Photo: HSclipartall.com

January 26, 2023

- US Q4 GDP, Durable Goods Orders, Jobless claims better than expected.

- Dovish Bank of Canada helps improve global risk sentiment.

- US dollar retreats across the board from yesterday’s open-CAD underperforms.

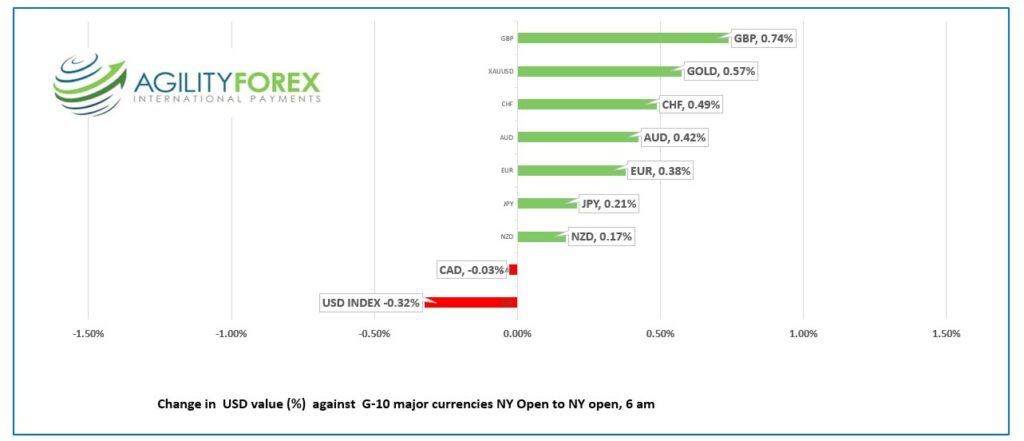

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3383-87, overnight range 1.3358-1.3406, close 1.3372

USDCAD whip-sawed in a 1.3340-1.3430 range yesterday after the dovish Bank of Canada rate hike. The BoC raised its policy rate by 25 bps to 4.5% and then said it was taking a break from further hikes. Governor Tiff Macklem was very clear saying “With today’s modest increase, we expect to pause rate hikes while we assess the impacts of the substantial monetary policy tightening already undertaken.”

When the dust settled, USDCAD remained comfortably inside its well travel 1.3340-1.3440 range with traders now waiting for the February 1, FOMC meeting.

USDCAD is also being undermined by firming oil prices. WTI has been grinding higher since the start of the year and the intraday technicals are bullish above $79.70/b. Oil prices are underpinned by fresh hopes of rebounding demand from China after travel in the mainland returned to pre-pandemic levels.

The Canadian economic calendar is empty.

USDCAD Technical Outlook

The USDCAD technical picture is unchanged. The downtrend from the start of the year is intact while prices are below 1.3450, but it faces strong support in the 1.3310-40. A break below 1.3310 targets 1.3230 while a topside breach above 1.3450 shifts the focus to 1.3600.

For today, USDCAD support is at 1.3310 and 1.3280. Resistance is at 1.3380 and 1.3420.

Today’s range 1.3310-1.3380

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The US data has spoken. The economy is resilient, a soft landing is possible although growth is slowing.

US Q4 GDP slowed to 2.9% y/y from 3.2% previously, but well above the 2.6% that was expected.

Durable Goods Orders rose 5.6% in December and Durable goods, ex-Defense rose 6.3%. Both results were higher than the consensus forecast.

Weekly jobless claims fell 6,000 to 186,000 in the week ending January 20, better than the forecast of 205,000.

S&P 500 futures gained, the US dollar churned, and the US 10-year Treasury yield inched higher to 3.511% from 3.4474% earlier.

The Bank of Canada decision yesterday opened eyes around the world. The BoC’s announcement that it was pausing rate hikes was seen as a glimmer of hope that other central banks would follow suit, particularly the Fed.

The ECB is in the early stages of a tightening program and anyone believing the Fed will stop hiking rates before fed funds hits 5.0% is delusional.

Nevertheless, global stock indexes are grinding higher, and the US dollar is on the defensive. In Asia, Hong Kong’s Hang Seng reopened after a four-day break and surged 2.37% higher. Japan’s Nikkei 225 index closed with a small 0.12% loss.

European bourses are in positive territory. The French CAC 40 index is up by 0.77% while UK FTSE gained 0.32%.

Russian fired a barrage of missiles into Ukraine as Putin expresses displeasure at the US and Germany decision to deliver high-tech tanks to Ukraine. India is doing its bit to support Russia (while pretending to be a western ally) by buying all the heavily-discounted Russian crude they can get.

The US dollar index peaked in September and a slow decline turned into a sharp fall in November and continued into January. USDX snapped the June 2021 uptrend line on January 12 which sets the stage for further weakness to 99.00.

EURUSD traded with a bit of a bid in a 1.0894-1.0929 range in anticipation of a hawkish ECB monetary policy meeting on February 2. Analysts are expecting the ECB to raise rates by 50 bps next week and again in March.

GBPUSD consolidated yesterdays gains in a 1.2376-1.2429 range. The BoC monetary policy meeting is February 2 and a 50 bp hike is expected. Some analysts are warning of GBPUSD weakness if the BoE expresses caution about the need for further rate hikes.

USDJPY traded in a 129.03-129.99 range with the low seen in Asia. The BoJ Summary of Opinions said it was appropriate to keep existing monetary polices and the YCC cap.

AUDUSD drifted in a 0.7094-0.7127 due to a mildly weaker US dollar. Volumes were light due to the Australian Day holiday. NZDUSD traded quietly as well, in a narrow 0.6472-0.6501 range.

Today’s US data dump includes Chicago Fed National Activity Index, Weekly Jobless Claims, Durable Goods Orders, Q4 GDP, Wholesale Inventories, New Home Sales, and Personal Consumption Expenditures Prices.

Chart of the Day: US Dollar Index (USDX) daily

Source: Saxo Bank

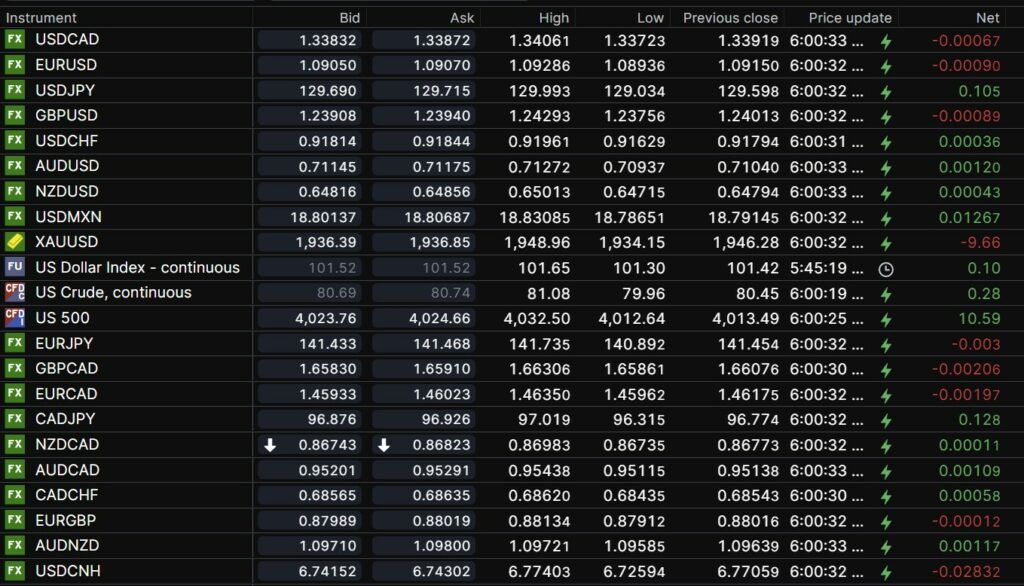

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Closed Lunar New Year Bank of China Fix: Jan. 20,2023, 6.7702, previous 6.7674.

Shanghai Shenzhen CSI 300 closed 4181.53. 20Jan23

In first four days of China Lunar New Year (Sat.-Tues) China passenger trips (road, rail, air, and water) were close to 98 million, 29% higher than last-year, thanks to repealed covid restrictions.

Chart: USDCNH (off-shore) one month

Source: Bloomberg