Photo: Freepik

March 23, 2023

- European central banks hike rates-SNB 50 bps, Norges Bank 25 bps.

- Traders aren’t buying what the Fed is selling.

- US dollar slides overnight as traders digest FOMC decision.

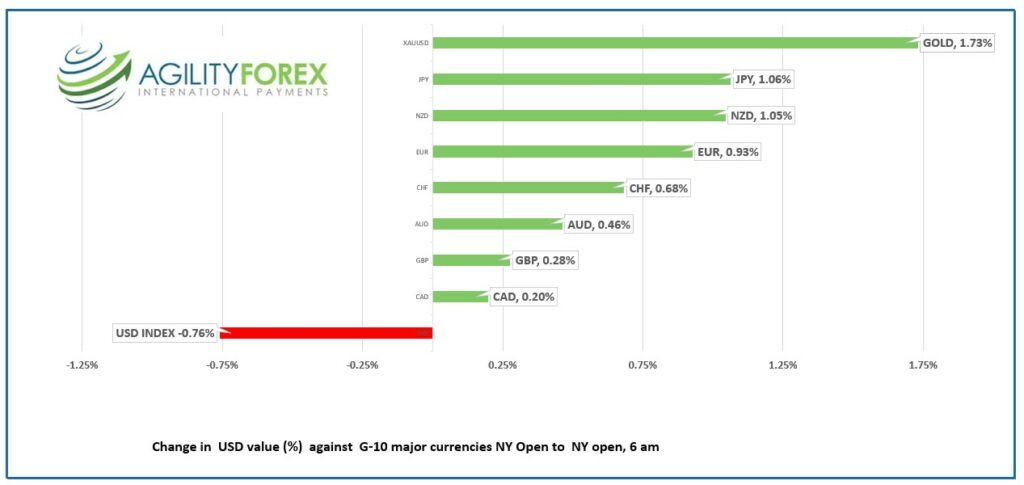

FX at a glance

Source: IFXA Ltd/RP

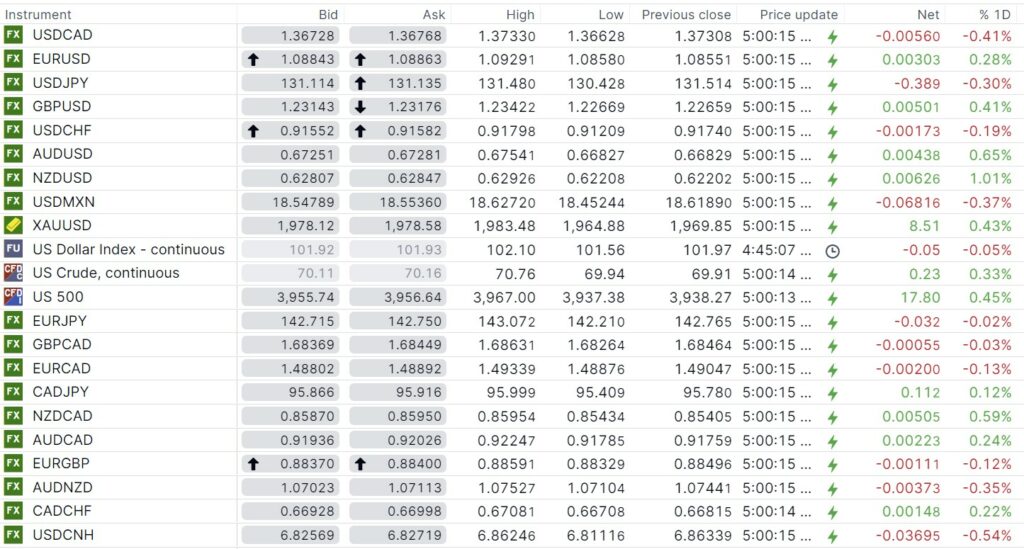

USDCAD Snapshot: open 1.3673-78, overnight range 1.3642-1.3733, close 1.3731

USDCAD is the laggard as the US dollar falls against the G-10 majors.

The FOMC raised US rates 25 bps yesterday bringing the benchmark rate range to 4.75-5.0%. It probably would have been a 50 bp bump if the Fed just focused on economic data, but the recent banking system tremors spooked them.

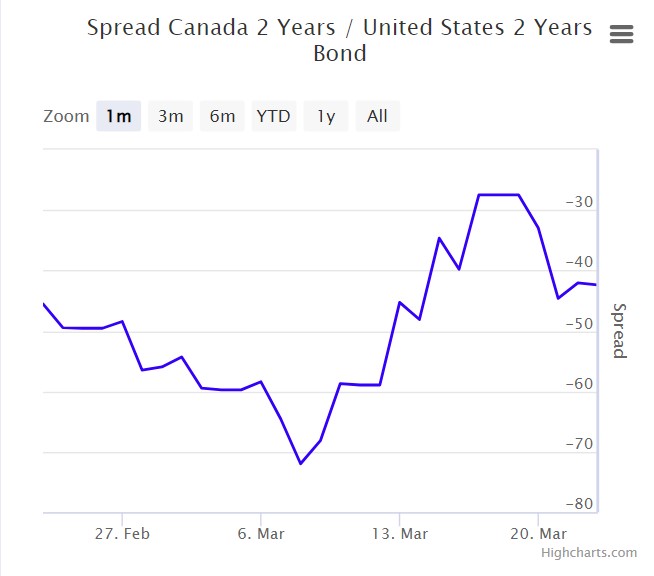

The Fed move also put a spotlight on the recent Bank of Canada decision to leave its benchmark rate and the widening CAD/US interest rate differential since that meeting. The search for yield suggests USDCAD demand as investors move from Canada to US bonds.

Source: Worldgovernmentbonds.com

However, the rebound in WTI oil prices since Monday is helping to cap USDCAD gains. WTI traded at $64.15 at the start of the week and hit $70.76/b overnight. Prices got an added boost today after Goldman Sachs energy analysts flipped flopped. Last week they lowered their Brent forecast and today they raised it. They expect Chinese oil imports to accelerate due to demand and new refining capacity later this year.

The S&P 500 index is trading with a negative bias and that will underpin USDCAD today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish with the downtrend from March 10 intact below 1.3740. However, support in the 1.3640-60 continues to thwart downside moves. A decisive break below 1.3640 would target 1.3580 then 1.3520. A topside break suggests a retest of the 1.3850 area.

Longer term, the uptrend line from June 2022 will provide support at 1.3390 and it guards the June 2021 uptrend line which comes into play at 1.3000.

For today, USDCAD support is at 1.3640 and 1.3610. Resistance is at 1.3720 and 1.3760.

Today’s range 1.3630-1.3720

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Traders and analysts are still digesting the FOMC action, but the US dollar and the 10-year Treasury yield have retreated like the Fed announced an end to rate hikes. They didn’t, but traders believe a pause is on the horizon.

Wall Street gave up initial gains following the Fed decision and the S&P 500 closed down 1.65%. The major Asian equity indexes followed the lead with the Nikkei finishing its session with a loss of 0.17% while Australia’s ASX 200 gave up 0.67%. Chinese equity indexes bucked the trend and the Hang Seng rallied 2.34%.

European bourses are close to unchanged except for the UK FTSE which is down 0.40% ahead of the Banak of England monetary policy announcement. S&P 500 futures are higher but below its best level.

The Swiss National Bank hiked rates 50 bps to 1.5% to fight inflation, suggested further rate hikes were possible, and announced that government actions put an end to the banking crisis.

US weekly jobless claims were 191,000, 1,000 less than the prior week and more evidence of a tight labour market. The Chicago Fed National Activity index showed economic growth declined in February as the index was -0.19 compared to 0.23 in January. The data did not have any impact on trading.

EURUSD traded in a 1.0858-1.0929 range overnight and sit at 1.0880 in NY as of 5:30 am PDT. ECB Governing Council member and Estonia Central Bank President Madis Muller said inflation was a bigger problem than higher borrowing costs. He is a well known hawk, and his comments were not new. EURUSD is in an intraday uptrend above 1.0820 but momentum studies suggest it is overbought and ripe for a correction.

GBPUSD climbed from 1.2267 to 1.2342 overnight and is trading at 1.2330 in the aftermath of the Bank of England raising interest rates by 25 bps to 4.25%. It was not unanimous as two MPC members voted against the hike. The dissenters, Swati Dhingra and Silvana Tenreyro believe the energy price shock will drive CPI lower.

USDJPY rallied from its overnight low of 130.43 to 131.48 in NY after the US 10-year Treasury yield rose from 3.43% in Asia to 3.511% in NY (as of 5: 30 am PDT).

AUDUSD is in the middle of its 0.6683-0.6754 range with price movements tracking global risk sentiment.

NZDUSD climbed to 0.6293 from 0.6221 despite comments by Reserve Bank of New Zealand Chief Economist Paul Conway suggesting a recession was likely.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

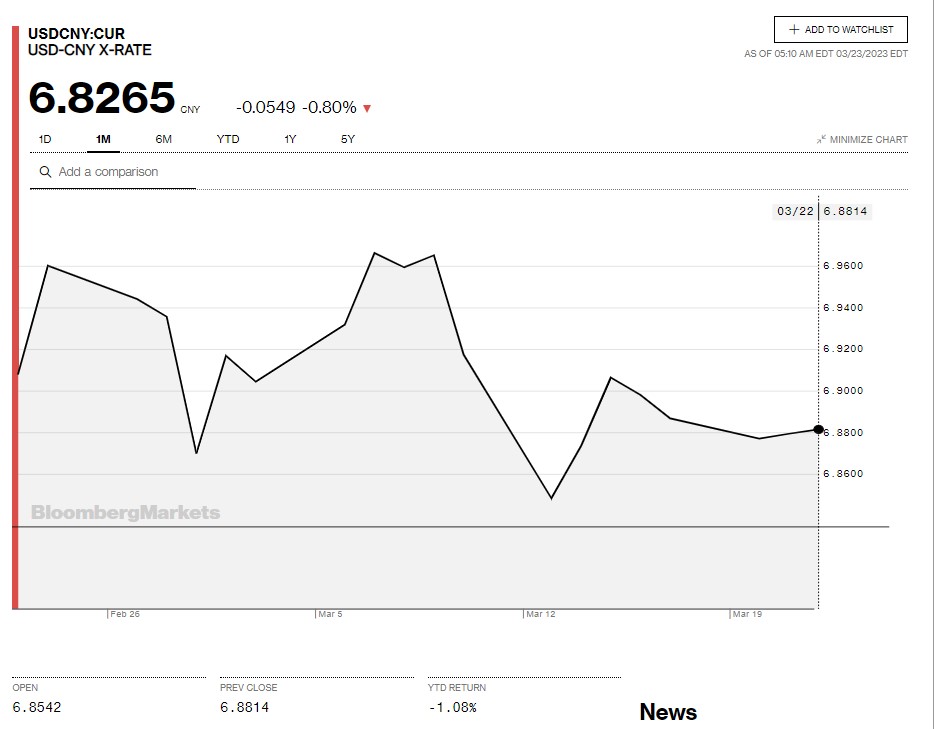

China Snapshot

Bank of China Fix: 6.8709, Previous: 6.8715

Shanghai Shenzhen CSI 300 rose 0.99% to 4039.09.

Chart: USDCNY 1 month

Source: Bloomberg