Source: Wikimedia commons

- GBPUSD soars after Prime Minister fired

- USDJPY trades above 150 then retreats quickly

- US dollar opens firm supported by higher Treasury yields

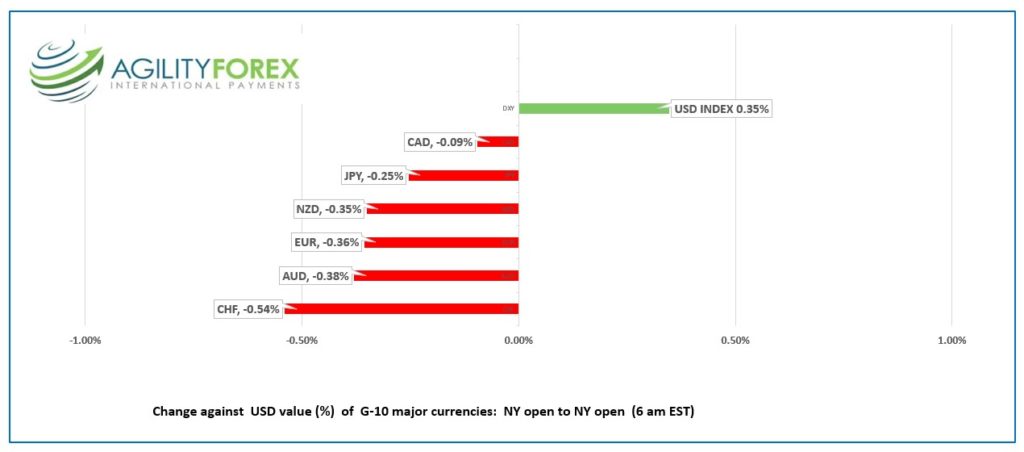

FX at a glance:

Source: IFXA Ltd/RP

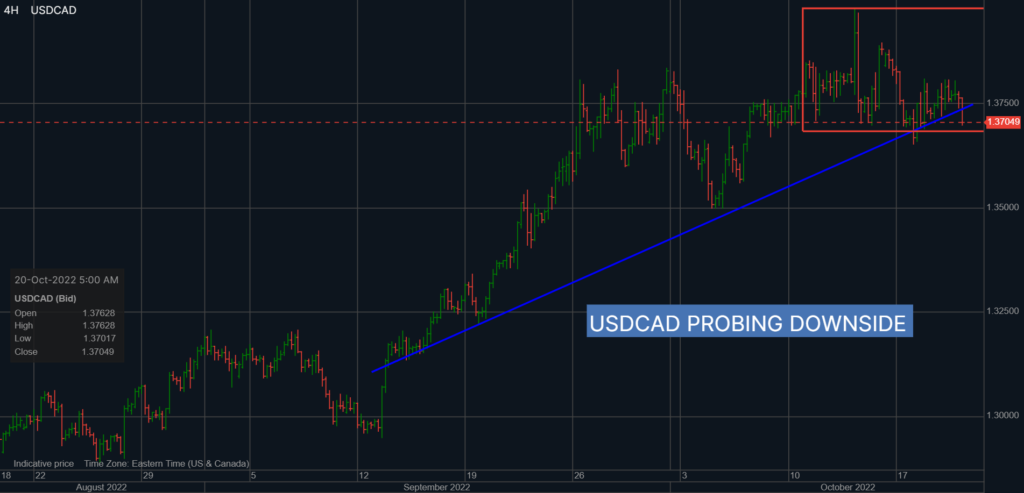

USDCAD Snapshot: open 1.3739-43, overnight range 1.3699-1.3805, close 1.3764

USDCAD rallied in in early Asia then dropped from the session peak to the low in NY as prices tracked the modest recovery in S&P 500 futures.

USDCAD churned in the wake of the inflation report yesterday. CPI rose 0.1% m/m in September, a tick higher than forecast, but the headline year over year number ticked lower to 6.9% from 7.0% in August. The results pretty much guarantee a 75-bps rate hike next week.

Nevertheless, other than the initial USDCAD volatility around the data release, the key focus is the US equity markets and rising Treasury yields.

The US 10-year Treasury yield rose from 4.007% yesterday to 4.18% today and is trading at 4.119% in NY.

WTI oil prices rallied from $82.63/barrel yesterday to $87.30/b in NY today. Prices got a bit of a boost from yesterday’s EIA crude inventories data which showed stocks falling by 1.72 million barrels in the previous week.

USDCAD Technical outlook

The intraday technicals flipped to bearish today with the move below 1.3730 that sets the stage for further losses to 1.3660. A break below 1.3660 targets 1.3550. A move above 1.3830 suggests further 1.3660-1.3860 consolidation.

For today, USDCAD support is at 1.3660 and 1.3610. Resistance is at 1.3740 and 1.3790. Today’s range: 1.3660-1.3760

Chart: USDCAD 4 hour

Source: Saxo Bank

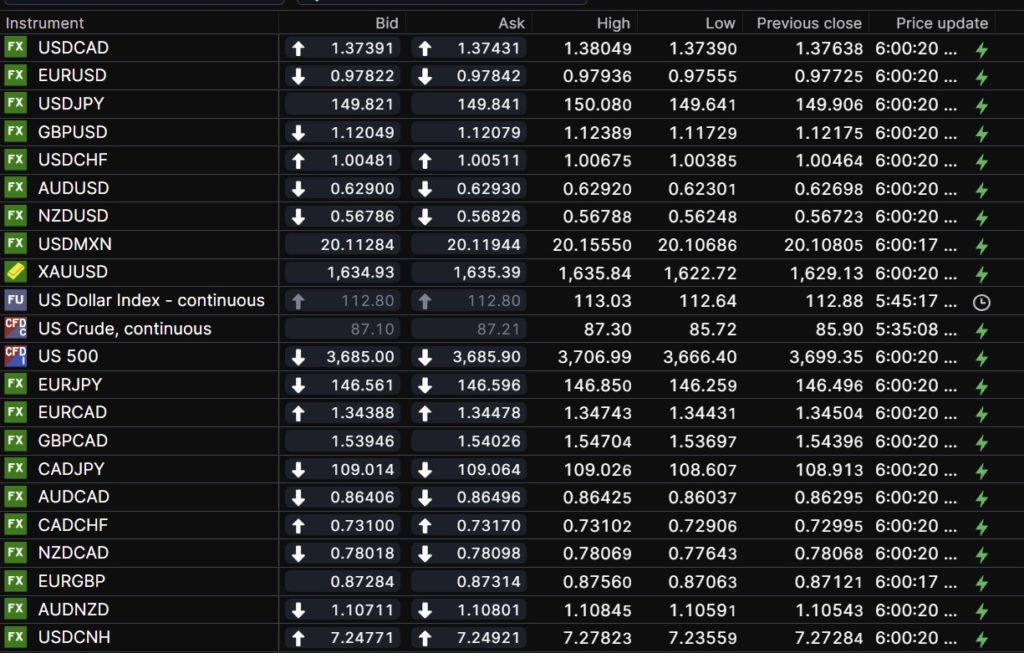

G-10 FX recap and outlook

FX markets are skittish as traders ask themselves if the US dollar has peaked. Equity traders are flirting with the notion that since the S&P 500 has dropped 22.47% year-to-date, perhaps they have seen the bottom. Bond traders are wondering if the 10-year Treasury yield has peaked.

The answer to all the above questions is probably not. US inflation is far above the Fed’s 2.0% target and Chair Powell is determined (he said so) to hike rates as high as needed to tame the inflation beast.

Asian equity indexes closed in the red led by a 1.02% drop in Australia’s ASX 200. European bourses are climbing off their session lows but are still in negative territory. S&P 500 futures have bounced of the overnight bottom but still need to rise another 0.22% to achieve unchanged status.

The US weekly jobless claims underscored the strength in the labour market. The number of claims fell 12,000 to 214,000 last week, easily beating the forecast of 230,000.

EURUSD consolidated yesterday’s losses in a 0.9756-0.9836 range. German Producer Prices data was a tad better than expected but largely ignored. Traders are biding their time until next week’s ECB meeting with a 75 bp hike price in.

However, the good jobless claims data was offset by a weaker than forecast Philadelphia Manufacturing Survey. This is the index’s fourth negative reading in the past five months.

GBPUSD soared, rising from an overnight low of 1.1173 to 1.1306 after Prime Minister Liz Truss resigned (fired). The gains were short lived as the PM’s resignation does nothing to quell the turmoil in UK politics. Dovish comments from Bank of England deputy governor Ben Broadbent are also hampering gains. He said suggested that markets may have overestimated how high rates will rise.

USDJPY traders taunted the Bank of Japan and the Ministry of Finance when they boosted prices to 150.08, the level expected to trigger FX intervention. Alas, no dice. USDJPY is trading at 149.89 with prices supported by the 10-year treasury yield at 4.119%.

AUDUSD dropped in early Asia trading then soared from 0.6230 to 0.6329 in early NY, powered by a modest retreat in the US dollar against the major G-10 currencies and an Australian unemployment report which wasn’t as bad as the headline implied. Australia only added 923 jobs in September (forecast 25,000) but the unemployment rate was unchanged at 3.5%. The rally was helped after National Australia Bank’s Business Confidence Survey rose to 9 q/q, compared to 5 previously.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

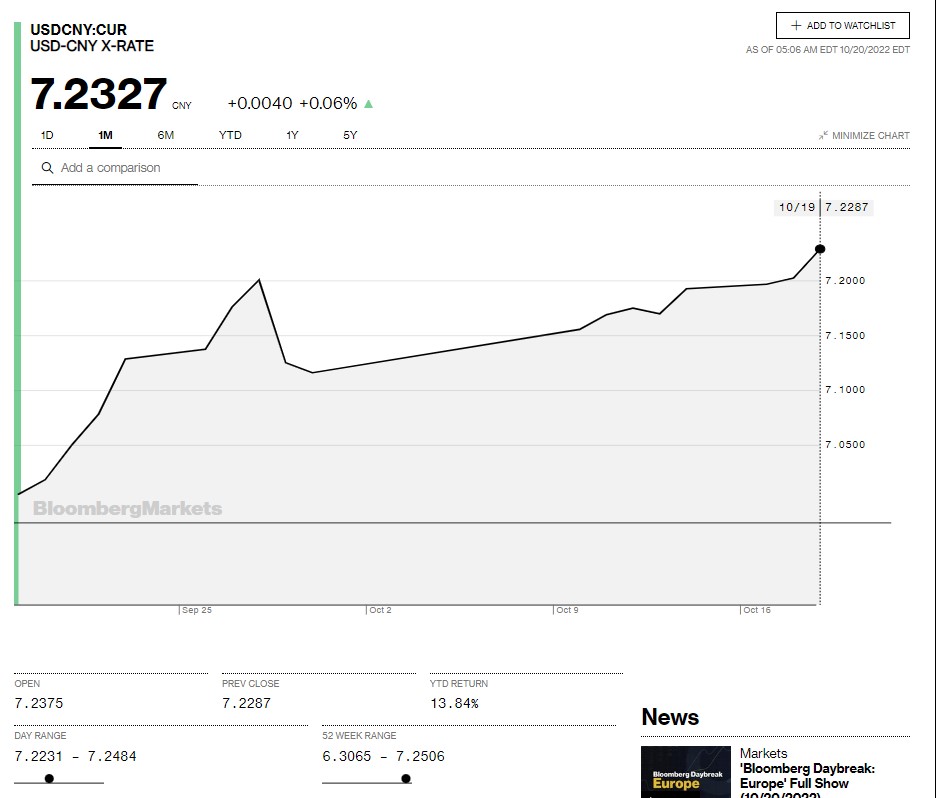

China Snapshot

Today’s Bank of China Fix: 7.1188, previous 7.1105

Shanghai Shenzhen CSI 300 fell 0.57% to 3754.93

Stocks fell with softer yuan. Markets concerned about President Xi Jinping’s plan to “regulate the accumulation of wealth.

Chart: USDCNY 1 month

Source: Saxo Bank