September 16, 2021

Wall Street poised to open with gains, European Equity indexes are higher

US data beats expectations, gives greenback a bid

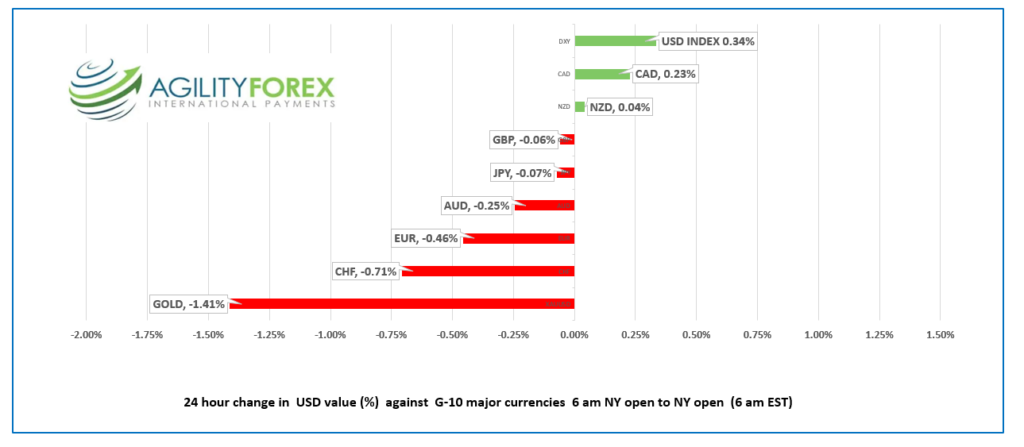

US dollar opens with gains compared to yesterday, CAD outperforms

FX at a Glance:

Source: IFXA/RP

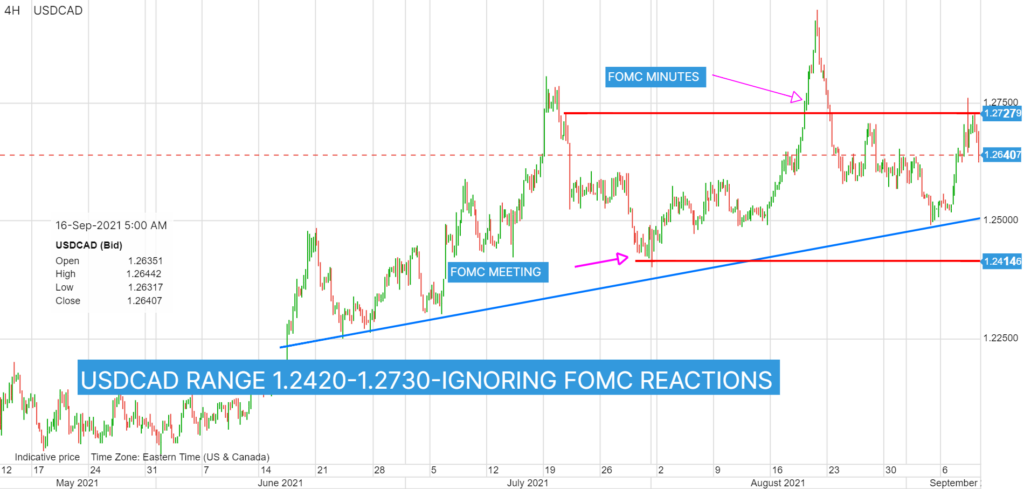

USDCAD Snapshot Open 1.2640-44, Overnight Range 1.2619-50, Previous close 1.2625

USDCAD is consolidating yesterday’s losses, albeit with a modestly bullish bias. USDCAD dropped from 1.2693 just before Canada CPI on Wednesday to close at 1.2625. Statistics Canada noted “Consumer Price Index (CPI) rose 4.1% on a year-over-year basis in August, the fastest pace since March 2003, up from a 3.7% gain in July. The increase in prices mainly stems from an accumulation of recent price pressures and from lower price levels in 2020.” Analysts are beginning to believe that inflation may be less transitory than what the Bank of Canada believes.

The USDCAD slide got an assist from rising WTI oil prices, which rose from $71.07/barrel to $73.06/b. Prices have since slid to $72.22/b in early NY trading

Global risk sentiment turned mixed overnight, which limited USDCAD losses. USDCAD is modestly higher following better than expected US retail Sales and Philadelphia Fed data.

Technical view: The intraday USDCAD technicals are bearish below 1.2660, looking for a break of 1.2600 to extend losses to 1.2550. Since the end of July, the price action is just noise. USDCAD is bouncing in a 1.2420-1.2730 range, if you ignore the short-term moves following the FOMC meeting and then the minutes. A break either side of that range will provide direction for the next 0.0300 points.

For today, support is at 1.2610 and 1.2580. Resistance is 1.2670 and 1.2710. Today’s range 1.2610-1.2770

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar started the NY session with gains against the G-10 majors except against NZD and CAD. It would appear that dollar buying because of prospects for fiscal stimulus overwhelmed dollar selling due to proposed tax hikes.

US Retail Sales rose 0.7% in August, easily beating the forecast for an 0.8% m/m decline. Retail sales ex-autos soared 1.7% m/m, well above predictions for a -0.2% drop. Jobless claims were steady at 332,000. The Philadelphia Fed Manufacturing Survey expanded 111 points to 30.7.

The greenback extended its overnight gains following the news. S&P 500 futures inched higher and 10-year Treasury yields rose to 1.336% from 1.304%. Gold prices extended their slide and dropped to $1759.95.

Asia stock markets underperformed thanks to another large Chinese property developer, Country Garden, reporting financial difficulties. Traders were already nervous due to China’s regulatory clampdown. European stock markets are trading rose overnight and held on to gains post-US data.

Geopolitical tensions continue to ripple in Asia. Australia, UK, and the USA announced a security partnership to counteract China’s military aspirations which irked Beijing.

EURUSD traded in a 1.1806-1.1820 band in Asia then dropped to 1.1753 in after the US retail sales report. Broad US dollar demand combined with ongoing dovish ECB speak, and bearish technicals weighed on prices. ECB policymaker Olli Rehn said the ECB will “gradually transition from crisis measures.” The intraday technicals are bearish looking for a break of 1.1750 to extend losses to 1.1700.

GBPUSD peaked at 1.3851 in Asia then drifted steadily lower before to 1.3802 on broad US dollar strength in NY trading. The downside may be limited due to signs the UK economy continues to rebound. The recent spike in UK inflation supports a hawkish bias for the Bank of England.

USDJPY consolidated recent losses and traded in a 109.22-109.45 range. The drop in US Treasury yields drove USDJPY to 109.10 yesterday and but the post data Treasury yield bounce lifted USDJPY to 109.70.

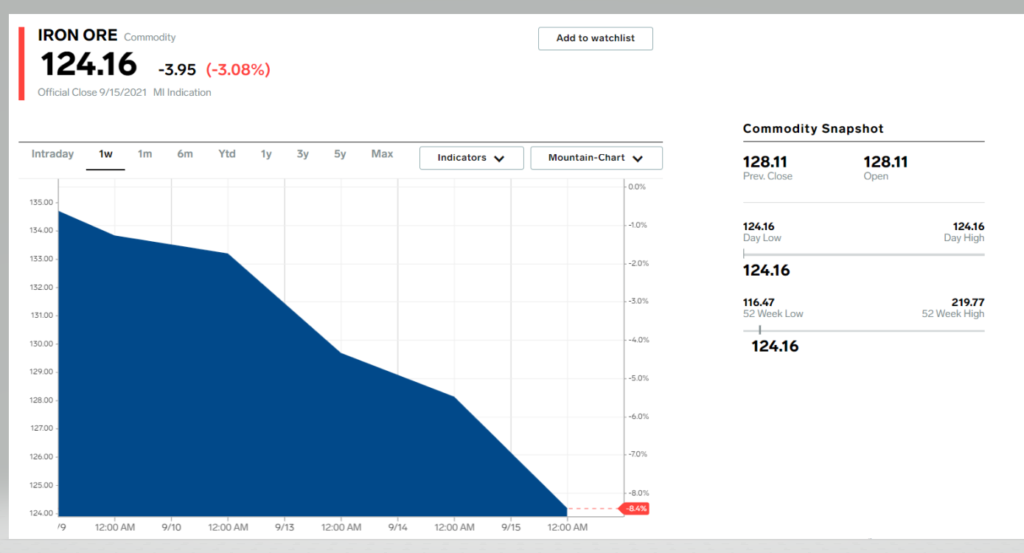

AUDUSD suffered from a weak employment report which is distorted because of COVID-19 lockdown measures and broad US dollar strength. AUDUSD is also weighed down by the dovish RBA outlook and falling iron ore prices. NZDUSD rallied after Q2 GDP rose 2.8% q/q, beating the forecast for a 1.8% q/q increase. The gains didn’t last, and prices dropped from 0.7138 to 0.7103.

Chart of the Day- Iron ore, one week

Chart: Markets.businessinsider.com

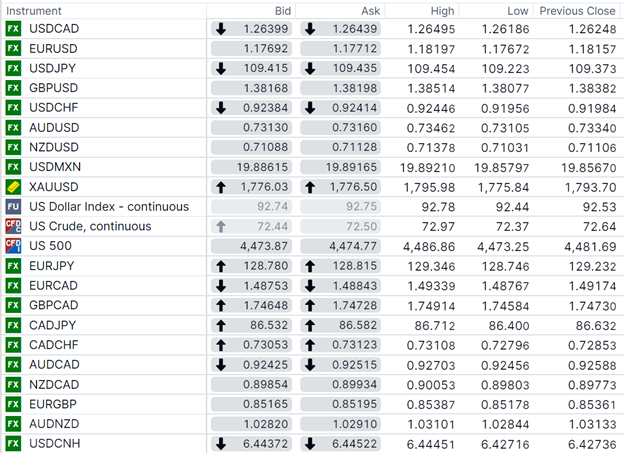

FX open, high, low, previous close

Source: Saxo Bank

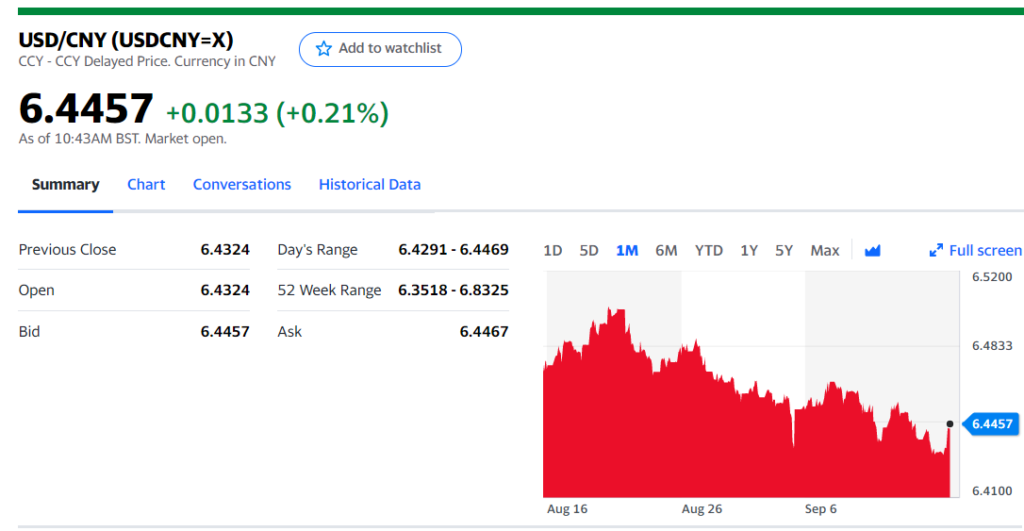

China Snapshot

Today’s Bank of China Fix, 6.4330, Previous 6.4492

Shanghai Shenzhen CSI 300 index fell 1.22% to 4807.70

Green Garden property developer adds to real estate financial woes, while the ongoing regulatory crackdown weighs on stocks.

Traders were also spooked by news Australia, UK and USA have a defence partnership to counter China.

Chart: USDCNY 1 month

Source: Yahoo Finance