May 17, 2024

- Markets are closed in Canada and in most of Europe on Monday.

- Fed officials repeat “high rates for longer” mantra.

- US dollar claws back some losses.

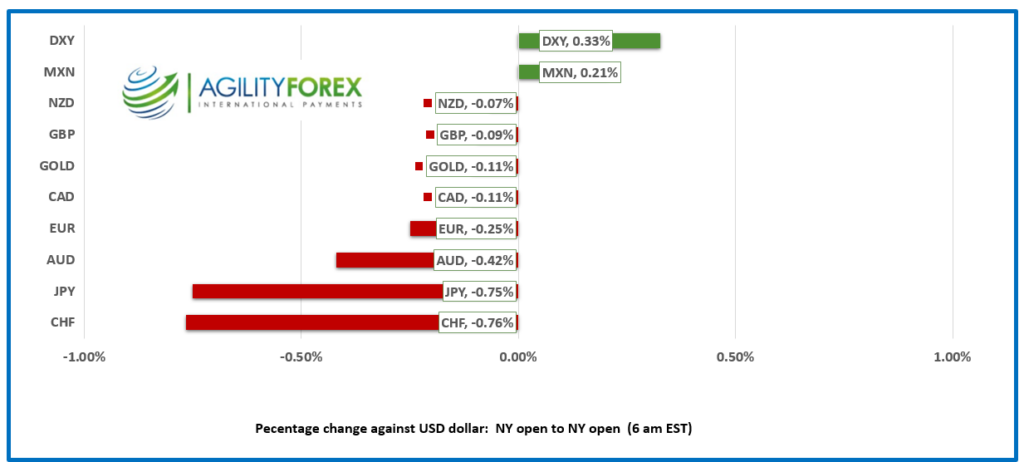

FX at a Glance

Source: IFXA/RP

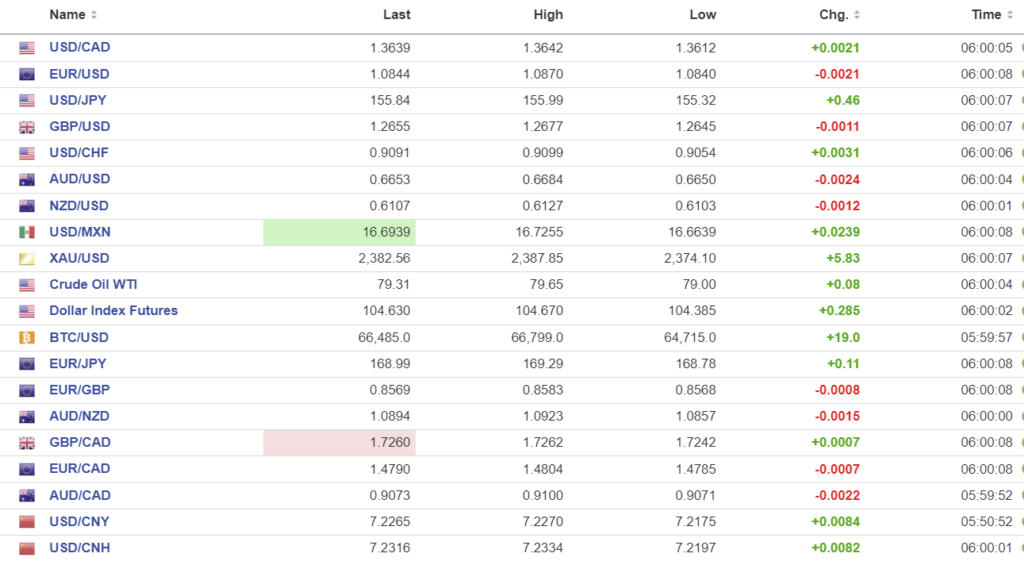

USDCAD Snapshot: open 1.3639, overnight range 1.3612-1.3642, close 1.3619

It is the May 24th weekend in Canada, the unofficial start to summer in the Great White North. The holiday is to celebrate Queen Victoria’s Birthday, which the woke have not realized was the British ruler when Britain colonized about 25% of the world. Let the Cancel Games begin. The fact that Monday is only the 20th has probably confused the muppets.

USDCAD failed in another attempt to break below support in the 1.3590 area yesterday and then spent the overnight session trading sideways but with a bit of a bid. All the USDCAD price action is dictated by the prevailing interest rate outlook for the Fed and at the moment, it is “high rates for longer.” The expectation for the Bank of Canada to cut rates in June is baked into the price.

And just to confirm what most Canadians already know, the Fraser Institute reports that living standards in Canada have declined by 3% since 2019. Sunny ways, indeed.

Oil prices are trading in a 79.00-79.65 range with support stemming from hopes of fresh demand after interest rate cuts in non-US markets stimulate demand.

There is more Fed speak but no economic data of note from Canada or the US.

USDCAD Technicals

The intraday USDCAD technicals flipped to bullish with the break above 1.3620 on the hourly chart and are looking for further gains to 1.3690. A move below 1.3610 targets the 1.3590 support zone again.

The longer-term uptrend line is intact above 1.3590, which is just above the 200-day moving average at 1.3565. Meanwhile, the downtrend line from mid-April comes into play at 1.3740.

For today, USDCAD support is at 1.3610 and 1.3590. Resistance is at 1.3660 and 1.3690. Today’s range is 1.3610-1.3680.

Chart: USDCAD daily

Source: DailyFX

Fed Officials Suggest Markets Need a Reality Check.

Cleveland Fed President Loretta Mester and Richmond Fed President Thomas Barkin echoed Fed Chair Powell’s earlier remarks that, because inflation risks persist, policymakers will leave rates at current levels for longer than expected. Ms. Mester said, “The most likely scenario for the overall economy and that of the region is that the current restrictive stance of monetary policy will continue to help moderate growth and labor market conditions and that this moderation will contribute to the further easing of price pressures,” adding, “I expect progress on inflation over time, but at a slower pace than we saw last year.” Mr. Barkin said it would take more time to get inflation down to 2.0%.

Those comments helped to boost the US 10-year yield from 4.31% on Wednesday to 4.39% today and lowered the odds of a September rate cut to 67%.

War and Pieces

Israel continues its mission to eradicate Hamas, who are waging war while using human shields in Rafah. Meanwhile, South Africa (which is at the bottom of the 2023 Corruption Perception Index Top 70; Denmark, Finland, and New Zealand are the top 3) is demanding that the UN International Court of Justice order Israel to halt its assault. It would come as no surprise to learn Iran paid off the South African politicians.

Meanwhile, Russia’s summer offensive into Ukraine is in full swing. Putin feels empowered after meeting with Chinese President Xi Jinping, although Jinping’s military aid may be extremely limited due to fears of more US sanctions. But the status quo may fall to pieces if NATO follows through on discussions to send troops (disguised as trainers) into Ukraine.

Profit-taking Weighs on Equities.

Asian equity indexes closed mixed. Australia’s ASX 200 fell 0.85% while the Nikkei 225 index dropped 0.34%. Hong Kong’s Hang Seng rallied 0.91%. European bourses are all negative, led by a 0.36% decline in the German DAX. S&P 500 futures are flat. Gold (XAUUSD) is close to this week’s peak and is trading at $2,386.97.

EURUSD

EURUSD traded negatively and is at the bottom of its 1.0840-1.0870 range, likely due to profit-taking ahead of the long weekend. Markets in Belgium, Denmark, France, Germany, Netherlands, Norway, and other countries are closed Monday. The final inflation readings for April were unchanged as expected. The ECB is expected to cut rates in June, but ECB policymaker Isabel Schnabel said, “Based on current data, a rate cut in July does not seem warranted. We should follow a cautious approach.”

GBPUSD

GBPUSD traded lower in a 1.2645-1.2677 range due to broad US dollar demand and rate cut pushback by Fed officials. Prices are also on the defensive due to expectations for a dovish outcome at next month’s Bank of England monetary policy meeting.

USDJPY

USDJPY rallied to 155.99 from 155.32 due to higher US Treasury yields and because the Bank of Japan did not reduce its purchases of JGBs.

AUDUSD AND NZDUSD

AUDUSD consolidated yesterday’s losses in a 0.6649-0.6684 range, although support following China’s actions to support the housing market was offset by soft retail sales data on Thursday. AUDUSD downside may be limited due to what some believe is the inflationary impact from the latest Federal budget, which may limit the RBA’s efforts to reduce rates.

NZDUSD remained inside yesterday’s range, trading in a 0.6102-0.6127 band with prices weighed down by profit-taking and renewed US dollar demand.

USDMXN

USDMXN rode a 16.6630-16.7255 roller-coaster and is the only currency to have gained against the US dollar, albeit only slightly.

BTCUSD

BTCUSD (Bitcoin) rallied steadily overnight, rising from 64,715 to 66,799 due to bullish forecasts and reports that the CME is considering listing spot Bitcoin.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1045 (forecast 7.2222) prev. 7.1020.

Shanghai Shenzhen CSI 300 rose 1.03% to 3677.97.

China is attempting a Housing market rescue. They scrapped the minimum rate for mortgages and cut the minimum downpayment to 15% for first time buyers (25% for second homes) in addition to telling local governments to buy homes at reasonable prices and turn them into affordable housing. The PBoC is establishing a $41.5 billion fund to facilitate the program.

Chinese economic data was mixed. Retail Sales rose 2.3% y/y in April which was below the 3.8% expected and 3.1% in March. Industrial Production rose6.7% (forecast 5.5%).

Chart: USDCNY and USDCNH

Source: Investing.com