Source: Wikimedia Commons

- Opec may announce more aggressive production cuts today

- NZDUSD traders shrug off RBNZ 50bp rate hike

- US dollar opens mixed from yesterday, equities retreat, US 10-year yield 3.70%

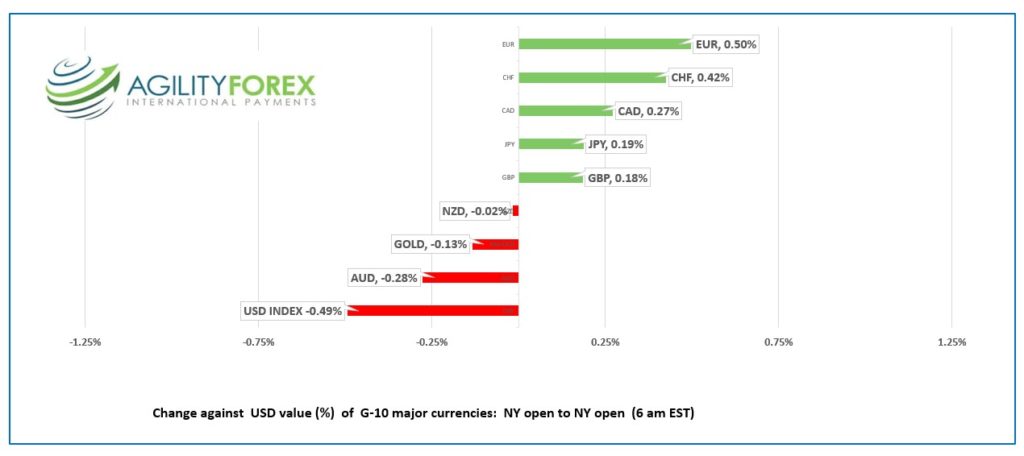

FX at a glance:

Source: IFXA Ltd/RP

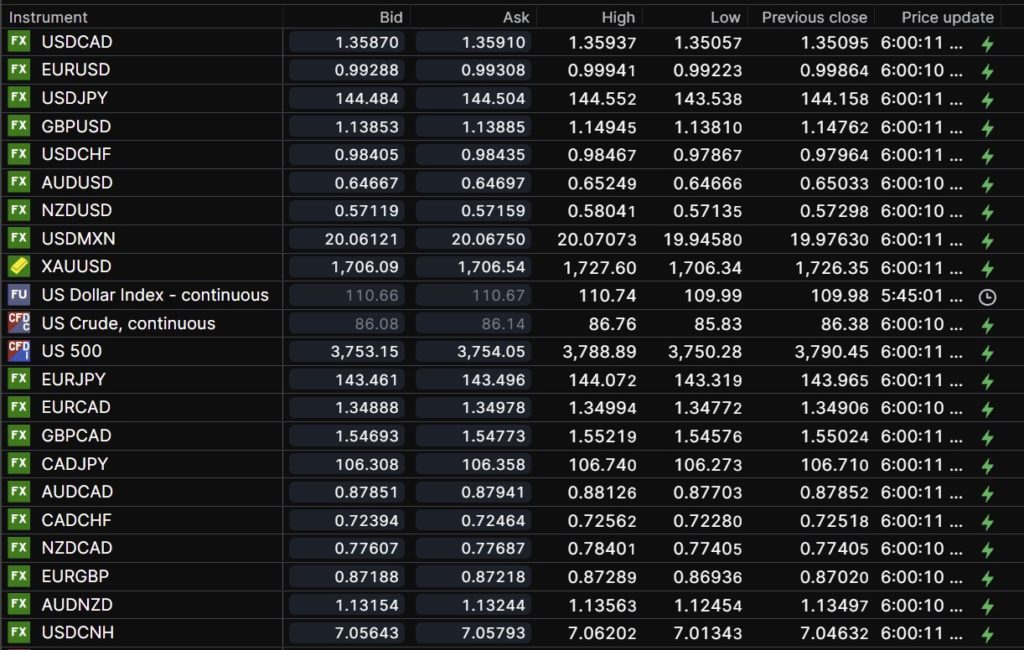

USDCAD Snapshot: open 1.3587-91, overnight range 1.3506-1.3622, close 1.3510

USDCAD closed at the low yesterday then traded sideways in Asia. Prices accelerated higher rising from 1.3510 to 1.3598 in early NY trading with the gains fueled by higher US treasury yields and a rebounding US dollar against the major G-10 currencies.

WTI oil prices consolidated this week’s gains in a $85.83-$87.33/barrel range and are trading at $86.47/b in NY. Opec is expected to announce it is cutting actual production (rather than quotas) by 2.0 million barrels/day to shore up what Opec feels is a mis-priced market. The move is welcomed by Vladimir Putin, which should raise the ire of American authorities.

Canada’s trade surplus narrowed to $1.5 billion in August from $2.37 billion in July. Building Permits surged to 11.9% from a drop of 7.3% in July.

USDCAD Technical outlook

The intraday technicals are turned bullish with today’s move above 1.3605 which was the downtrend line from Monday’s peak, and it sets up a test of resistance in the 1.3670 area. A topside break targets 1.3790, while a move below 1.3540 suggests a retest of 1.3505. A decisive break below 1.3490 targets 1.3400.

For today, USDCAD support is at 1.3570 and 1.3510. Resistance is at 1.3630 and 1.3670. Today’s range: 1.3560-1.3650

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The answer to yesterday’s “correction or trend change” question is correction.

The greenback rallied overnight, knocking gold prices and equity indexes lower, supported by the US 10-year yield climbing to 3.71%, from 3.637% at yesterdays close.

Yesterday, traders decided that the Fed and other central banks will slow the pace of rate hikes to avoid unnecessarily damaging the economy. The view got some traction after the JOLTS report said job openings fell to 10.1 million. It was the fourth decline in five months and cited as evidence that the job market is cooling.

The JOLTS data helped accelerate the dollar’s decline which was already under pressure due to rebounding equity prices. Wall Street closed sharply higher led by a 3.54% rally in the Nasdaq.

But that was yesterday.

Traders are re-assessing the recent equity and US dollar moves. The odds that the Fed will announce any deviation from its planned rate hike path took a further hit after two Fed officials reiterated policymakers’ determination to drive inflation down to its 2.0% target.

Fed Governor Philip Jefferson said “Restoring price stability may take some time and will likely entail a period of below-trend growth. I want to assure you that my colleagues and I are resolute that we will bring inflation back down to 2% … We are committed to taking the further steps necessary.”

San Francisco Fed President Mary Daly dispensed with the idea the Fed would temper rate increases to avoid creating hardships in other countries saying “the Fed’s mandate is to achieve U.S. price stability and full employment, and that’s what the Fed is focused on.

Traders who didn’t think the Russian/Ukraine war had any bearing on the day-to-day life in America got a wakeup call from the Russian Ambassador to the US Anatoly Antonov.

He used the Telegram messaging app to warn that military aid to the Ukraine is “an immediate threat to the strategic interests of our country. The supply of military products by the U.S. and its allies not only entails protracted bloodshed and new casualties, but also increases the danger of a direct military clash between Russia and Western countries.”

That statement took the bloom off the risk seeking rose overnight as did reports Opec may cut actual production (not quotas) by 2.0 million/barrels/day.

The US ADP employment change report showed a gain of 208,000 jobs in September, a tad better than the 200,000 forecast and higher than the 185,000 in August. The results suggest the Fed will be in no hurry to slow the pace of rate hikes.

EURUSD traded sideways in Asia then dropped from 0.9994 to 0.9893 in NY as negative Eurozone sentiment returns to the forefront. Eurozone and German composite and services PMI reports were weaker than expected. The EU is expected to announce a cap on Russian oil and other sanctions against Russia in retaliation for Russia’s “illegal” referendums in Ukraine.

GBPUSD peaked at 1.1495 in Europe then dropped to 1.1306 in NY after UK composite and services data The S&P Global statement said, “September data pointed to a loss of momentum for the UK service sector, with an 18-month period of output expansion coming to an end amid falling volumes of incoming new work. Shrinking client demand was widely attributed to pressure on household budgets from escalating inflation, alongside widespread pessimism about the economic outlook.

USDJPY found a bottom at 143.54 in early Asia trading then climbed steadily to 144.55 on the back of rising US Treasury yields.

NZDUSD traded erratically. Prices climbed from 0.5708 at the Asia open to 0.5804 following the RBNZ 50bp rate hike which takes the Overnight Cash Rate to 3.5%. The move was expected, but policymakers did not mention anything about slowing the pace of hikes. Prices retreated to 0.5688 in early NY.

US ISM Services data is ahead.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: Closed: previous 7.0998

Shanghai Shenzhen CSI 300 closed

NOTE: Chinese markets closed next week for Golden Week.

Chart: USDCNH (offshore) 1 month

Source: Saxo Bank