Photo: HDClipart.com

- China trims interest rates to combat faltering growth

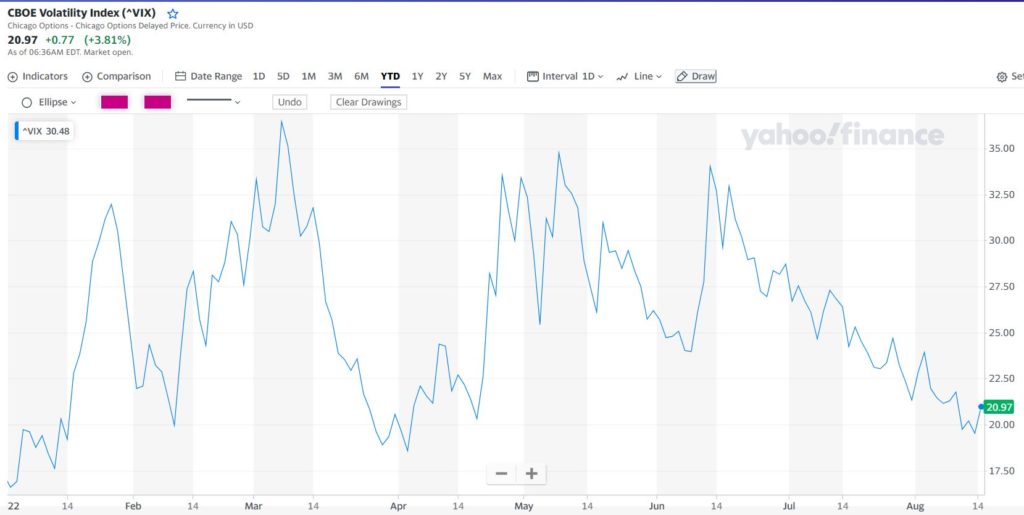

- CBOE Volatility Index (VIX) below March lows

- US dollar surges on broad safe-haven demand

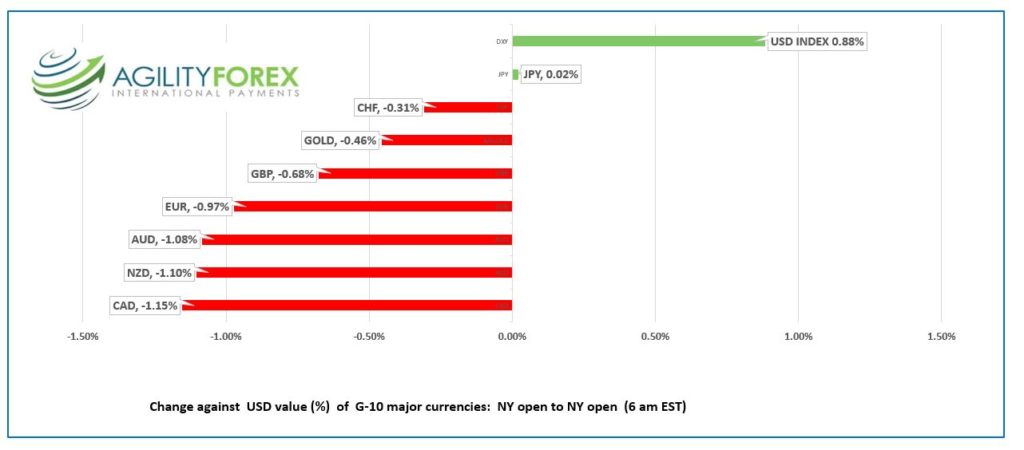

FX at a glance:

Source: IFXA Ltd/RP

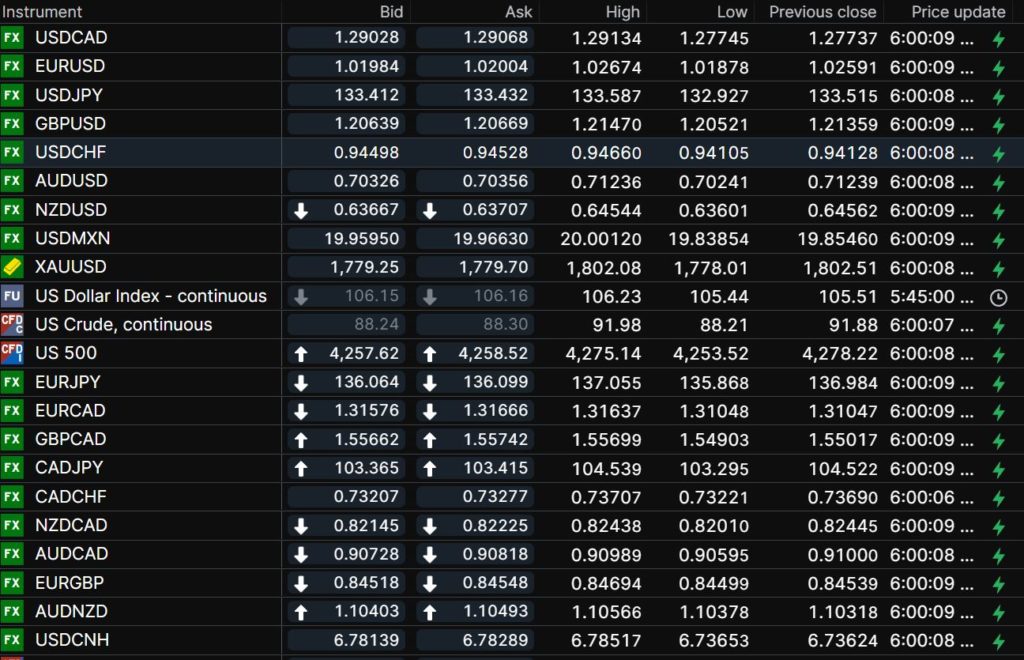

USDCAD Snapshot: open 1.2903-07, overnight range 1.2775-1.2919, close 1.2774

USDCAD rallied from the open in Asia and continued unabated until just before NY opened. The gains were due to broad US dollar demand sparked by China’s interest rate cut with the 4.6% plunge in WTI oil prices just adding insult to injury.

USDCAD direction is highly correlated with the S&P 500 and that stock index is showing signs of stress as momentum indicators are extremely overbought, suggesting a steep correction to 4120 is almost inevitable.

WTI oil prices dropped from $91.98/barrel to $87.42 on the back of broad US dollar strength and talk that the US and Iran may announce another Nuclear deal. If so, Iran would ultimately add another 4 million b/day of crude into global markets.

Canada Manufacturing Sales fell 0.8% m/m a tick below the forecast -0.9% m/m (previous -2%) Wholesale Sales were worse than expected rising just 0.1% m/m (forecast 0.5%, previous 1.6% m/m). The data merely adds more fuel to the Canadian economic slowdown story.

USDCAD Technical outlook

The USDCAD technicals are after breaking above resistance in the 1.2830-50 area and looking to continue the trend with a decisive break above the 1.2890-00 area (4 hour chart). If sustained, USDCAD would target the 1.2990-1.3005 zone, then 1.3080. A move below 1.2840 suggests further 1.2720-1.2900 range trading.

For today, USDCAD support is at 1.2850 area, and 1.2810. Resistance is at 1.2930 and 1.2960. Today’s range: 1.2870-1.2940

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Chinese spin doctors were hard at work writing today’s National Bureau of Statistics press release. The NBS report extolled the virtues of the ruling elite, saying, “under the strong leadership of the Central Committee of the Communist Party of China (CPC) with Comrade Xi Jinping at its core, all regions and departments adhered to the general principle of pursuing progress while maintaining stability. It went on to list seven weaker than expected economic stats underscoring the fact that the ruling elite and Comrade Xi Jinping are inept.

The Peoples Bank of China (PboC) trimmed the one-year Medium Term Loan facility and the 7-day reverse repo rates by 10 basis points in the wake of weaker than expected Industrial Production and Retail Sales data.

The news set the stage for a somewhat subdued, risk-averse overnight session with the US dollar in demand.

Asian stock markets closed with modest gains. Japan’s Nikkei 225 index shrugged off weaker than expected GDP data and gained 1.14%, while Australia’s ASX 200 climbed 0.45%. The major Chinese equity markets fell modestly.

European bourses are trading with a lack of conviction and are close to unchanged. S&P 500 futures and DJIA futures are down around 0.55%. WTI oil prices dropped 4.58%, while gold lost 1.35%. The US 10 year Treasury yield is sitting at 2.833%.

Even so, the CBOE Volatility index, the so-called fear index, shows equity traders have no fear. Everything is sunshine and unicorns, reflected by the VIX trading just above the year-to-date low.

EURUSD traded in a 1.0187-1.0267 range after trading sideways in Asia and then dropping in Europe.

China’s rate cut precipitated a rash of US dollar buying, and the single currency was not immune. German Wholesale price data was a nonfactor as EURUSD remained pressured by ECB/Fed interest rate outlooks and the German and European energy crisis, which will not be resolved until the Russia/Ukraine war plays out. EURUSD remains bearish below 1.0270, with a decisive move below 1.0180 targeting 1.0105.

GBPUSD traded defensively in a 1.2052-1.2147 range and is currently sitting at 1.2084 in NY. GBPUSD is beset with a litany of woes, from Brexit to government incompetence. Tuesday’s CPI, PPI, Retail Price Index, and House Price index data are likely to exacerbate downside risks. A break below 1.2050 will extend losses to 1.1950.

USDJPY rallied from 132.97 to 133.59 due to broad US dollar demand following the PboC rate cut, modestly higher US Treasury yields, and weaker than expected Japanese GDP data (actual 2.2% y/y vs forecast 2.5%).

AUDUSD dropped to 0.7024 from 0.7124 following the PboC action and soft Chinese data. Traders are looking ahead to the release of the RBA minutes from the July 5 meeting.

NZDUSD is trading near the bottom of its 0.6358-0.6454 due to broad US dollar demand and ahead of the RBNZ monetary policy meeting on Wednesday. The RBNZ is widely expected to raise rates 0.50%.

The US economic calendar is empty.

Chart of the Day: CBOE Volatility Index

Source: Yahoo Finance

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

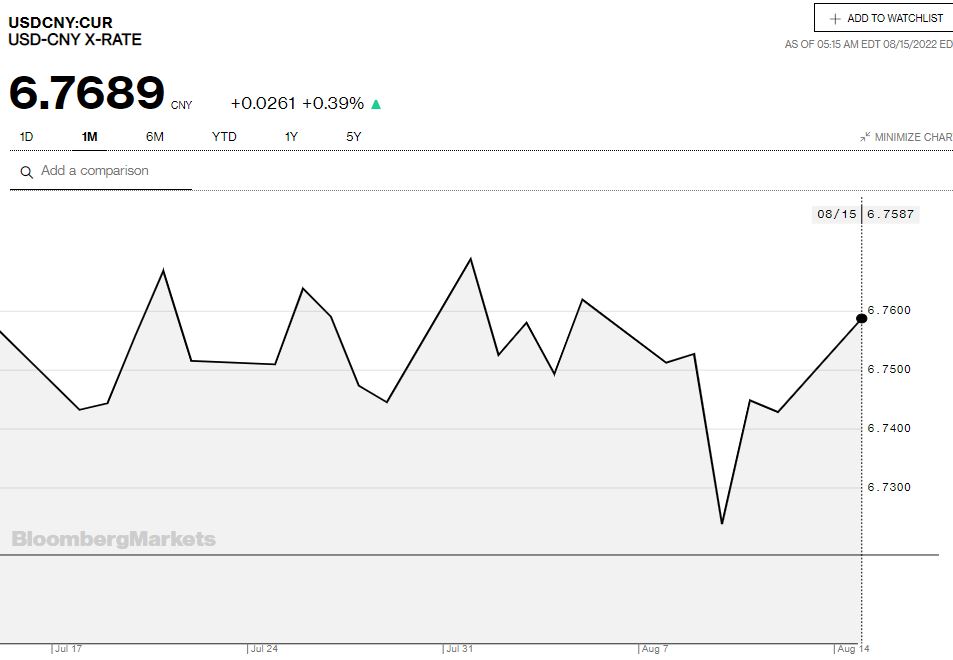

China Snapshot

Today’s Bank of China Fix: 6.7410, previous 6.7413

Shanghai Shenzhen CSI 300 fell 0.13% to 4,185.69

PboC cut 1 year Medium Term Lending Facility by 10 bps to 2.75% and 7 day reverse repo rate cut to 2.0%.

From National Bureau of Statistics China

Industrial Production (actual 3.8% vs forecast 4.6%, previous 3.9%)

Retail Sales July (actual 2.7% vs forecast 5.0%, previous 3.9% y/y)

Chart: USDCNY 1 month

Source: Bloomberg