Photo: Wikimedia commons

March 2, 2023

- US 10-year Treasury yield hits 4.083%, first time since November.

- Eurozone inflation ticks lower, but not by much.

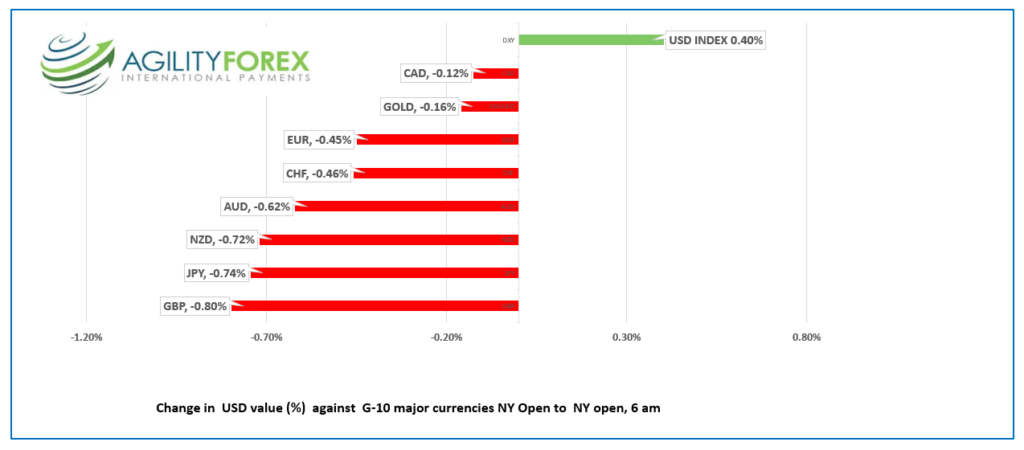

- US dollar opens with gains across the board.

FX at a glance-

Source: IFXA Ltd/RP

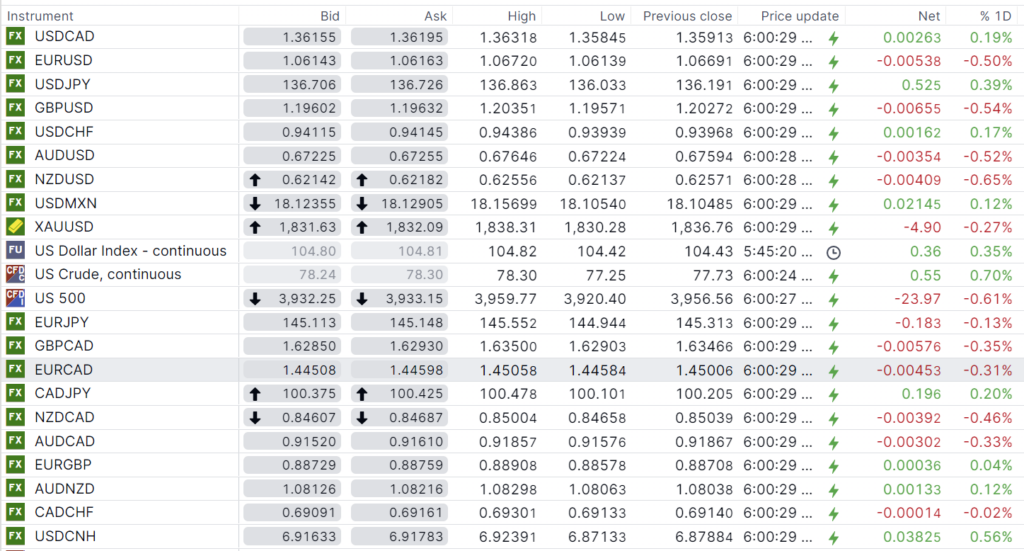

USDCAD Snapshot: open 1.3616-20, overnight range 1.3585-1.3632, close 1.3591

USDCAD is where the buffalo roam. (Home on the Range). The currency pair rises and falls with S&P 500 index moves, while domestic data and even Bank of Canada pronouncements has limited, if any, impact.

USDCAD direction is determined in America. The market focus is locked-in on the Fed’s terminal rate, which is a level that is unknown to the Fed. Recent sound bites from Fed officials have been hawkish and since the FOMC meeting isn’t until March 22, there is a lot of room for market angst, which translates to volatility.

WTI oil prices are also rangebound in a $72.00-$80.00/barrel band. Traders continue to expect higher prices from renewed Chinese demand although the EIA report that US crude inventories rose 1.18 million barrels tempered their enthusiasm.

The Canadian economic calendar is empty.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3570, looking for a break above the 1.3680-1.3700 are to extend gains to 1.3800. A break below 1.3570 targets 1.3510, then 1.3450.

The weekly USDCAD chart suggests that the downtrend line from October 2022 has been breached with last week’s move above 1.3520, opening the door to further gains to 1.4000. The uptrend from April 2022 is intact above 1.3190, which guards the long term uptrend that began in May 2021 and is intact above 1.2990.

For today, USDCAD support is at 1.3560 and 1.3510. Resistance is at 1.3660 and 1.3690.

Today’s range 1.3560-1.3660

Chart: USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

Skittish traders went from cautiously optimistic earlier this week to pessimistic yesterday and overnight. The better-than-expected Chinese PMI data on Tuesday raised hopes for a global economy recovery. It was a short-lived sentiment.

US data disappointed. The Chicago PMI index was 43.6, in contraction territory and weaker than in January. US Consumer Sentiment declined for the second month in a row. Hawkish Fed speak and the increase in the “prices Paid” component of the ISM Manufacturing report sparked US dollar demand and a sell-off in equities.

Geopolitical tensions continue to rumble in the background. Chinese officials will be discussing its economy as the National Committee of the Peoples Political Conference starts March 4 followed by the National Peoples Congress. President Putin will be chairing a Russian Security Council meeting on Friday. US Defence department officials warn that Iran has enriched uranium to, or close to, weapons-grade.

Asian equity indexes closed with small losses except for Australia’s ASX 200 which finished just above flat for the session. European bourses are defensive and in negative territory with the German Dax index down 0.37%.

S&P 500 futures are 0.44% lower while gold and oil are posting small gains. The US 10-year yield traded in a 3.991-4.083%, with peak occurring after today’s US data.

US weekly jobless claims surprised forecasters again. Jobless claims were 190,000 in the week ending February 25, compared to the forecast of 195,000. The results are further evidence that the US job market is tight which risks wage inflation.

EURUSD peaked at 1.0686 yesterday, closed at 1.0669, the slid steadily to 1.0590 in NY. Speculation that the ECB will hike rates to over 4.0% was reinforced today after Eurozone data showed inflation remained elevated. Harmonized Index of Consumer Prices (HICP) Core was 5.6% y/y in February compared to 5.3% in January. EURUSD remains supported by the data, but gains are struggling to the US 10-year yield rising above 4.0%.

GBPUSD traded negatively in a 1.1931-1.2035 range. Sterling is paying the price following yesterday’s comments by Bank of England Governor Andrew Bailey. His remarks were rather wishy-washy, suggesting rates could either remain unchanged or go higher. Analysts considered his comments dovish and sold GBPUSD. EURGBP demand following firm Euro area inflation data exacerbated GBPUSD selling pressure.

USDJPY traded firmer in a 136.03-137.05 range with the peak level seen following the US jobless claims data which underscored the risk for higher US rates for longer. USDJPY continues to derive support from dovish comments by BoJ nominees.

AUDUSD is at the bottom of its 0.6702-0.6765 range as the prospect of sharply higher US rates overshadows the outlook for a RBA rate increase next week.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

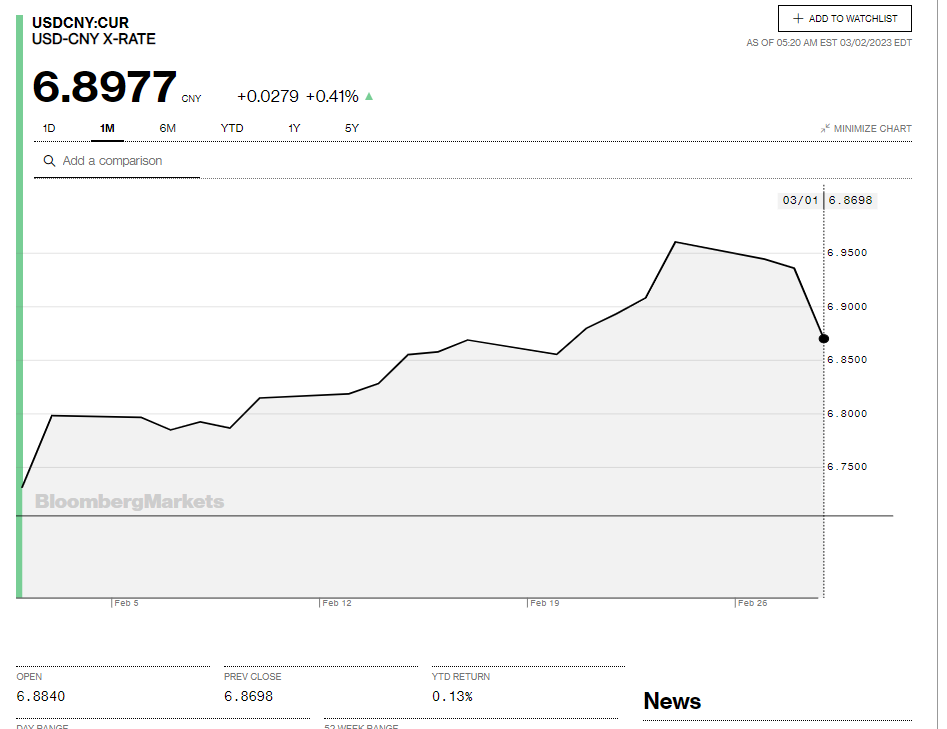

China Snapshot

Bank of China Fix: 6.8808, Previous: 6.9400

Shanghai Shenzhen CSI 300 fell 0.22% to 4117.74.

Reuters sources claim policymakers are discussing raising the 2023 growth target from 4.5-5% to %-5.5%.

Chart: USDCNY 1 month

Source: Bloomberg