February 20, 2024

- China PBoC cuts 5yr LPR by 25 bps, 1-yr unchanged

- Canada inflation falls to 2.9% y/y.

- US dollar drifting lower-NZD outperforms

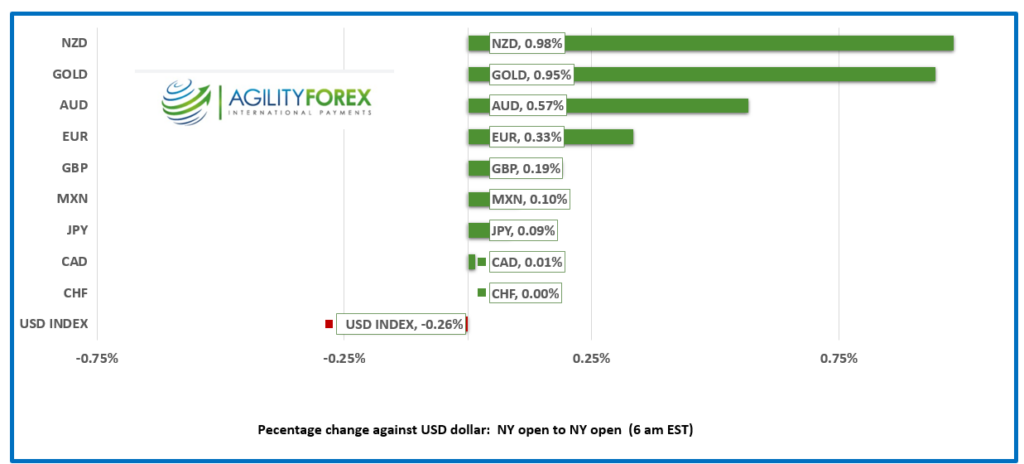

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3477-81, overnight range 1.3476-1.3516, close 1.3491

USDCAD started today’s session where it started on Friday, then popped from 1.3476 to 1.3516 on the heels of a cooler than expected January inflation report. January CPI headline inflation dropped to 2.9% from 3.4% in December (forecast 3.3%) is expected to be 3.3% y/y. The USDCAD reaction to the slightly cooler reading has everything to do with weak short position covering and nothing to do with an anticipated Bank of Canada reaction. That’s because Governor Macklem and his crew are looking for evidence of a sustainable decline in inflation and today’s data is not evidence, just a good start.

The latest oil price rally stalled at $79.28 at the end of the day on Friday and prices have dropped to $77.54/b today. The latest PBoC rate cut is viewed as further evidence of China’s economic woes which suggests weaker crude demand.

USDCAD Technicals

The intraday USDCAD technicals are looking to break out. The symmetrical triangle on the 4 hour chart suggest a move above 1.3520 will extend gains to the 1.3600 area while a break below 1.3470 targets 1.3370.

Longer term, USDCAD is shuffling between the 100 and 200 day moving averages and between the 10 day Bollinger bands (1.3410 and 1.3550).

For today, USDCAD support is at 1.3470 and 1.3410. Resistance is at 1.3530 and 1.3580. Today’s range is 1.3460-1.3550.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The US and Canada return from an extended weekend to markets struggling for direction against a backdrop of rising geopolitical tensions.

The Chinese navy is creating havoc in the South China Sea. They boarded a Taiwanese tourist boat to intimidate passengers and then complained when the US and Philippines conducted joint air and sea drills.

Meanwhile, Israel is ignoring demands for a ceasefire until they can exterminate Hamas hiding in tunnels beneath nursery schools and hospitals in Rafah. Houthi rebels managed to damage a Belize-flagged ship in the Red Sea. And the world turns.

The PBoC cut its 5-year Loan Prime Rate by 25 bps to 3.95% and the global market reacted with a collective yawn. Traders only want to know when the Fed will start cutting rates.

Asian equity indexes closed modestly lower, except for the Chinese indexes which saw tiny gains. European bourses are slightly higher except for the German Dax which is down 0.20%. S&P 500 futures are down 0.40% while the US 10-year Treasury yield is steady at 4.277%.

The US economic calendar does not have any top-tier data.

EURUSD traded in a 1.0762-1.0810 range and is at the top of its 2-week trading band. Broad US dollar weakness from last week’s US stock market rally is supporting prices. Traders ignore the Bundesbank’s monthly report which suggested that Germany entered a technical recession at the end of 2023 and the economy may continue to slow in Q1 2024.

GBPUSD see-sawed in a 1.2579-1.2616 band and is near the bottom in early NY trading. The currency pair is awaiting a fresh catalyst which may occur with the release of February PMI data on Thursday. Until then, the two-week-old 1.2520-1.2680 range will guide price action. BoE Governor Andrew Bailey said it expects CPI to hit its target this year and that the economy is showing signs it is picking up.

USDJPY is steady in a 149.88-150.44 range. Prices continue to be boosted by last week’s jump in US Treasury yields and the comments by BoJ Governor Ueda suggesting if rates rise it would be a case of “one and done.” USDJPY gains are limited by concerns about BoJ intervention.

AUDUSD traded firmer in a 0.6521-0.6562 range with prices getting a bit of a boost from the PBoC rate cut and the minutes of the RBA meeting on February 6. The minutes revealed a hawkish bias as policymakers considered hiking rates but chose to leave them unchanged due to uncertainty around the outlook.

USDMXN traded in a 17.0213-17.0695 range overnight with traders awaiting Thursday’s release of Q4 GDP, H1-February CPI data, and the Banxico monetary policy meeting minutes. The data is not expected to give Banxico reason to cut rates

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: closed 7.1068, expected 7.2018, Monday 7.1032

Shanghai Shenzhen CSI 300 rose 0.21% to 341.85, closed- Feb. 8/24- 3364.93.

The PBoC surprised markets with a 25 bps cut to the 5-year Loan Prime Rate (LPR) to 3.95%, while leaving the 1-year LPR unchanged. Some analysts see the move as a precursor to more aggressive stimulus down the road. The stock market reaction suggests investors were not impressed.

Chart: USDCNH daily

Source: Bloomberg