USDCAD support is at 1.3570 and 1.3520. Resistance is at 1.3630 and 1.3560. Todays Range 1.3570-1.3640

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

The show must go on. Not all U.S. Republican lawmakers came to their senses, but enough did and joined forces with Democrats to prevent a U.S. government shutdown, at least until the middle of November.

Even so, the insanity that permeates American lawmakers pales in the face of the deranged rantings of Russia’s Deputy Security Council Dmitry Medvedev, who advocates nuclear strikes in Ukraine and war on British troops if they deploy troops to Ukraine as suggested by the UK Defence Minister. Medvedev’s response had UK Prime Minister Rishi Sunak tripping over his tongue to clarify the British view. “What the defense secretary was saying was that it might well be possible one day in the future for us to do some of that training in Ukraine.”

Fed Chair Jerome Powell and Philadelphia Fed President Patrick Harker are in a roundtable discussion at 11:00 am EDT. Asia markets were extra quiet due to the Chinese Golden Week holidays and the Australian Labour Day holiday. European bourses are modestly lower, and S&P futures are unchanged. The U.S. 10-year Treasury yield climbed to 4.631% from Friday’s close of 4.571%.

EURUSD is trading with a negative bias in a 1.0534-1.0592 range. Rising U.S. Treasury yields, falling European equity index prices, and another contraction in Eurozone Manufacturing PMI (actual 43.4 vs. August 43.5) weighed on the currency. The short-term EURUSD technicals are in a downtrend bound by 1.0430 and 1.0660.

GBPUSD rallied in Asia, then tanked in Europe, falling from 1.2220 to 1.2161. The catalyst for the drop was the S&P Global Manufacturing PMI survey. The survey noted that although September’s results ticked up to 44.3 from 43.0 in August, it was “still among the weakest readings in the past fourteen years.” The GBPUSD technicals are bearish and in a 1.2040-1.2240 downtrend channel.

USDJPY traded erratically and is at the top of its 149.43-149.82 range. Prices were buffeted by a positive Tankan Survey showing Large Manufacturing Sentiment at its best level in 15 months and by higher U.S. Treasury yields. The BoJ Summary of Opinions suggested the ultra-easy monetary policy would not be changing anytime soon.

AUDUSD traded in a 0.6394-0.6446 range in a quiet session. Australians turned their clocks forward and then took the day off for Labor Day. The RBA meeting is tomorrow, and they are expected to leave monetary policy unchanged. The view was reinforced after TD Inflation data showed September inflation cooled to 5.7% y/y compared to 6.1% in August.

NZDUSD traded narrowly in a 0.5974-0.6008 range. The RBNZ is still expected to leave interest rates unchanged at 5.50% on Wednesday, despite more robust than expected GDP growth in Q2.

Today’s U.S. ISM Manufacturing PMI is expected to rise to 48.6 from 48.4.

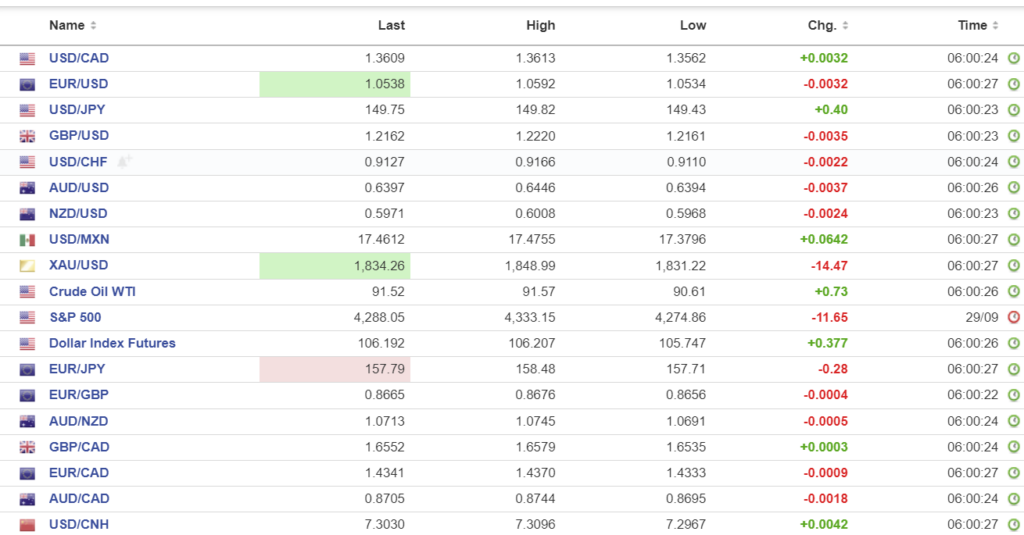

FX high, low, open

Source: Investing.com

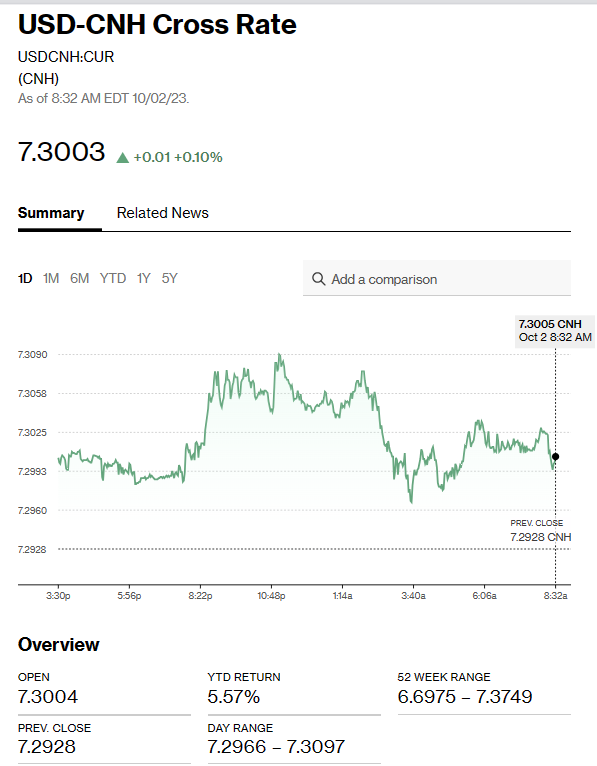

China Snapshot

Chinese markets are closed for Golden Week holidays.

Bank of China Fix: closed. previous 7.1798.

Caixin September Manufacturing PMI 50.6 (August 51)

Service PMI 50.2 (August 51.8)

Shanghai Shenzhen CSI 300 closed for Golden Week.

Chart: USDCNH (offshore)

Soource: Bloomberg