Photo: Wannapik.com

May 5, 2023

- US regional bank woes, dovish Fed, hawkish ECB, sink greenback.

- Nonfarm payrolls surpass estimates, rise 253,000 (forecast 179,000)

- US dollar poised to end week with losses, Commodity bloc outperforms overnight.

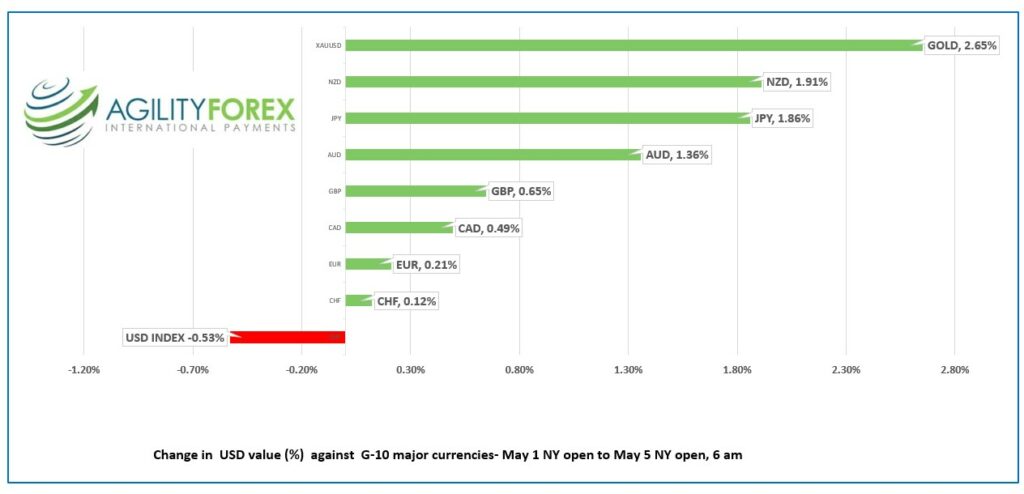

Weekly FX at a glance

Source: IFXA Ltd/RP

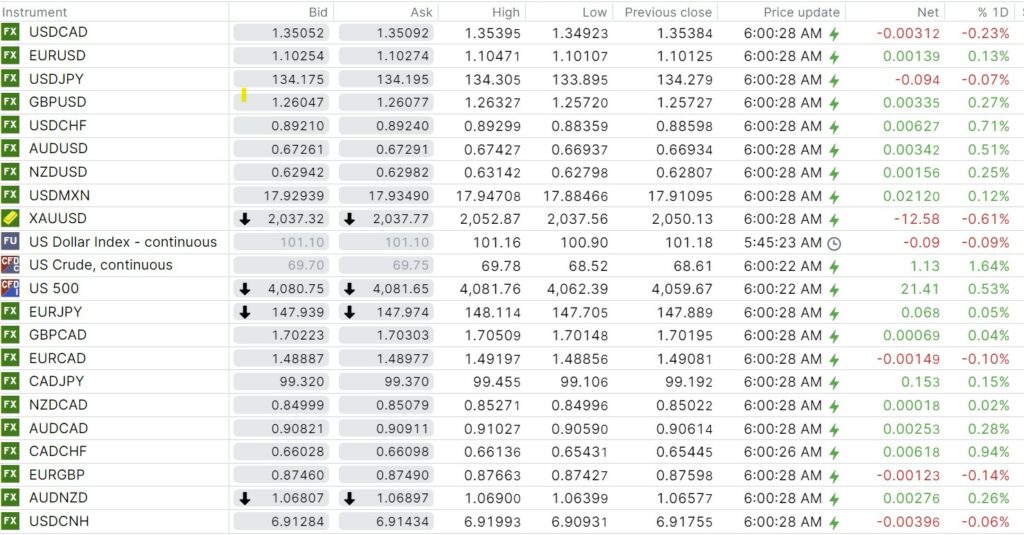

USDCAD Snapshot: open 1.3505-09, overnight range 1.3480-1.3540, close 1.3538

USDCAD sank due to broad US dollar weakness after monetary policy divergence between the ECB and the Fed sparked a sharp US dollar retreat. The move was exacerbated by escalating fears that the US banking crisis was not over, despite what JPMorgan Chase President Jamie Dimon saying it was.

Bank of Canada Governor Tiff Macklem may have contributed to the sell-off. The BoC left rates unchanged at two consecutive meetings, which led to speculation that they may cut interest rates in the latter part of 2023.

Mr Macklem poured cold water on that notion in a speech yesterday. He said it may take inflation longer than the BoC expects to reach the 2.0% target, especially services price inflation. He implied that businesses were partially to blame because they need to slow the pace and size of their price increases. He also said that inflation expectations need to come down and that the labour market needs to rebalance and wage growth moderate.

Perhaps he should have given the speech to the Canadian government. They just gave public servants outsized pay increases,

The Governors remarks suggest that the next BoC rate move could be a hike rather a cut, which may have encouraged additional USDCAD selling.

Canada added 41,400 jobs in April, easily topping the 20,000 forecast and the unemployment rate ticked down to 5.0% from 5.1%. USDCAD inched lower on the results, but the downside was limited because the US nonfarm payrolls report was better than expected, as well.

USDCAD Technical Outlook

The USDCAD flipped to bearish yesterday. USDCAD failed to break above resistance in the 1.3640-60 area, and the subsequent drop below 1.3580, snapped the uptrend from April 14. The sell-off accelerated on the breech of support in the 1.3515-30 area, setting the stage for further losses to the 1.3390-1.3400 zone.

Fibonacci retracement of the April 14-Arpil 28 range suggests a move below 1.3440 will lead to the 76.4% retracement level of 1.3390.

For today, USDCAD support is at 1.3440 and 1.3390. Resistance is at 1.3530 and 1.3560

Today’s range 1.3440-1.3540

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The mighty US dollar, the reserve currency of choice for central banks, is having its comeuppance. Nobody wants it-at least for the time being.

The greenback is suffering due to fears of widening US regional bank woes, the belief that the Fed’s next move will be to cut rates, and a hawkish ECB outlook.

The hardest hit regional banks (PacWest, Western Alliance Bancorp, and First Horizon) are rebounding in pre-market trading, although that bounce is likely of the dead cat variety. Nothing changed overnight to warrant a rally.

The US nonfarm payrolls surprised to the upside by adding 253,000 jobs (forecast 179,00), the unemployment rate dipped to 3.4% from 33.5% and average hourly wages rose 0.5% m/m compared to 0.3% in March.

The US dollar reaction was muted even though the results do not support a rate cut any time soon, mainly because traders are still concerned about regional bank risks.

Asia equity indexes closed modestly positive. Japan’s Nikkei 225 index gained 0.12% while Australia’s ASX index rose 0.37%. European bourses are higher with the German Dax soaring 2.17%, while the UK FTSE 100 index gained 0.91% and the French CAC-40 rose 0.74%. S&P 500 futures point to a positive Wall Street open, although the nonfarm payrolls report could change that outcome.

EURUSD see-sawed in a 1.1011-1.1047 range overnight, supported by the somewhat hawkish ECB outlook, which is in contrast to what the market believes, is a dovish Fed. The ECB raised rates by 25 bps to 3.50% yesterday but the statement, and President Christine Lagarde’s remarks were wishy-washy. Bullish Euro enthusiasm was tempered after Retail Sales fell 1.2% in March; a tad lower than expected.

The intraday EURUSD technicals are bullish above 1.1000, but an over-abundance of long EURUSD trades hampers gains.

GBPUSD traded in a 1.2573-1.2633 range overnight. Traders took full advantage of the widespread US dollar malaise and GBPUSD rallied sharply from this week’s low of 1.2434 on May 2, a gain of 1.6% from trough to peak. The Bank of England is expected to hike rates 25 bps next week, with analysts suggesting another two hikes to follow. GBPUSD is vulnerable to a sharp sell-off if the statement focuses on the latest central bank go-to phrase about the” lagging impact of previous rate hikes on the economy.” That would suggest a less aggressive BoE.

USDJPY consolidated yesterday’s losses in a 133.90-134.31 range overnight and has a negative bias due to soft US Treasury yields. The US 10-year Treasury yield is sitting a 3.405% today.

AUDUSD rallied from 0.6694- to 0.6743 overnight, leading commodity bloc currencies higher. The recent hawkish surprise from the RBA and broad US dollar weakness fueled the rally.

FX open, high, low, previous close as of 6:00 am ET

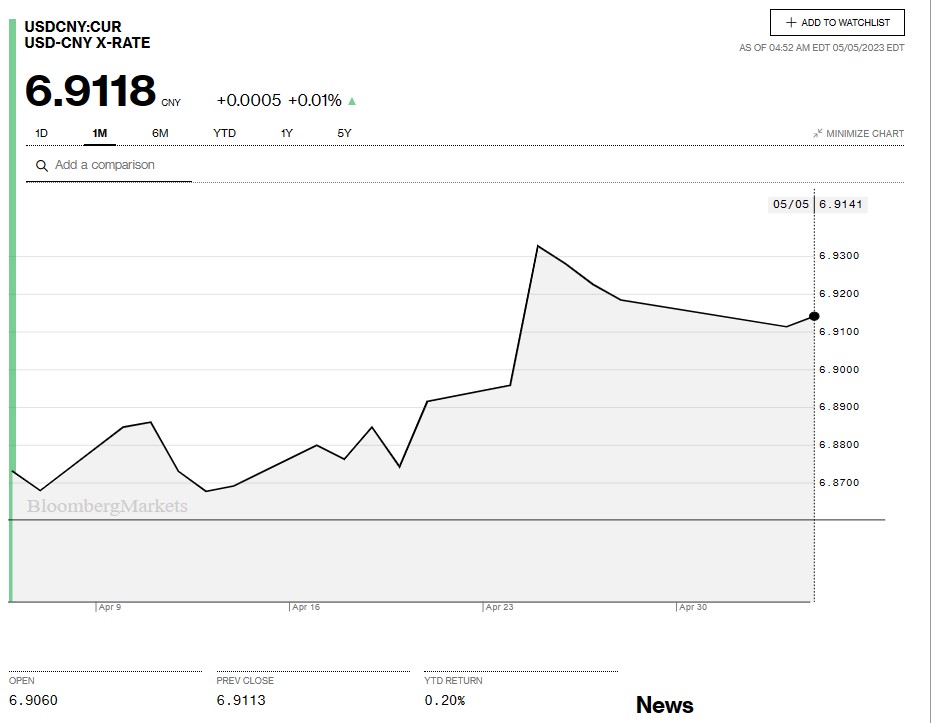

China Snapshot

Bank of China Fix: 6.9114, previous 6.9054.

Shanghai Shenzhen CSI 300 fell 0.33% to 4016.88.

Caixin April Services PMI 56.4 (forecast 56.5, previous 57.8).

Chart: USDCNY 1 month

Source: Bloomberg