Photo: Disney

May 4, 2023

- Fresh, new US regional bank worries make a mockery of Fed.

- ECB hikes 25 bps, more hikes ahead.

- US dollar opens mixed compared to close but lower from yesterday.

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3607-11, overnight range 1.3584-1.3631, close 1.3615

USDCAD whipsawed post-FOMC and overnight but when the dust settled, the loonie remained inside this week’s range. USDCAD direction has everything to do with broad US dollar sentiment and oil prices, and very little to do with domestic influences.

As North American trading transitioned to Asia, oil prices collapsed. WTI plunged from Wednesday’s peak of $71.70/barrel to $63.71 reportedly due to algo trading and stop-loss selling in a very thin market. Nevertheless, the drop underpinned USDCAD.

Traders may get some fresh insight into the Bank of Canada’s inflation outlook today. Governor Tiff Macklem addresses the Toronto Board of Trade and the text of his remarks will be released at 12:50 pm ET.

Canada’s Merchandise Trade deficit flipped to surplus, rising to $0.97 billion from -$0.49 billion in April. The Ivey PMI data is ahead.

USDCAD Technical Outlook

The USDCAD technicals are bullish while prices are above 1.3560. A decisive break above 1.3660 sets the stage for a test of resistance at 1.3810. AA break below 1.3560 targets 1.3490.

For today, USDCAD support is at 1.3580 and 1.3560. Resistance is at 1.3650 and 1.3700

Today’s range 1.3560-1.3660

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Fed Chair Jerome Powell and his FOMC colleagues have a credibility problem.

Traders are not buying what policymakers are selling. They haven’t forgiven Powell for his failure to react to spiralling inflation in a timely manner.

In addition, Powell gets some of the blame for the collapse of Silicon Valley Bank Financial Group (SVB) and Signature Bank as the failures occurred on his watch, at least according to Senator Elizabeth Waren.

They have a point. The FOMC statement pronounced (again) “The U.S. banking system is sound and resilient.” Sure it is, if you are JPMorgan Chase or Bank of America. If you are a regional bank, not so much.

Moments after the FOMC statement, PacWest Bank (PACW: Nasdaq) announced that it was exploring “all strategic options” in the wake of its free-falling stock price. Oops. Soon Jamie Dimon may claim his comment about the banking crisis being over, was taken out of context.

Mr Powell must shake his head at the market reaction to the policy decision and press conference. He clearly stated that the Fed was not announcing a pause, but nevertheless, traders are pricing 75-100 bps of rate cuts by November. The US 10-year yield dropped from 3.60% on Monday to 3.35% overnight. The US dollar retreated, and gold prices soared.

Geopolitics may be playing a role in the spike in gold prices. XAUUSD climbed from $2016.84 at Powell’s press conference to $2077.89 in early Asa, before dropping to $2037.36 in NY. Russian authorities claim that a drone strike on the Kremlin was really a Ukrainian attempt to kill Putin. In retaliation, Russia’s Defence Secretary Medvedev called for Zelensky’s elimination.

Traders will be keeping a close eye on regional banks after the PacWest news.

Asian equity markets finished the session close to unchanged. Japan’s Nikkei 225 index rose 0.12% while Australia’s ASX 200 index fell 0.06%. European bourses are trading negative, and S&P 500 futures are trading modestly lower.

EURUSD is steady after the ECB hiked rates 25 bps to 3.25%. It is the seventh increase in a row, but with Euro area inflation sticky, there are more hikes in the pipeline.

EURUSD has been in an uptrend all week and added to the gains following the FOMC, reaching 1.1090. The topside level was tested again at the European open and then prices consolidated in a 1.1037-1.1090 range. The EURUSD uptrend that began in September is intact above 1.078.

GBPUSD rallied post-FOMC then traded in a 1.2554-1.2592 range overnight. The belief that the Fed has paused and will cut rates while the Bank of England has at least one more rate hike to go, is supporting prices. UK Services PMI rose to 55.9 in April compared to 54.9 in March.

USDJPY dropped from 134.81 to 134.16 before climbing to 134.52 in early NY. The steep drop in the US 10-year Treasury yield and a bit of safe-haven demand for yen is weighing on prices.

AUDUSD caught an up-draft following the Fed meeting and touched 0.6702. The overnight session was choppy with prices falling, then rebounding in a 0.6642-0.6698 range. AUDUSD continues to benefit (modestly) from this week’s surprise RBA rate hike, and from broad US dollar weakness.

Today’s US data includes weekly jobless claims and trade data.

FX open, high, low, previous close as of 6:00 am ET

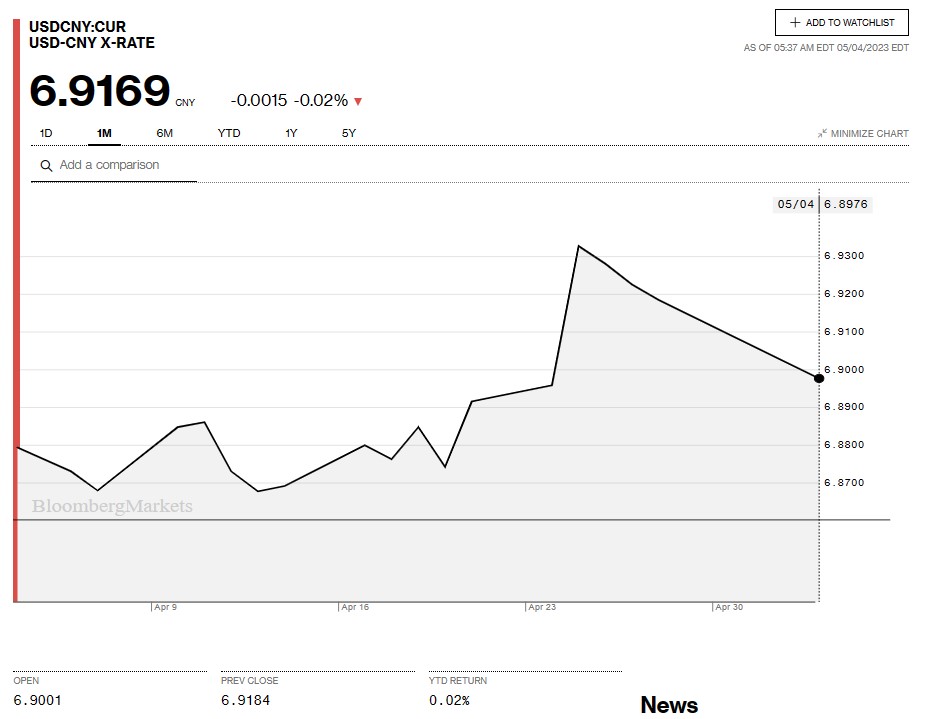

China Snapshot

Bank of China Fix: 6.9054, previous 6.9240.

Shanghai Shenzhen CSI 300 rises 0.03% to 4030.25.

Caixin Manufacturing PMI 49.5 (forecast 50.3, March 50.00

Chart: USDCNY 1 month

Source: Bloomberg