Source: Chronicle.com

- Hawkish ECB-speak underpins EURUSD

- BoE monetary policy meeting delayed until September 22

- US dollar remains on defensive, opens mixed compared to Friday

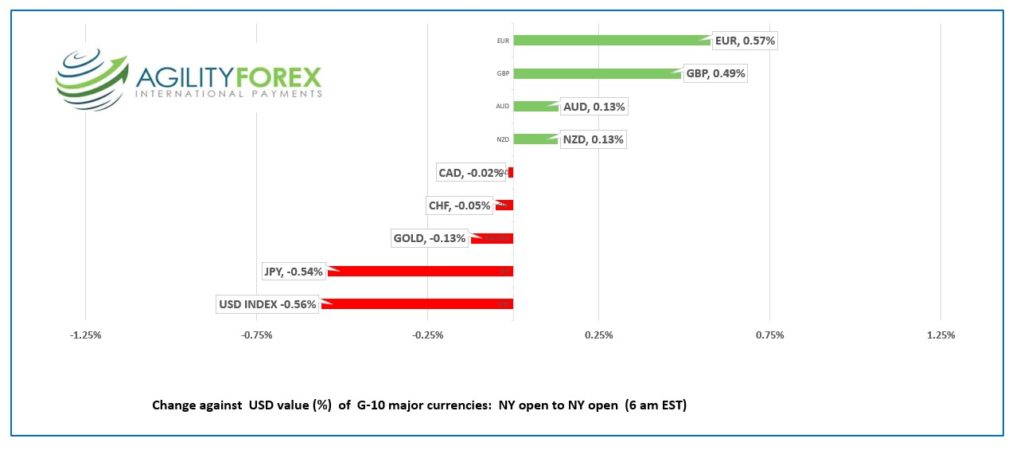

FX at a glance:

Source: IFXA Ltd/RP

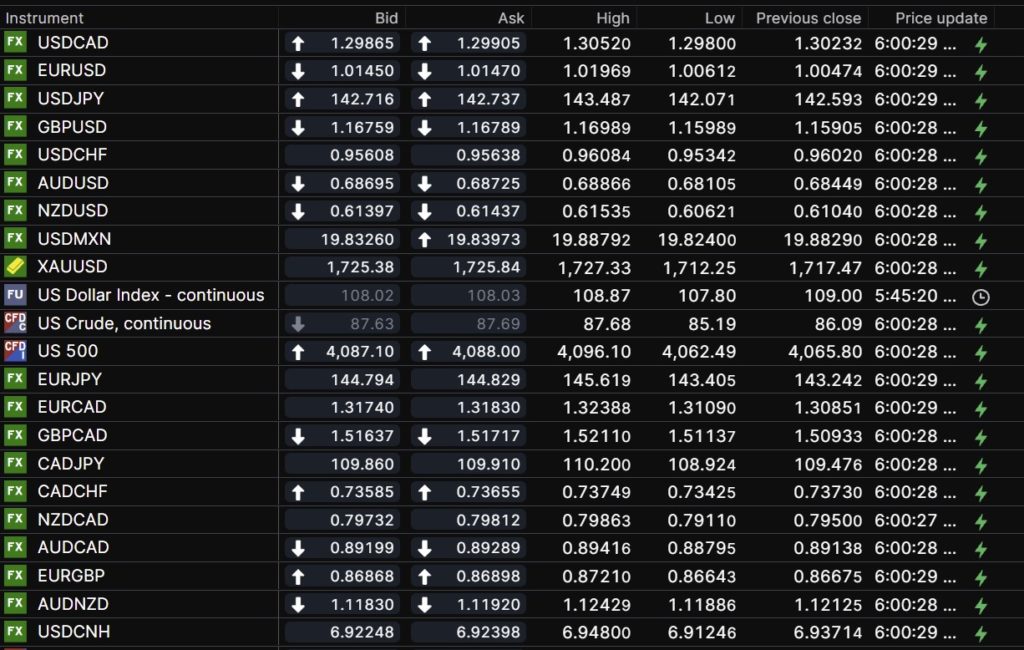

USDCAD Snapshot: open 1.2987-91, overnight range 1.2980-1.3052, close 1.3023

USDCAD dropped Friday despite a disappointing employment report. Canada lost 39,700 jobs instead of gaining 15,000 as expected, while the unemployment rate spike to 5.4% from 4.9%. The report was ugly and suggests that BoC rate hikes are having an impact on the economy.

But no one cared. All eyes were on the US and the rising S&P 500 index. Stocks rallied on speculation that the worst for US rates was priced in, and that sentiment extended S&P 500 futures gains overnight.

WTI oil prices started to rebound on Thursday and continued to do so overnight, rising from $85.19/b to $87.70/b in early NY. The gains were underpinned by fears the Iran nuclear deal talks have stalled.

There are no Canadian economic reports today leaving USDCAD direction to be determined by S&P 500 price action.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish below 1.3050, looking for a break of uptrend line, and Fibonacci support in the 1.2960 area. A successful breech puts 1.2840 in play. A break above 1.3060, negates the downward pressure and more 1.3000-1.3200 consolidation.

For today, USDCAD support is at 1.2960 and 1.2910. Resistance is at 1.3050 and 1.3090. Today’s range: 1.2960-1.3040

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Has the worm turned for US dollar bulls? Some think so. The US dollar started sliding last Wednesday, extended losses into Friday’s close, and continued the trend overnight. The US dollar index dropped from Wednesday’s peak of 110.75 to 107.80 in early NY today.

The dollar sell-off is fueled by ECB policymakers suggesting that last week’s 75 bp rate hike will be followed by a similar bump on October 27. Analysts suggest that the rise in ECB rates will be occurring at the same time the Fed slows the pace of US hikes as rates approach 4.0%, the expected peak level for this cycle. The narrowing of US/ECB interest rate spreads reduces the demand for US dollars.

Traders are also trimming positions because they believe senior Japanese politicians and BoJ officials are serious about intervening to boost the Japanese yen.

Dollar sellers also emerged following weekend reports that a Ukraine military offensive led to a panicked Russian retreat, driving the invaders from some key cities.

It is far too soon to conclude the US has won the inflation battle, and the evidence will be on display tomorrow when August CPI is released.

China continues to lock down the equivalent of most of the population of the US. President Xi Jinping’s “zero-covid” policy was a key reason for supply chain disruptions during the pandemic, and there is no reason to believe things have changed.

Aggressive intervention chatter by Japanese officials spurred Friday’s US dollar sell-off, but as George Soros and Stanley Druckenmiller proved to the Bank of England in September 1992, market forces will triumph over flawed monetary policy every time. As long as the BoJ insists on maintaining the 0.25% yield curve control cap for 10-year Japanese Government Bonds, the prospect of higher US rates will sink JPY.

The Ukraine military may have won a couple of battles, but the war is far from over. That means all the war-related issues weighing on the Eurozone economy are still valid.

The Iran nuclear talks have stalled, and Iran is increasing its stockpile of enriched uranium.

Israel, Saudi’s and the US will do whatever it takes to thwart Iran’s nuclear ambitions.

The Chairman of the National Peoples Congress of China said China is willing to enhance its cooperation with Russia and thanked Putin for condemning Pelosi’s visit to Taiwan. In return, Russia said they supported the “one- China” policy.

Arguably, the worm movements are merely due to it getting more comfortable.

EURUSD closed Friday at 1.0047, gapped higher at the Asina open to 1.0047, then climbed to 1.0197 before retreating to 1.0135 in NY. Prices were boosted by an improved risk tone and hawkish comments from ECB policymaker Luis de Guindos who said, “We decided to raise rates by 75 basis points and have announced that we’ll continue to raise. How many times we do so and by how much will depend fundamentally on data.” EURUSD resistance is in the 1.0190-1.0205 zone.

GBPUSD soared from 1.1591 to 1.1699 and snapped the downtrend line from August 10 in the process. The currency got a bit of a lift after July GDP grew 0.2%, less than expected but far better than the 0.6% drop in June. The UK will be closed on September 19 for Queen Elizabeth’s funeral, and the Bank of England monetary policy meeting has been delayed until September 22.

USDJPY retreated in the face of broad US dollar weakness, but losses were slowed by the US 10-year Treasury yield flitting around 3.30%.

AUDUSD rallied in a 0.6811-0.6887 range while NZDUSD bounced in a 0.6062-0.6153 band. Both currency pairs dropped at the Asian open, then recouped all the losses on the improved risk sentiment tone.

There are no top-tier US economic reports today.

Chart of the Day US dollar Index

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

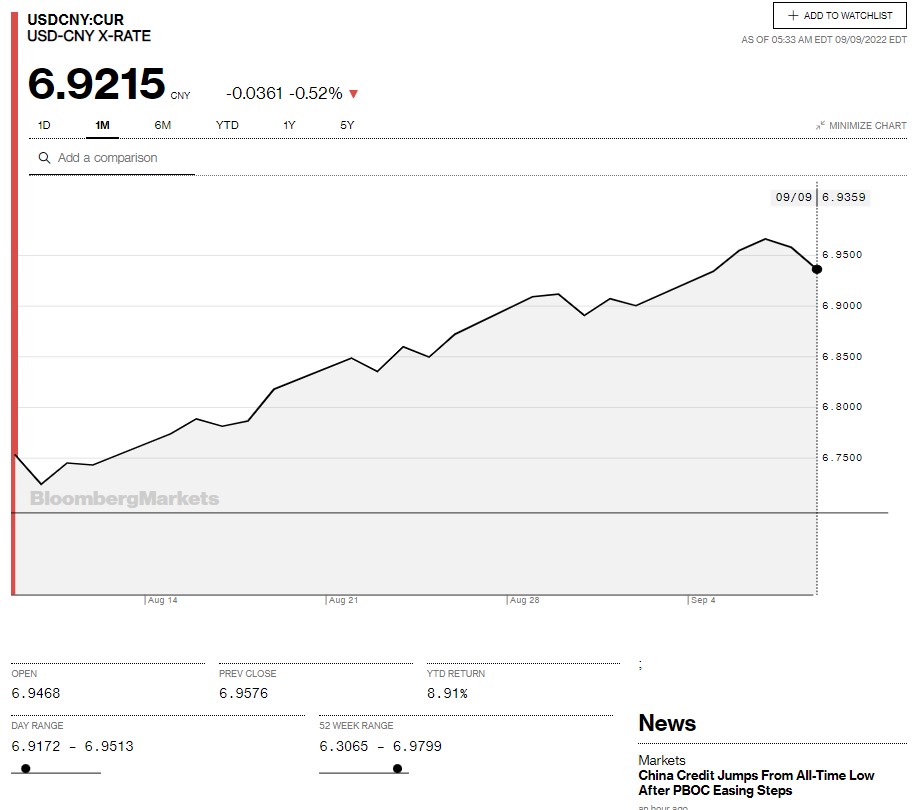

China Snapshot

Today’s Bank of China Fix: Closed, previous 6.9098

Shanghai Shenzhen CSI 300 CLOSED, Previous 4,093.79

China Close for Mid-Autumn holiday

Chart: USDCNY 1 month

Source: Bloomberg