Photo: wikimedia commons

- US GDP and jobless claims better than expected

- Oil prices extend this week’s gains

- US dollar opens mixed, CAD unchanged

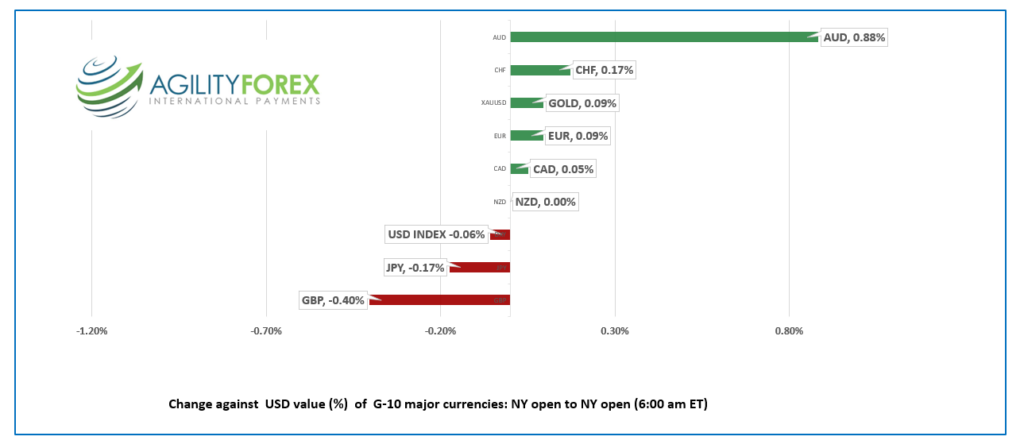

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3616-20, overnight range 1.3573-1.3637, close 1.3613

USDCAD traders largely ignored the November inflation data, which at 6.8%, was a tick lower than the October reading, but above expectations. The next CPI report is January 15, and the level and trend of inflation will determine if the BoC hikes rates at the January 25 meeting.

And oil prices will play a key role in the decision.

WTI oil prices climbed 8.9% since last Friday’s low. Fibonacci retracement analysis from the November peak of $93.45, suggest a decisive break above $79.10 may seen an extension to $88.00. Prices retreated to $78.85/b in NY after the US data.

Traders are expecting renewed demand supported by China accelerating the easing of covid measures. Beijing announced an end to quarantines for travellers starting in January. Prices are also supported by yesterday’s EIA report showing crude inventories fell 5.9 million barrels.

USDCAD popped to its session peak after better-than-expected US data.

USDCAD technical outlook.

The intraday technicals are unchanged from yesterday. Bullish. USDCAD is bullish above 1.3550, looking for a break above 1.3650 to extend gains to 1.3700. A move below 1.3550 targets 1.3510.

The uptrend that has been intact since August comes into play at 1. 3440.

For today, USDCAD support is at 1.3570 and 1.3540. Resistance is at 1.3640 and 1.3690

Today’s range 1.3560-1.3640

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Traders reacted to this mornings higher than expected US Q3 GDP by lifting the US dollar, selling S&P 500 futures, and boosting the US 10-year treasury yield to 3.677% from the overnight low of 3.63%.

The Bureau of Economic analysis wrote “Real gross domestic product (GDP) increased at an annual rate of 3.2 percent in the third quarter of 2022. In the second quarter, real GDP decreased 0.6 percent.” They said, “the increase reflected increases in exports, consumer spending, non-residential fixed investment, state and local government spending, and federal government spending, that were partly offset by decreases in residential fixed investment and private inventory investment.”

In addition, Initial Jobless claims rose 2,000 to 216,000 last week the news was overshadowed by the GDP data.

Overnight, traders were reluctant to get involved as the holidays and year end curtailing activity.

Yesterday, positive sentiment from news US consumer confidence increased to 108.3 from 101.4 in November was offset by a 7.7% decline in existing home sales in November.

It didn’t stop bottom pickers from lifting the S&P 500 index 1.5%. The positive mood from Wall Street spilled over into Asia. Hong Kong’s Hang Seng soared 2.71% spurred by China easing covid restrictions further and rebounding property developer fortunes. Australia’s ASX 200 rode higher commodity prices to a 0.53% gain.

European stocks are trading in negative territory except for the UK FTSE 100 which has gained 0.35%. S&P 500 futures extended overnight losses and are down 1.09%, post US GDP (6:00 am PT). Gold (XAUUSD) is down 0.36% from Wednesday’s close.

Russia and the West tensions are elevated after the US agreed to send a Patriot surface-to-air missile system to Ukraine as part of a $1.85 billion military assistance package. A Russian spokesman said the Patriot system would not help end the war and claimed the US was fighting a proxy war with Russia.

EURUSD is drifting in a 1.0606-1.0659 range. With traders ignoring today’s US economic reports. ECB board member Mario Centeno said inflation data suggested that inflation shows signs of peaking in Q4 2022. However, his colleague Luis de Guindos contradicted him by insisting rates need to increase at their current pace for a “period of time.”

GBPUSD slumped to 1.2023 in NY after peaking at 1.2146 in Asia. Stronger than expected US GDP combined with weaker than forecast UK GDP (actual 1.9% y/y vs forecast 2.4% y/y) weighed on prices.

USDJPY is at the top of its 131.65-132.49 range due to renewed US dollar demand and ahead of Japan’s inflation report tomorrow.

AUDUSD dropped to 0.6697 following the US data after touching 0.6766 overnight. The initial gains came after China made an effort to improve its relations with Australia.

NOTE: The final Loonieviews for 2022 is December 23.

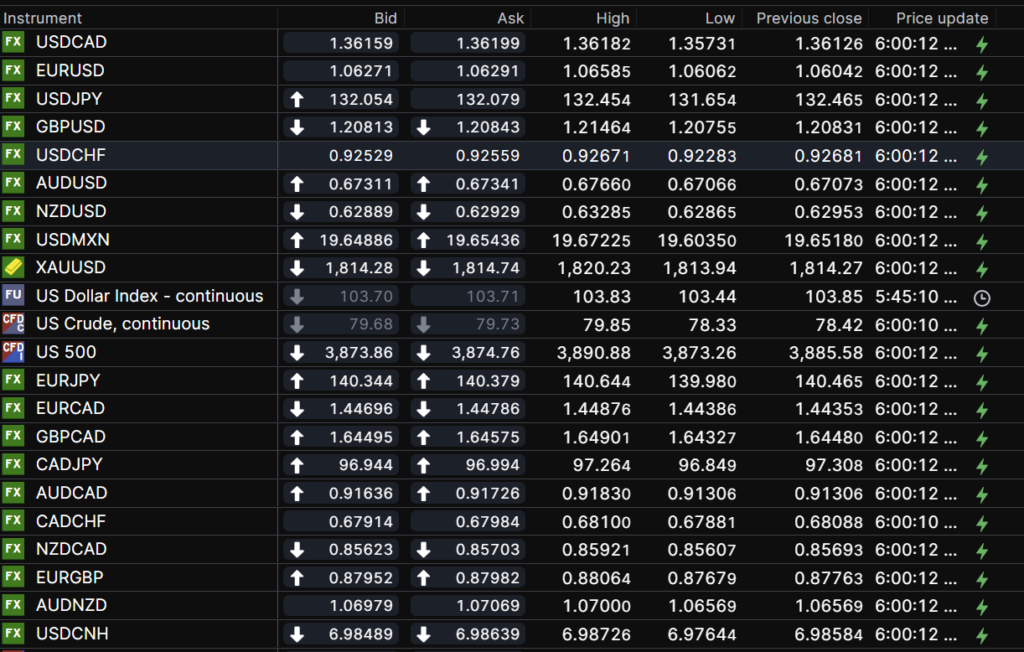

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

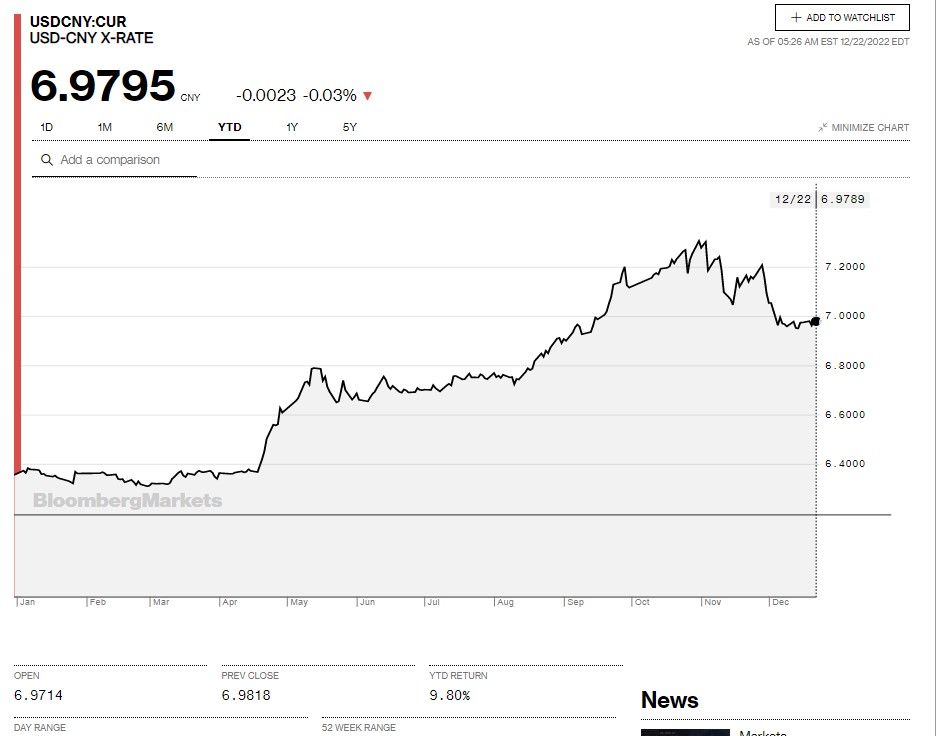

China Snapshot

Today’s Bank of China Fix: 6.9713, previous 6.9650

Shanghai Shenzhen CSI 300 rose 0.14% to 3836.03

Chart: USDCNY year-to-date

Source: Bloomberg