Source: YouTube/Peakes

- US 10-year Treasury yield touches 1.806%, opens at 1.774%

- US/NATO and Russia talks ongoing

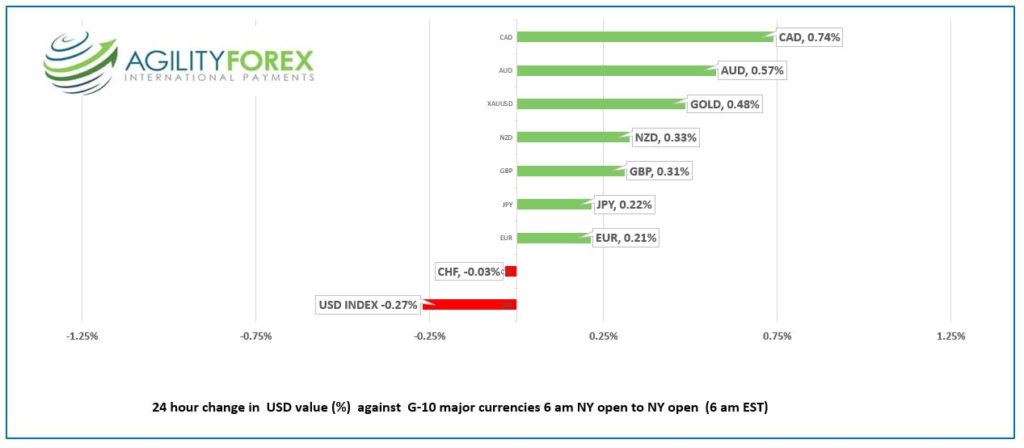

- CAD dollar leads G-10 currencies higher

FX at a Glance

Source: IFXA Ltd/RP

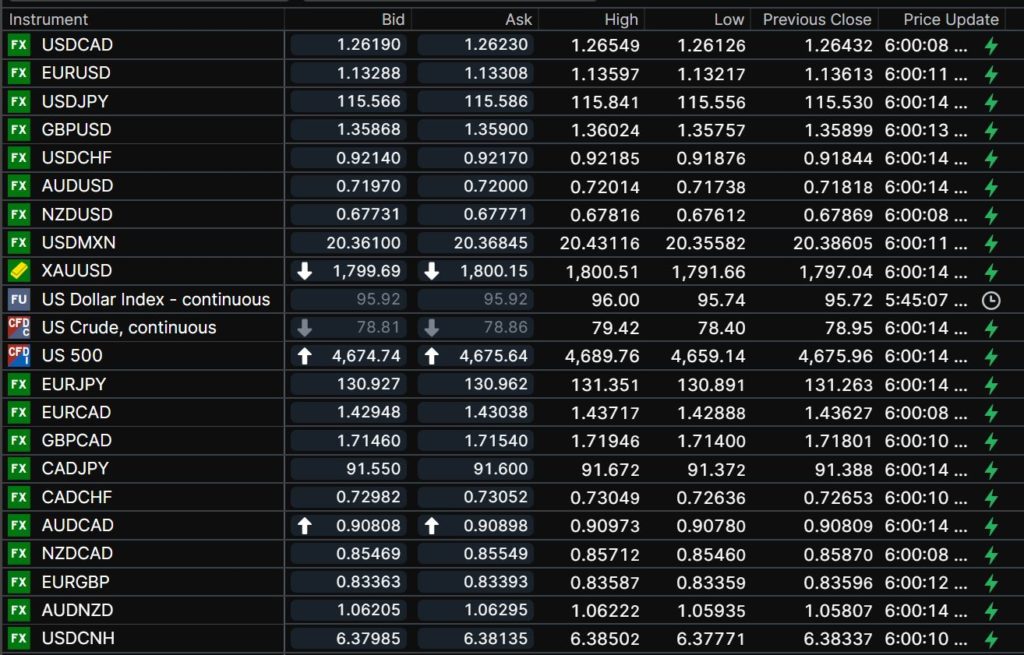

USDCAD Snapshot: Open 1.2619-23, Overnight Range-1.2613-1.2666, previous close 1.2643

The USDCAD slide precipitated by the US and Canadian employment reports may have been overdone. The US data was not as bad as the headline suggested while Canada’s January employment data is expected to be very weak due to the latest Omicron restrictions in Quebec and Ontario.

WTI oil prices have retreated back below $80.00/b due to a mix of profit-taking, and global growth concerns.

Technical view: The intraday USDCAD technicals are bullish following the test and rebound off of the 1.2600-1.2610 support area and the subsequent breach of the minor January downtrend line when prices moved above 1.2650. Nevertheless, the downtrend line from December 20 remains intact below 1.2770 and unless it is decisively broken, further tests of support are likely.

For today, USDCAD support is at 1.2610 and 1.25900. Resistance is at 1.2680 and 1.2710. Today’s Range 1.2620-1.2680

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Analysts are predicting US CPI will be 7.0%/y/y Wednesday and how the Fed will manage prices going forward will be a key theme for Powell on Tuesday.

There is a minor undercurrent of negative risk sentiment in case the ongoing US/NATO and Russia talks about Putin’s intentions toward the Ukraine sour.

GBPUSD rallied to 1.3602 then dropped to 1.3551 due to renewed US dollar strength and fears that the UK will trigger Article 16. EURGBP selling pressures provide a modicum of support for GBPUSD.

USDJPY traded quietly in Asia, due to a Japanese holiday. Traders are ignoring the bounce in US Treasury yields in part due to mild safe-have demand, and profit-taking.

AUDUSD and NZDUSD retreated from session highs due to broad US dollar strength. Australia Building Approvals rose 3.6% m/m in November (forecast 0.0%) and Retail Sales are due tomorrow.

The US and Canadian economic calendars are empty.

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

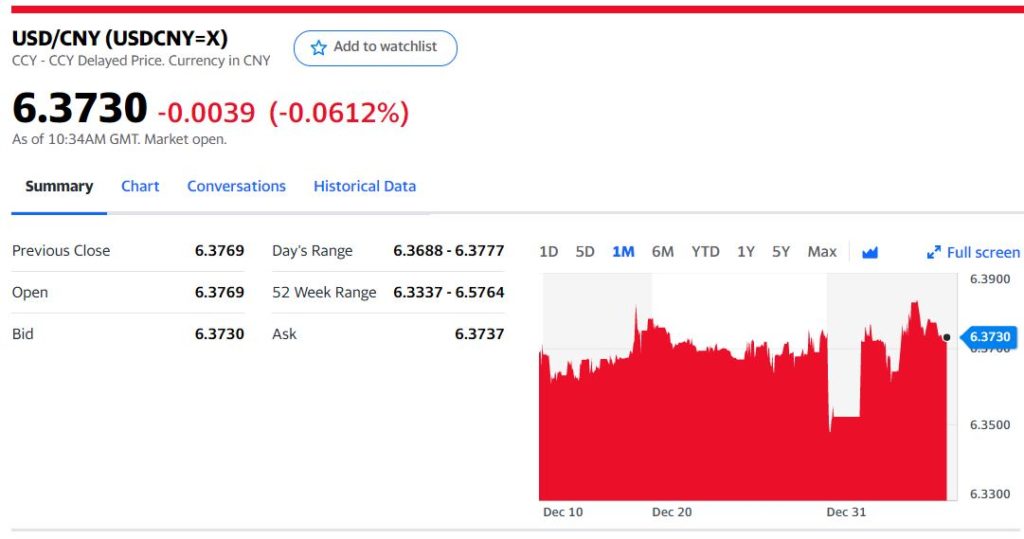

China Snapshot

Today’s Bank of China Fix 6.3653, previous 6.3742

Shanghai Shenzhen CSI 300 rose 0.45% to 4,844.05

Analysts suggest PBoC may ease in first few months despite risk of US tightening

Chart: USDCNY 1 month

Source: Yahoo Finance