Source: USmoney reserve

- RBA hikes 25 bps as expected

- Risk sentiment improves on hopes Fed slows pace of rate hikes

- US dollar opens lower compared yesterday, EUR unchanged

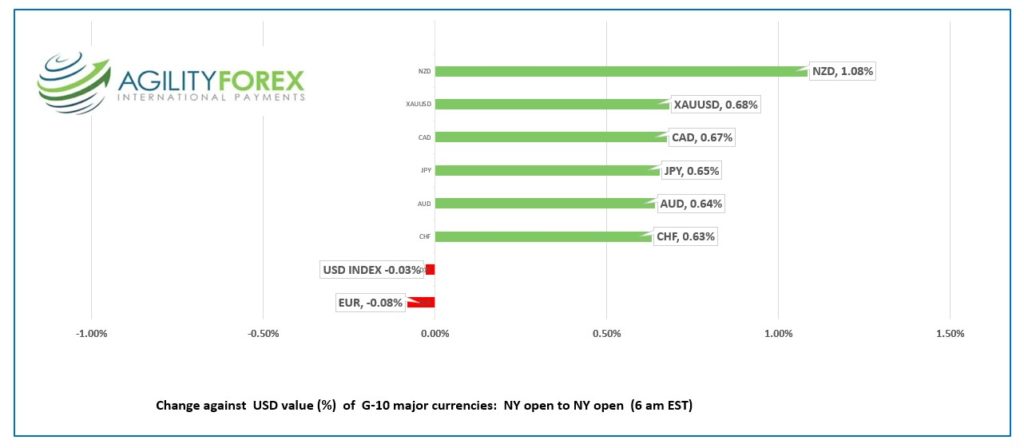

FX at a glance:

Source: IFXA Ltd/RP

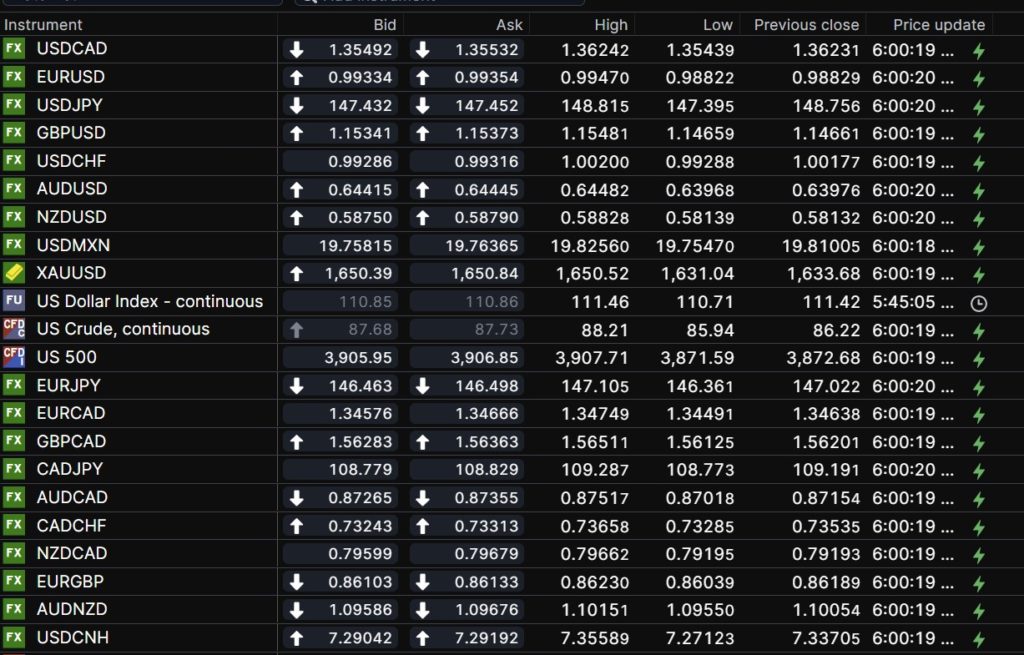

USDCAD Snapshot: open 1.3549-53, overnight range 1.3544-1.3624, close 1.3623

USDCAD dropped thanks to broad US dollar weakness ahead of Wednesday’s FOMC meeting and perhaps from modestly higher oil prices.

Opec’s 2 million b/day production cuts begin today although production difficulties mean the actual cut is just 1.2 million/bd. Opec raised its medium- and long-term forecasts for world demand which are pretty meaningless for traders today.

President Joe Biden is jumping on the “tax windfall oil profits” bandwagon while simultaneously allowing Russia crude shipments to continue without price cap penalties until mid-January.

It is all noise and markets will churn inside recent ranges until after the Fed meeting tomorrow.

USDCAD Technical outlook

The intraday USDCAD turned bearish after failing to break above the top of the downtrend channel yesterday, then dropping through support at 1.3605 overnight. That sets the stage for a probe of the 1.3490-1.3500 support area.

Fibonacci retracement analysis of the September 12-October 13 range suggests that the break of 1.3580, the 38.2% Fibonacci retracement level sets up further losses to 1.3340, the 61.8% level.

For today, USDCAD support is at 1.3490 and 1.3460. Resistance is at 1.3580 and 1.3610. Today’s range 1.3510-1.3580.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Halloween may have come and gone but traders are eagerly awaiting the tricks or treats from Wednesday’s Fed meeting.

Risk sentiment is mostly positive today with the US dollar in retreat, global equities higher, and the US 10-year Treasury Yield at 3.96%, well below the 4.10% level seen yesterday.

It would be foolish to read a lot into the overnight market action as they are merely position adjusting based on hopes and wishes for the Fed to slow the pace of rate hikes. That view is encouraged by Wall Street Journal Reporter Nick Timiraos who is thought to be the Fed’s unofficial “press agent.”

Goldman Sachs economists think Nick is full of hot air and yesterday said fed funds would peak at 5.0% by March 2023.

Asia equity indexes closed higher with Hong Kong’s Hang Seng index surging 5.23%, partly due to the easing of Covid restrictions in some areas. Australia’s ASX 200 jumped 1.65% in relief the RBA only raised rates 25 bps.

European bourses opened higher and continued to climb with the French CAC index gaining 1.62% and the UK FTSE 100 rising 1.45%.

The improvement in global risks sentiment lifted S&P 500 futures 0.87%, and DJIA futures 0.61% while WTI oil and gold rose 1.68% and 0.80% respectively.

EURUSD traded firmly in a 0.9882-0.9447 range with many centers closed for All Saints Day. Yesterday’s sharply higher than expected eurozone inflation data suggests the ECB will hike rates another 75 bps on December 15.

GBPUSD is attempting to recover yesterday’s losses and rallied from 1.1466 to 1.1551 and is at 1.1542 in NY. Prices are supported by broad US dollar weakness, but gains are capped ahead of Thursday’s Bank of England meeting. Markets are expecting a 75 bp rate hike but that call is far from unanimous. Failure to match an expected 75 bp Fed hike could knock GBPUSD back to 1.1250.

USDJPY traded defensively in a 147.00-148.82 range with prices weighed down by the drop in the 10-year Treasury yield. The Bank of Japan reportedly spent $43 billion to knock USDJPY below 150.00.

AUDUSD traded choppily with a bullish bias in a 0.6397-0.6448 range and opened near the top in NY. The RBA hiked 25 bps to 2.85% as expected, although hotter than expected inflation data last week had some analysts expecting a 50 bp hike. Traders anticipate another 25 bp hike at the December meeting.

US October ISM Manufacturing PMI (forecast 53 vs 51 in September) and the Job Openings and Labor Turnover (JOLTS) survey due.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

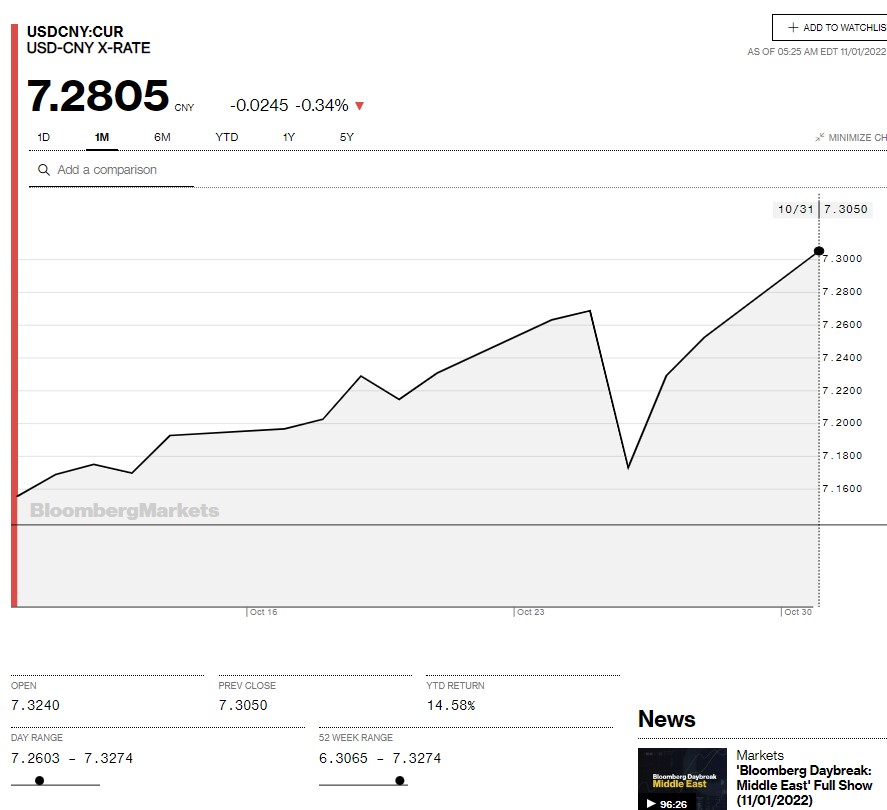

China Snapshot

Today’s Bank of China Fix: 7.2081, previous 7.1768

Shanghai Shenzhen CSI 300 rose 1.65% to 3634.17

Caixin October Manufacturing PMI 49.2 (forecast 49, September 48.1)

Chart: USDCNY 1 month

Source: Saxo Bank