Photo: Wikimedia Commons

June 5, 2023

- Saudi Arabia goes solo and cuts oil production.

- Fed rate hike debate is a coin toss.

- US dollar consolidating Friday’s post-NFP gains-CAD outperforms.

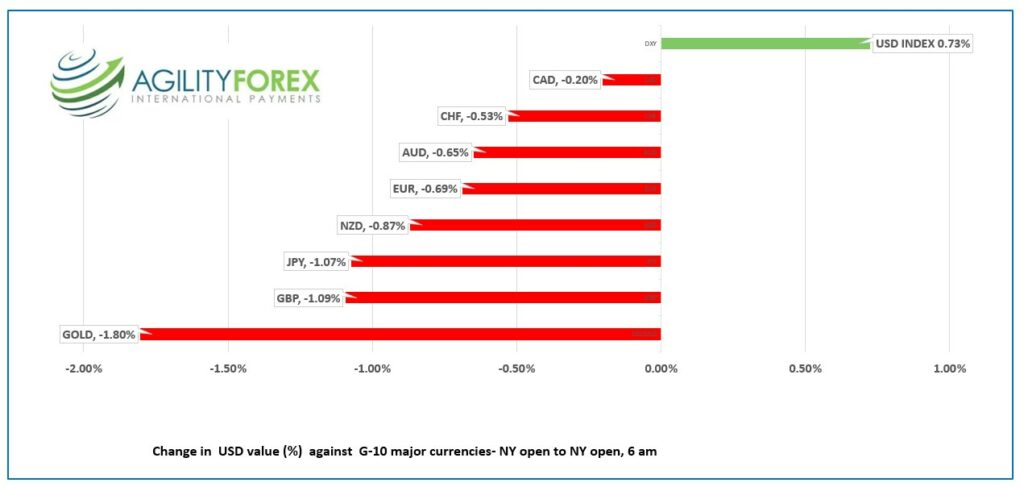

FX at a glance

Source: IFXA Ltd/RP

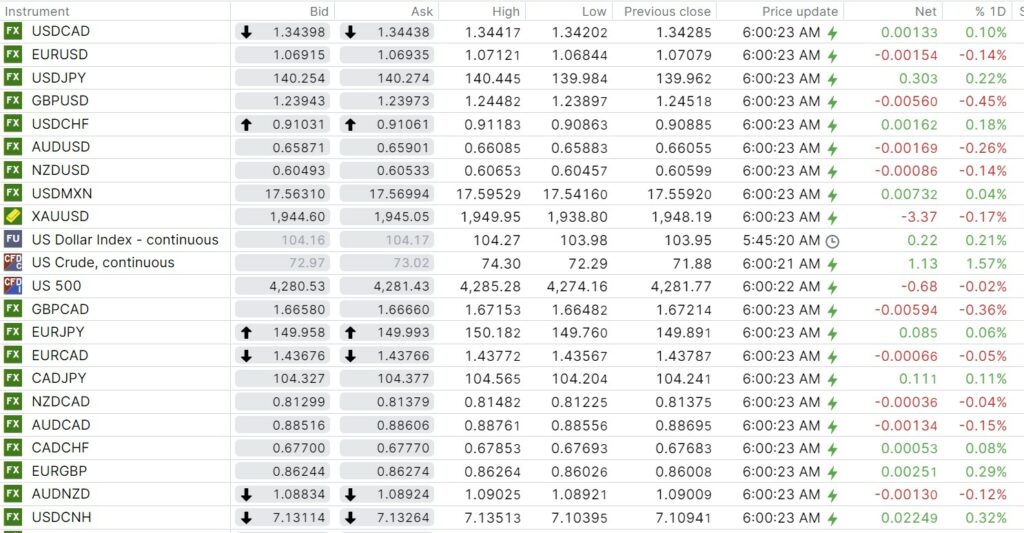

USDCAD Snapshot: open 1.3440-44, overnight range 1.3420-50, close 1.3429

USDCAD was largely ignored int the post-NFP drama and consolidated its losses after falling from 1.3650 May 31 to 1.3405 Friday.

Traders are looking ahead to Wednesday’s Bank of Canada meeting. Most economists expect the BoC to leave rates unchanged since there is no press conference. However, Scotiabank Head of Capital Markets Economics Derek Holt thinks a 0.25 bp bump is warranted.

Saudi Arabi wanted to cut oil production but the rest of Opec preferred the status quo. The decision was to leave production unchanged except for Saudi Arabia who decided they would reduce production by 1.0 million barrels/day. WTI rose to $74.30/barrel after closing Friday at $71.88 for a 3.3% gain and I are trading in NY at $73.11/b.

USDCAD Technical Outlook

The intraday USDCAD technicals are unchanged from Friday. They are bearish below 1.3480, looking for a break below 1.3390 to extend losses to 1.3350. A move above 1.3480 suggests further 1.3400-1.3600 consolidation.

The longer term USDCAD technicals are bearish below 1.3640 and looking for a move below 1.3250 (2023 low) to test the 1.3000 (61.8% Fibonacci retracement of April 2022, 1.2405-October 2022, 1.3965 range)

For today, USDCAD support is at 1.3410 and 1.3360. Resistance is at 1.3480 and 1.3550.

Today’s range 1.3400-1.3480

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Friday’s nonfarm payrolls report (actual 339,000 vs forecast 190,00) raised the odds for an unchanged Fed decision on June 14, to 78.2%. The odds for a July rate hike are 68.5%. The results boosted the US 10-year yield from 3.61%, pre-NFP to 3.75% in NY today.

Equity traders were not concerned about the jobs data. It may be due to fading recession fears and the sense that the Fed rates are close to peaking. Japan’s Nikkei 225 index closed with a gain of 2.20%, its highest level since 1990. European bourses are slightly higher. The UK FTSE 100 is up 0.50% while the German Dax has gained 0.03%. S&P 500 futures are unchanged.

China and US tensions are elevated so much so, that China refuses to talk to US Defense Secretary Lloyd Austin. China blames the US for sanctioning Chinese officials and challenging China’s claim to the entire South China Sea for the hostility.

EURUSD is consolidating Friday’s post-NFP losses and is at the bottom of its 1.0684-1.0712 overnight range. German and ECB Services PMI data were a tad weaker than in April but not a factor for markets. ECB President Christine Lagarde testifies to the EU parliament, and she is expected to reiterate her well-discussed hawkish message.

GBPUSD rallied last week but went off the rails after US employment data. GBPUSD dropped from a pre-NFP peak of 1.2542 to 1.2452 in early NY trading today. UK Services May PMI was close to unchanged at 55.2 (April 55.1) and traders ignored the data.

USDJPY rallied following Friday’s robust US nonfarm payrolls report, rising from 138.70 to 140.45 in Europe overnight. Analysts predict the Bank of Japan will intervene if USDJPY rises to 145.00. Traders are likely to test that theory.

AUDUSD traded negatively in a 0.6588-0.6609 range. Australia and New Zealand markets were closed for holidays. Prices received a bit of support from higher iron ore prices and the prospect of a RBA rate hike tomorrow. Many analysts were spooked by the upside surprise to April inflation and believe policymakers will raise rates 25 bps, however the consensus view is for rates to be unchanged.

US ISM Services PMI and Factory orders data are due.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

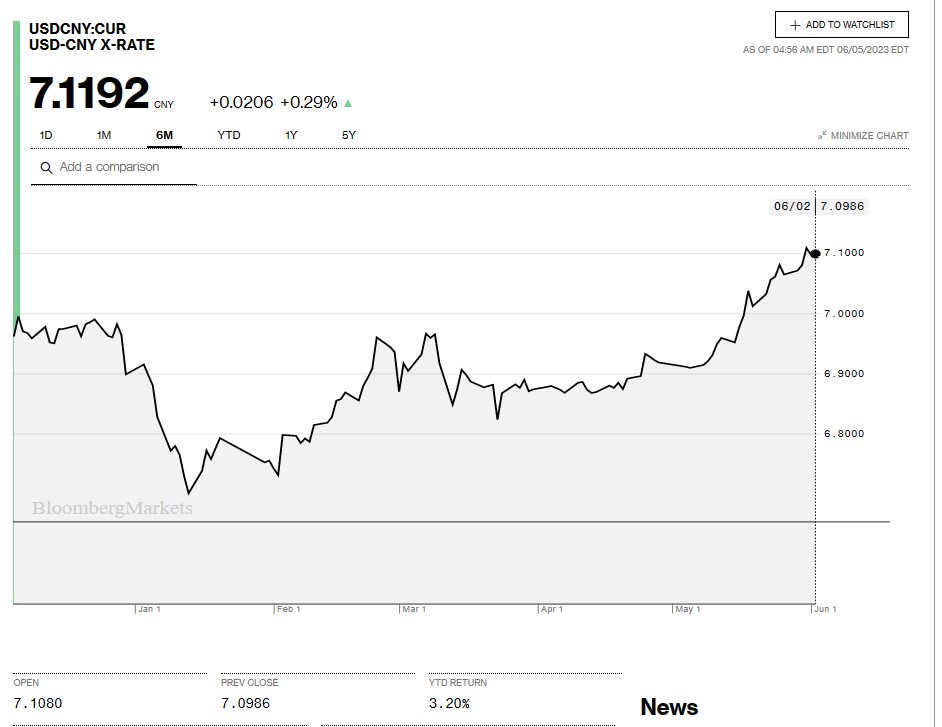

China Snapshot

Bank of China Fix: 7.0904, previous 7.0939

Shanghai Shenzhen CSI 300 fell 0.46% to 3844.25.

Caixin May Services PMI 57 vs April 57.

Chart: USDCNY 6 month

Source: Bloomberg