Source: Bing AI

July 11, 2023

- GBPUSD rallies thanks to wage gains

- IEA reiterates forecast of tight oil market in H2.

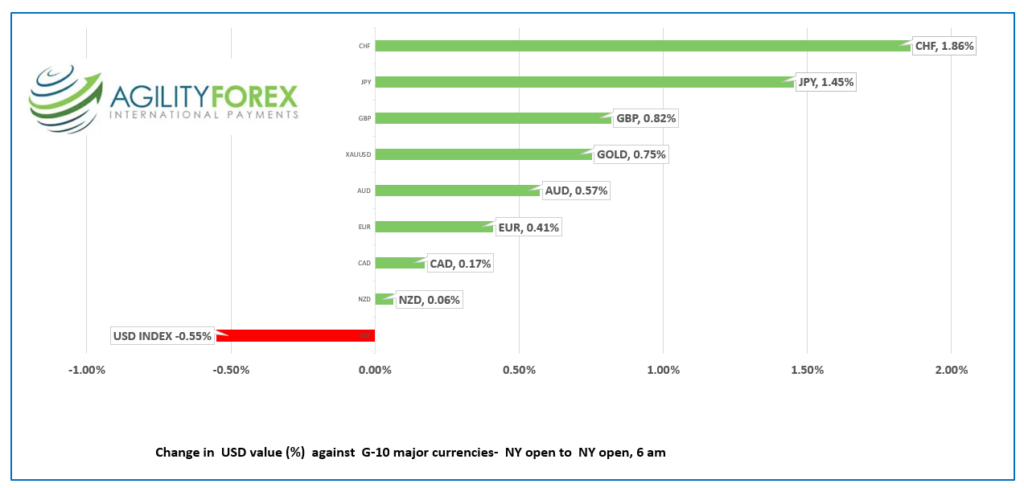

- USD extends yesterday’s losses-CHF outperforms.

FX at a glance:

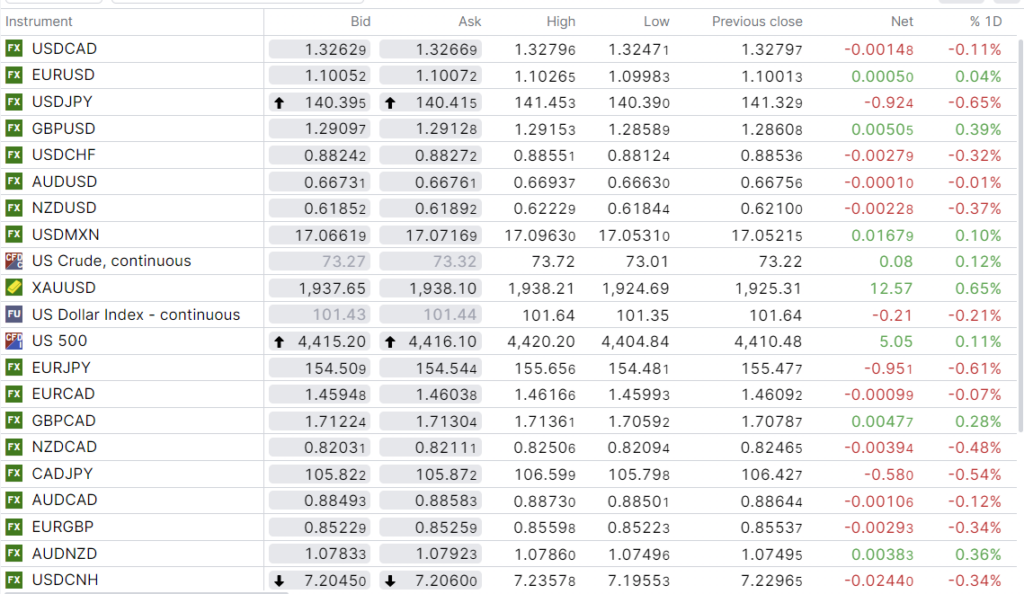

USDCAD Snapshot: open 1.3263-67, overnight range 1.3247-1.3281, close 1.3280

USDCAD is trading defensively but has been unable to break below last week’s floor despite robust domestic employment data and a disappointing US NFP report.

USDCAD selling pressure stems from expectations that the Bank of Canada will raise rates at Wednesday’s meeting and broad US dollar weakness. The greenback is being sold due to improved global risk sentiment after Chinese announced some targeted stimulus and hopes that Wednesday’s US inflation report is low enough to suggest the Fed’s tightening cycle is near an end.

USDCAD is also undermined by steady to firm oil prices. WTI is bouncing in a $73.01-$73.72/barrel range with a bit of a bullish bias after IEA officials reiterated their forecast of tighter crude supply in H2 2023.

The Canadian economic data calendar is empty.

USDCAD Technical Outlook

The USDCAD intraday technicals are bearish below 1.3320 and looking for a break below 1.3240 to extend losses to 1.3210, then 1.3150. A break above 1.3320 targets 1.3380 and suggest further 1.3240-1.3340 consolidation is ahead.

USDCAD has traded in a 1.3120-1.3660 range since April. After several attempts at a topside break-out failed, the currency pair is poised to test the strength of support in the 1.3120 area.

The long term uptrend comes into play in the 1.3000-1.3020 area.

For today, USDCAD support is at 1.3240 and 1.3210. Resistance is at 1.3320 and 1.3360.

Today’s range 1.3240-1.3310

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap

The US dollar is under duress in anticipation of a sharp fall in tomorrow’s US inflation readings. Headline CPI is expected to drop to 3.1% y/y from 4.0%, while Core CPI is expected at 5.0% compared to 5.3%. The results may not be enough to prevent the Fed from hiking rates on July 26, but they could suggest the tightening cycle is nearing completion.

On the other hand, if the CPI data is higher than expected, the stuff will hit the fan and the dollar will rally.

Global risk sentiment is positive, partly because of China’s latest measures to shore up its economy and thanks to somewhat dovish comments from a couple of Fed officials yesterday. Cleveland Fed President Loretta Mester said rates needed to move up “somewhat further and hold there for a while.” Atlanta Fed President Raphael Bostic was more dovish, suggesting rates did not have to rise any further. He said, “I have the view that we can be patient, our policy right now is clearly in the restrictive territory.”

Traders are being distracted by headlines about the NATO summit and the debate as to whether Ukraine should be admitted as a member. President Biden says “No,” but others argue that having a heavily armed, unaligned country in Europe is just asking for trouble.

Asian equity indexes closed on a happy note, led by a 1.50% gain in Australia’s ASX 200. European bourses are all higher, except the UK FTSE 100, which is 0.16% lower. S&P 500 futures are up 0.11%. The US 10-year Treasury yield is 3.96%.

EURUSD rallied to 1.1026 then retreated to 1.0982 in NY as traders adjusted positions while biding their time until Wednesday’s US inflation numbers. ZEW data showing worsening outlooks for German and the Eurozone were largely ignored. EURUSD is in a minor uptrend above 1.0950.

GBPUSD rallied from 1.2750 yesterday to 1.2918 in early NY today after UK average earnings rose higher than expected in the 3-month period ending in May, while the results from the previous earnings data were revised higher. Some analysts believe that the results could force the Bank of England to raise rates by 50 bps in August. However, jobless claims rose, and the unemployment rate climbed to 4.0% from 3.8%.

USDJPY fell from 141.45 to 140.17 in early NY trading as traders refocus on the risk of BoJ tightening while the Fed reaches its terminal rate. USDJPY is also being sold because of improved global risk sentiment and the US 10-year Treasury yield falling to 3.984% from 4.08% yesterday.

AUDUSD gave up earlier gains and dipped to 0.6654 from 0.6694 after positive sentiment from better than expected data, faded. NAB Business Confidence Index came in at 0 compared to -0.4% in May, while Business Conditions improved to 9 from 8. Westpac Consumer Confidence was 2.7% as expected.

NZDUSD is tracking AUDUSD moves and is at the bottom of its 0.6177-0.6223 range. The RBNZ is expected to leave rates unchanged when policymakers meet tomorrow.

There are no top-tier US economic data releases today.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

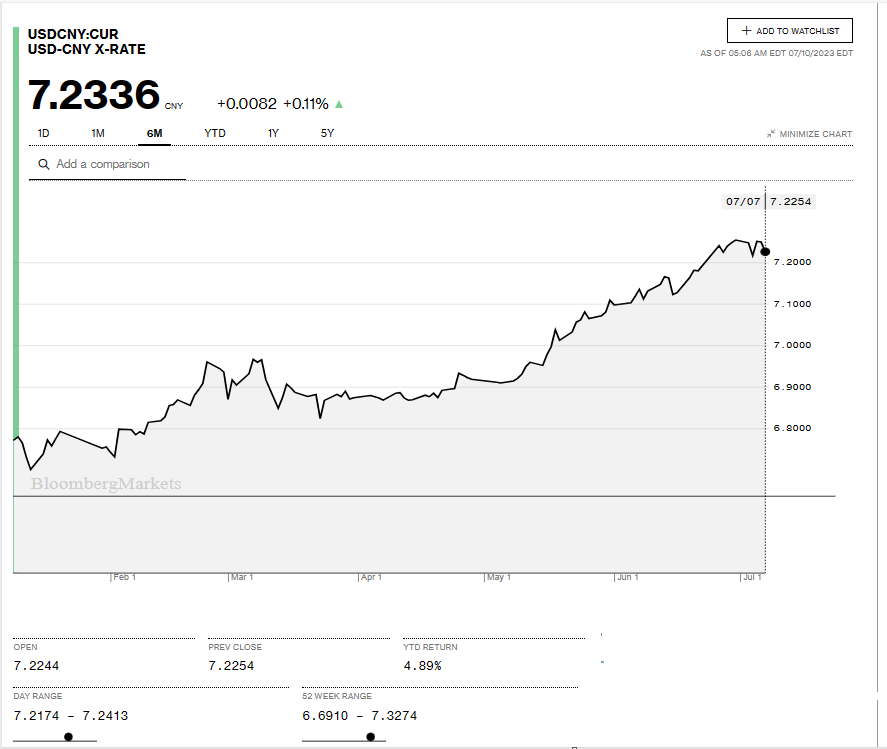

China Snapshot

Bank of China Fix: 7.1886 (expected 7.2177) Previous 7.1926

Shanghai Shenzhen CSI 300 rose 0.65% to 3869.49.

China announced the extension of the 16-point plan designed to support healthy development of real estate market, until the end of 2024. In addition, authorities asked banks to extend loans to developers that mature before the end of 2024 for another year beyond their maturities.

Chart: USDCNY 6 month

Source: Bloomberg