Photo: Freekpik.com

May 24, 2023

- FOMC minutes released this afternoon.

- Debt default concerns rise as talks rise.

- US remains bid while NZD crashes.

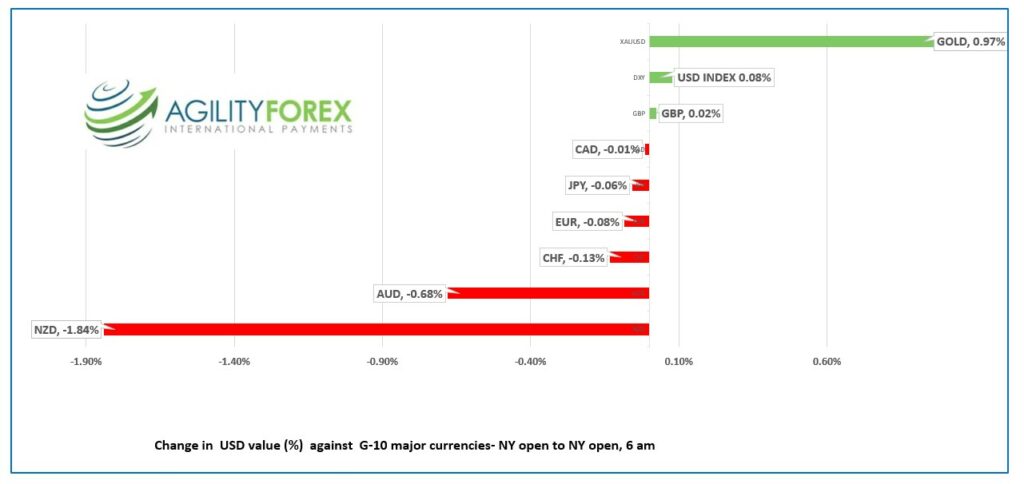

FX at a glance

Source: IFXA Ltd/RP

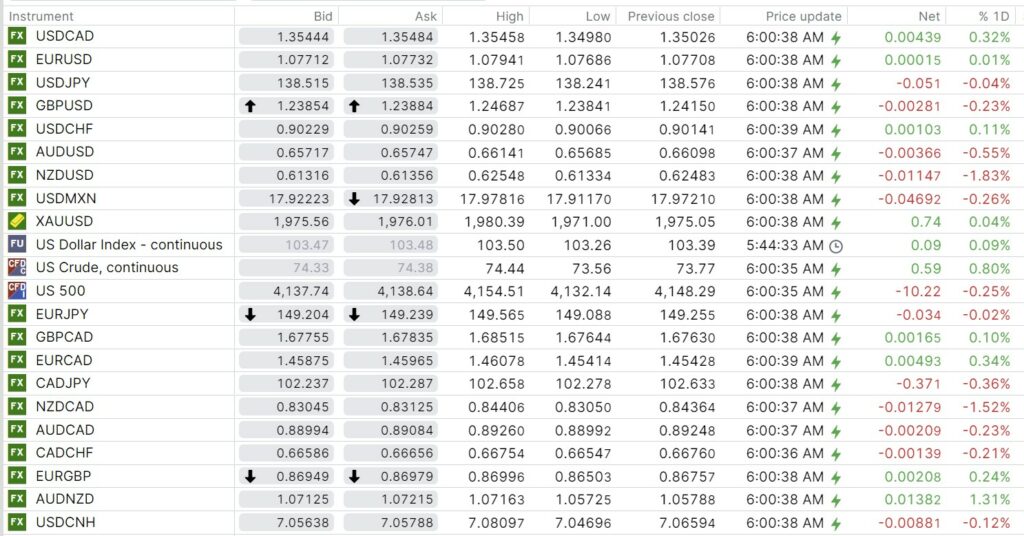

USDCAD Snapshot: open 1.3544-48, overnight range 1.3498-1.3558, close 1.3502.

USDCAD outperformed its antipodean cousins while remaining inside its one-week range but continued to drift higher in early NY trading

USDCAD gains were hampered by oil prices which rose after the Saudi Arabian energy minister hinted about new prices support measures to thwart short-sellers.

Recent domestic data (inflation, retail Sales and housing prices) has raised concerns that the BoC may be forced to hike rates at the June 7 meeting, although the odds of that happening are still low.

USDCAD has a modest bid, with direction at the whim of risk sentiment. S&P 500 futures are still edging lower in early NY trading.

There are no Canadian economic reports today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3490 looking for a break above 1.3580 to extend gains to 1.3620 then 1.3660. A break below 1.3490 targets 1.3440, then 1.3390. The downtrend from March comes into play at 1.3560, which if decisively broken, opens the door to a rally to 1.3860.

Longer term, USDCAD has been range bound (1.3220-1.3860) since October 2022

For today, USDCAD support is at 1.3470 and 1.3430. Resistance is at 1.3570 and 1.3610.

Today’s range 1.3480-1.3570

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

There is a dark cloud over financial markets which curtails activity. No one really believes that the US government will default but nevertheless, traders are adjusting positions “just in case.”

Traders are disappointed about the lack of progress in the debt ceiling negotiations and fear nothing will happen until after Memorial Day (May 29), which doesn’t leave much time before a June 1 default occurs.

The Reserve Bank of New Zealand provided excitement in Asia. They hiked rates by 25bps as expected, but knocked traders for a loop when they announced rates would remain at 5.5% until 2024.

The FOMC minutes from the May 4 meeting are released this afternoon amidst an ongoing debate about whether the Fed will hike or pause on June 14. Comments from a host of policymakers since the meeting suggest that the minutes will not provide new insight into the debate.

Asian equity indexes followed Wall Street lower. Japan’s Nikkei 225 index closed down 0.89% but it was the major Chinese equity indexes that suffered the most. Hong Kong’s Hang Seng index lost 1.62%.

European bourses opened in negative territory and continued to slide led by a 1.44% drop in the UK FTSE 100 index. S&P 500 futures are down 0.40%. The US 10-year Treasury yield is close to unchanged at 3.69%.

EURUSD is at the top of its 1.0749-1.0800 range although prices need to break above 1.0820 to negate downward pressure. The German Ifo Business climate index fell to 91.7 from 93.4 due to more pessimistic expectations and concerns ahead of summer. Nevertheless, broad US dollar demand is the main reason EURUSD suffers.

GBPUSD rallied to 1.2469 then dropped to 1.2366 after UK inflation rose 1.2% m/m in April. This is well above the forecast for an 0.8% increase. Annually, CPI rose 8.7% y/y, which was worse than expected but far better than the 10.1% level seen in March. The CPI data all but confirms that the BoE will raise rates by 0.25% in June 22.

GBPUSD technicals are bearish inside a downtrend channel bound by 1.2350 and 1.2490.

USDJPY fluctuated in a 138.24-138.73 band due to the higher US 10-year Treasury yield which is hovering around 3.70%,

AUDUSD traded in a 0.6562-0.6614 range overnight with prices weighed down by ongoing concerns about China’s economic rebound and US debt ceiling inspired risk aversion.

NZDUSD got sideswiped after the Reserve Bank of New Zealand announced that it was raising rates by 25 bps and then leaving them unchanged until the middle of 2024.

Analysts expected a hawkish statement due to still high inflation, and labour market pressures. The RBNZ didn’t see it that way. The statement said, “A pause would also allow more time to assess the impact of the significant tightening, and the timing of any further increase that might be needed.

There are no US economic reports today.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

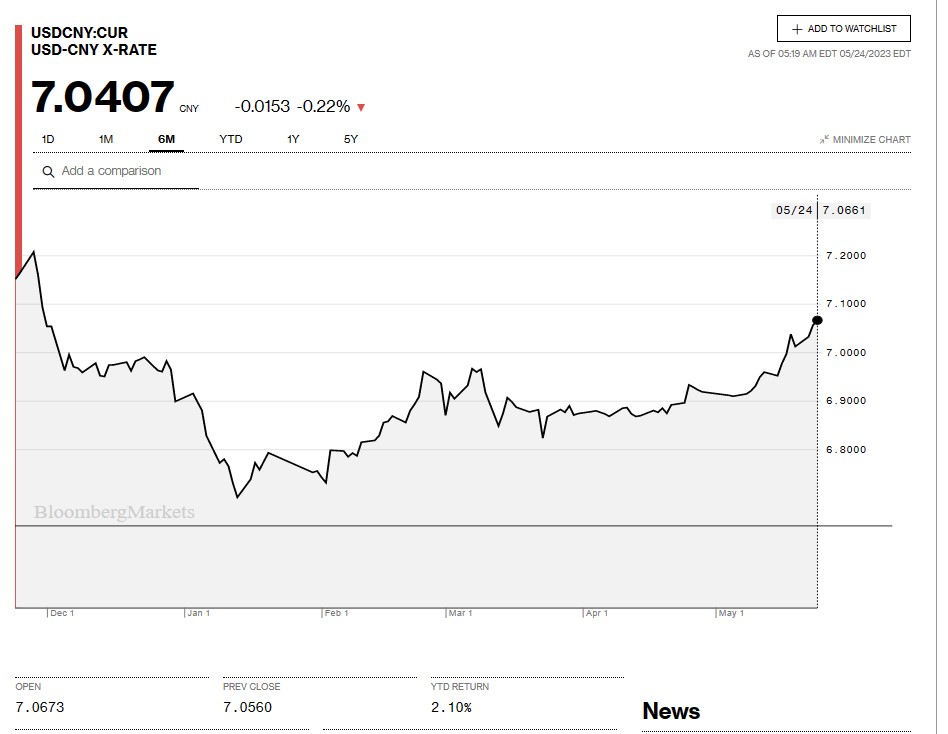

China Snapshot

Bank of China Fix: 7.0560, previous 7.0326

Shanghai Shenzhen CSI 300 fell 1.38% to 3859.09.

Chart: USDCNY 6 month

Source: Bloomberg