May 24, 2024

- US, UK and Australian markets closed on Monday.

- Canada March retail sales fall 0.2% y/y

- US dollar gains from yesterday recede overnight.

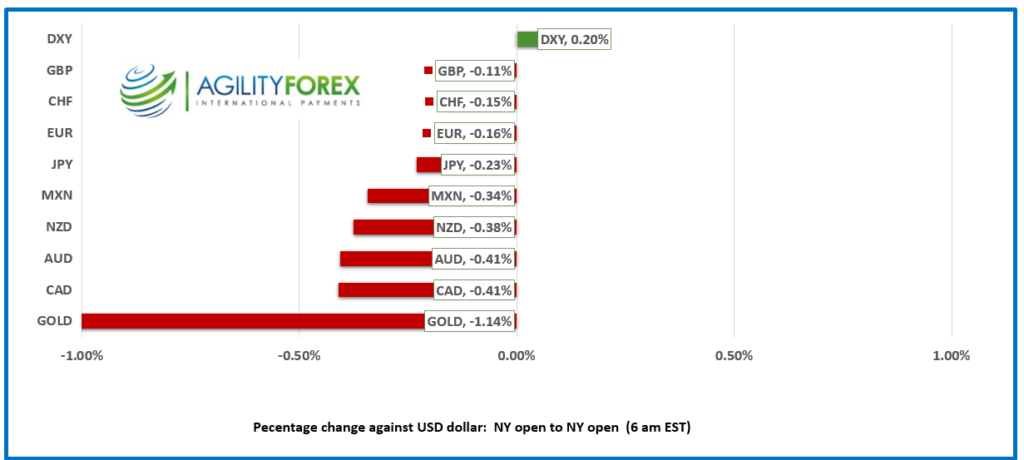

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3725, overnight range 1.3712-1.3740, close 1.3729

USDCAD rallied sharply yesterday after Fed comments and US economic data underscored the divergent Bank of Canada and Federal Reserve monetary policy outlooks. The BoC is set to cut rates in June while the Fed has no plans to cut rates before November.

USDCAD got additional support from WTI oil prices which dropped to 76.16 from 77.05 overnight to renewed concerns that unchanged US interest rates would stymie global growth. Opec plans a virtual meeting on June 2.

Canada retail sales were weaker than expected falling with retail sales ex-autos falling 0.6%m/m compared to the forecast for a 0.1% gain.

USDCAD Technicals

The intraday USDCAD technicals are bullish which was reinforced with the break above the 1.3695-1.3705 area yesterday and the subsequent spike to 1.3744.Instraday support is now at 1.3690 while resistance is at 1.3650.

The longer term technicals are bullish with the January uptrend line intact above 1.3600. Fibonacci retracement analysis suggests that a break above 1.3650 targets 1.3850.

For today, USDCAD support is at 1.3690 and 1.3660. Resistance is at 1.3750 and 1.3790. Today’s range is 1.3680-1.3750.

Chart: USDCAD daily

Source: DailyFX

“I’m a Believer”

It has taken a while, but it appears that traders are finally getting the Fed’s message that rates will remain at elevated levels for longer than previously thought, which was repeated by Atlanta Fed President Raphael Bostic yesterday. US economic data appeared to confirm his view. Weekly jobless claims fell by 8,000, which keeps the “strong labour market” story alive. That was followed by tier 2 S&P Global PMI data, which was stronger than expected.

“Out of your pajamas and into the office”

A number of large banks on Wall Street are demanding employees return to the office 5 days per week. One oft-cited reason is that employees are needed to revitalize the downtown core and provide much-needed support to the depressed office market. Another reason is that managers need workers to feed their insecurities. It’s hard to ruin your employees’ day because you are in a bad mood if they can tune you out by muting their laptop.

US long weekend will overshadow data.

It is the Memorial Day long weekend in America, and the focus will be on beaches, beer, and BBQs, not April Durable Goods Orders which rose 0..75 in April compared to the forecast for a -0.8% vs March 2.6%.

Michigan Consumer Sentiment is due later. (forecast 67.5 vs previous 67.4).

EURUSD

EURUSD has a modest bid, rising from 1.0805 in Asia to 1.0842 in NY. German Q1 GDP rose 0.2% q/q as expected. Prices got a bit of support after noted ECB hawk Isabel Schnabel warned policymakers need to exercise caution to prevent moving too fast on rate cuts.

GBPUSD

GBPUSD is trying to recoup yesterday’s losses and climbed from 1.2677 to 1.2722 in NY. The gain is supported by mildly better risk sentiment and by GfK Consumer Confidence data improving two points to -17 from -19 in April. The Client Strategy Director, Joe Staton, wrote, “There was another strong showing for the UK Consumer Confidence Index this month, driven by a jump in the outlook for our personal finances (up five) and a boost for our view on the wider economy in the coming year (up four).” Weaker-than-expected April Retail Sales data (actual -2.3% m/m vs forecast -0.4%) was largely ignored.

USDJPY

USDJPY traded in a 156.89-157.15 range supported by firmer US Treasury yields and expectations that US interest rates will remain elevated for most of 2024. Prices were also supported after Japan’s inflation rose less than it did in March (actual CPI 2.5% y/y vs March 2.7%), which may encourage BoJ policymakers to leave interest rates unchanged.

AUDUSD AND NZDUSD

AUDUSD is attempting to claw back yesterday’s losses and has risen from 0.6592 to 0.6619 in early NY as the US dollar gives up some gains against the majors. Monday is a holiday in Australia.

NZDUSD is at the top of its 0.6087-0.6112 range due to broad US dollar weakness. RBNZ Deputy Governor Christian Hawksby’s hawkish comments helped underpin the currency. He said rate cuts were not being discussed as other factors have to be dealt with before “shift(ing) that conversation to whether we should hold or cut.”

USDMXN

USDMXN consolidated yesterday’s gains in a 16.7026-16.7625 range. Slightly better than expected Q1 GDP data (actual 0.3% q/q vs forecast and previous reading of 0.2% q/q) is disappointing as it is further evidence that economic growth is waning while inflation inches higher (actual two-week inflation rate 0.29% vs 0.9% previously). Mexican April trade data is on tap.

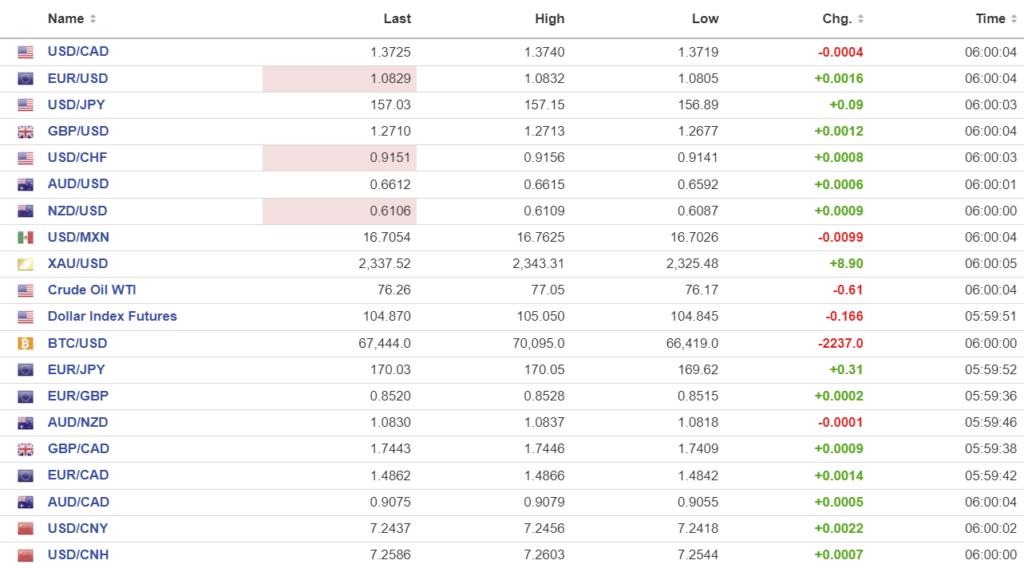

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

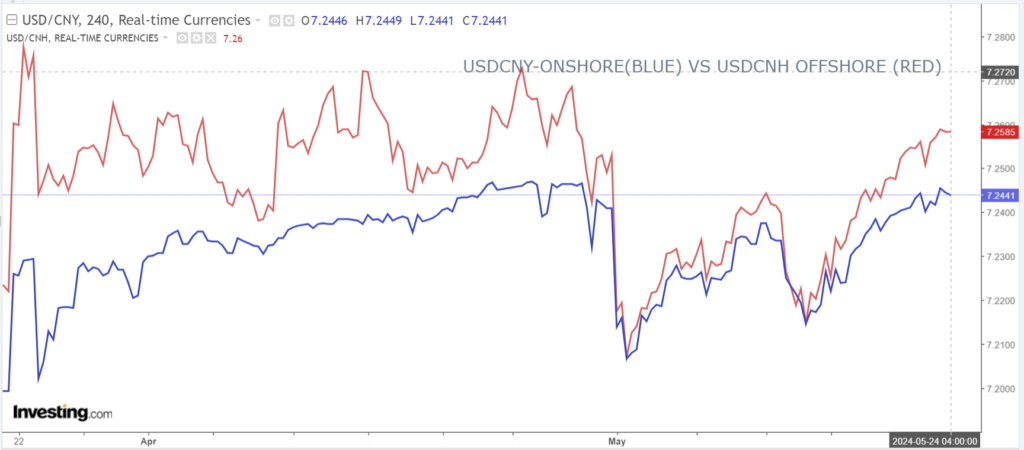

China Snapshot

PBoC fix: 7.1105 vs exp. 7.2539 (prev. 7.1098).

Shanghai Shenzhen CSI 300 fell 1.1% to 3601.48.

China is vying for the title of “World’s Worst Neighbor.” The Chinese defence ministry said it’s ongoing “punishment drills” were to allow the military to assess its capacity to “seize power” and occupy key areas, in line with Beijing’s ultimate goal of annexing Taiwan.

Chart: USDCNY and USDCNH

Source: Investing.com