Source: Wikimedia commons

- Powell says “time to retire Transitory”

- Wall Street futures clawing back Tuesday losses

- US dollar opens mixed, Commodity currency bloc gain.

FX at a Glance:

Source: IFXA Ltd/RP

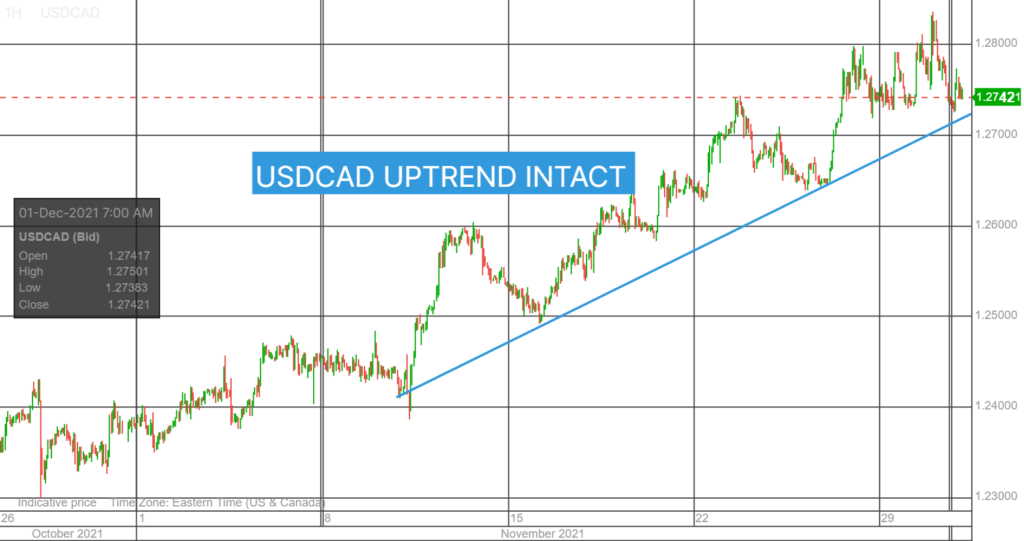

USDCAD Snapshot Open 1.2749-53, Overnight Range 1.2728-1.2785, Previous close 1.2779

USDCAD trading has been messy with prices bouncing between 1.2720 and 1.2835 since Monday. Domestic factors were not in play. The volatility is all due to Omicoron virus fears tanking oil prices and then Fed Chair Powell bowing to inflation realitites. That won’t change today.

Mr Powell resumes his testimony to the Senate and Wall Street’s reaction to his comments will dicatee USDCAD moves.

Today’s Canadian data is second-tier and will not be a factor.

Technical view: USDCAD retreated aggressively after touching 1.2835 yesterday. A decisive move below 1.2710 suggests a short-term top is in place and opens the door to further losses to 1.2510. A break above 1.2780 shifts the focus to 1.2850.

For today, USDCAD support is at 1.2710 and 1.2680. Resistance is at 1.2780 and 1.2840. Today’s Range 1.2710-1.2790.

Chart USDCAD 1 hour

Source: Saxo Bank

G-10 FX recap and outlook

It’s enough to make you seasick. Financial markets are rising and falling like a rowboat in an ocean storm. Panicked sellers meet optimistic buyers in a loop that has lasted for days.

A host of newly-minted Omicron experts popped up like weeds in springs, spouting tales of caution and hope, wreaking havoc in markets. Then Fed Chair Powell caved to reality and announced that it was a good time to retire “transitory” from Fed communications.

News of another coronavirus variant with a dose of inflation was not received cordially by traders. Stocks plunged, the US dollar soared, Treasury yields climbed, and oil prices tanked.

It didn’t last. The US dollar began retreating in the afternoon, oil prices firmed, and the move continued overnight. Asia equity indexes closed with small gains, while European bourses are on a tear. The German DAX index has gained 1.56%, followed by a 1.36% rise in the UK FTSE 100. S&P 500 and DJIA futures gained 1.19% and0.90%, respectively. WTI oil soared 4.6%, and gold rose 0.70%

Meanwhile, traders shrugged off comments by OECD officials warning that Omicron could exacerbate supply shortages while rising inflation could derail the global recovery.

US ADP employment change data showed 534,000 jobs gained, but the news was largely ignored.

EURUSD has been whippy. The single currency traded in a 1.1240-1.1381 range yesterday then settled into a 1.1304-1.1359 band overnight. The proverbial “buyers on dips” and profit-taking fueled the rally. In addition, EURUSD saw additional support from speculation that Powell’s acknowledgment of higher inflation would force the ECB to a similar move. Gains were capped by ongoing coronavirus concerns in Europe and modestly weaker Manufacturing PMI data and prices retreated to 1.1324.

GBPUSD mirrored EURUSD moves. It traded in a 1.3198-1.3368 range yesterday and a more sedate 1.3278-1.3331 range overnight. Prices are near the top of the range with better than expected Nationwide Housing and BRC Shop Price Index data supporting prices. GBPUSD needs a decisive break above 1.3360 to extend gains to 1.3500.

USDJPY bounced between 112.55 and 113.95 this week on the ebbs and flows of global risk sentiment and US Treasury yields. Since Monday, the 10-year Treasury yield see-sawed in a 1.431%-1.545% range and is currently sitting just below 1.50%. That rally lifted USDJPY from its depths.

AUDUSD and NZDUSD recouped all of yesterday’s losses overnight due to improved risk sentiment and higher commodity prices. AUDUSD got an added lift from better than expected data. Manufacturing PMI was 59.2 in November compared to 58.2 in October. GDP Rose 3.9% y/y in Q3 compared to the forecast for a 3.0% increase, although the Q/Q growth was down 1.9%.

Fed Chair Jerome Powell continues his Senate testimony today. Markets will be looking for more insight to his inflation outlook.

US economic data includes ISM Manufacturing PMI (forecast 61 vs previous 60.8) and ADP employment change (forecast 525,000).

Chart of the Day: EURUSD

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

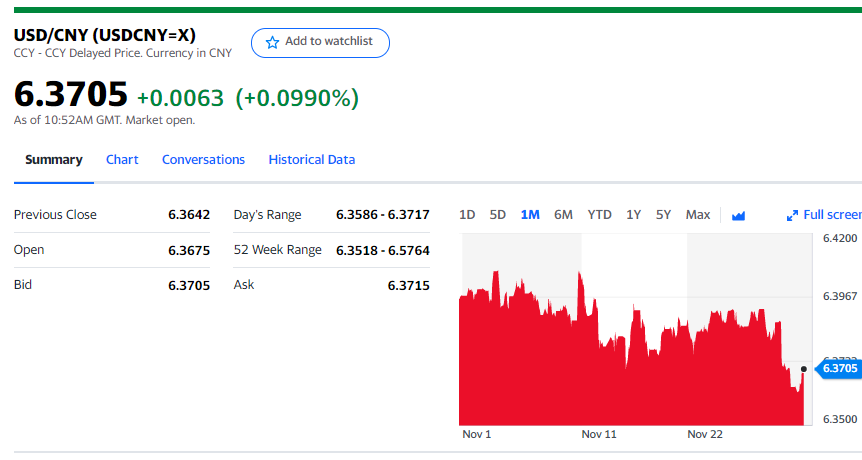

China Snapshot

Today’s Bank of China Fix 6.36.93 Previous 6.3794

Shanghai Shenzhen CSI 300 rose 0.24% to 4,843.85

Chart: USDCNY 1 month

Source: Yahoo Finance