Photo: Pixabay

August 13, 2020

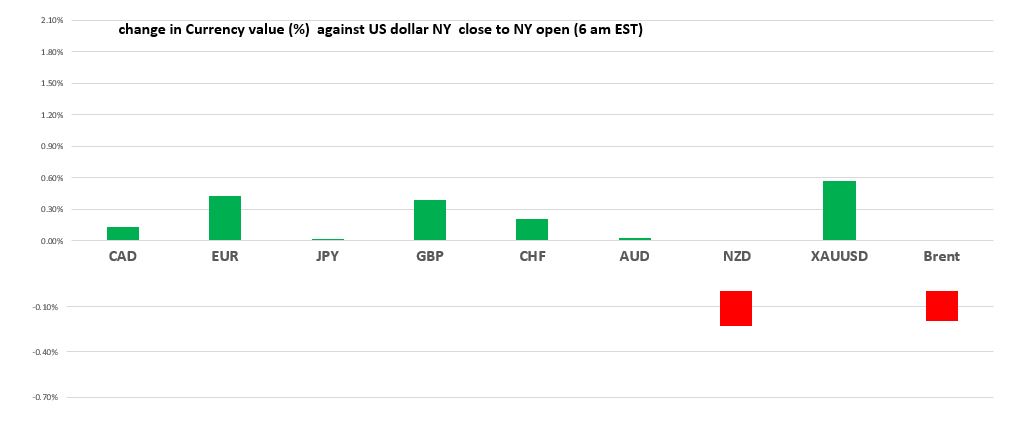

USDCAD Open (6:00 am) 1.3227-31, Overnight Range 1.3224-1.3256

- IEA trims oil demand forecast

- America records 1,500 COVID-19 deaths, Wednesday-highest since May

- Greenback opens down against majors except NZD

Source: Saxo Bank/IFXA Ltd

FX Recap and outlook: Traders continue to shun the US dollar, at least those of them who are actively trading, and not vacationing.

August is vacation month, and Puerto Backyardo is the preferred destination in this Summer of COVID. It also means FX volumes are lighter than usual and FX moves may be exaggerated.

The Trump Administration continues to hammer friends and foes with trade tariffs. Yesterday, the Americans announced the 15% levy on Airbus and 25% tariffs on over 100 European products would stay in place. US Trade Representative Robert Lighthizer said: “The EU and member states have not taken the actions necessary to come into compliance with WTO (World Trade Organization) decisions.”

The news did not dissuade EURSD traders from buying the single currency. EURUSD bottomed out at 1.1710 yesterday and is trading at 1.1840 in NY today. EURUSD continues to be supported by expectations that the Eurozone economy will outperform the US economy. The American bungling of the pandemic is another factor as many states are still struggling to cope with new cases. (55,504 cases were reported yesterday). German July CPI data was as expected and not a factor for FX.

Traders are looking ahead to today’s weekly US Jobless Claims report. They are expected to be 1.120 million, and according to the Wall Street Journal, the 21st week, they have been over 1.0 million.

Nevertheless, if the forecast is accurate, it would be lower than last week and show that American job landscape is improving.

GBPUSD tracked EURUSD gains, as EURGBP stayed in a tight range. GBPUSD gains may be limited as long as there isn’t progress in the EU/UK trade talks, leaving the risk of a “no-deal” Brexit at elevated levels. GBPUSD is trading at the top of its 1.3099 from 1.3032 range in NY.

USDJPY traded in a narrow 106.58-106.88 band. Upside momentum waned with the dip in US Treasury yields.

AUDUSD chopped about in a 0.7157-0.7186 band supported by a general bearish US dollar sentiment and by a stellar employment report. Australia added 114,700 jobs in July, well above the 40,000 forecast and the unemployment rate fell to 7.5% from 7.8%.

NZDUSD was the only major G-10 currency to lose ground against the greenback. Prices continue to be weighed down by yesterday’s ultra-dovish RBNZ outlook and chatter about negative rates. Overnight, RBNZ Deputy Governor Geoff Bascand warned that the resurgence of COVID-19 in NZ was a significant risk to the bank’s outlook.

Oil prices have helped on to this week’s gains. Prices extend yesterday’s gains then stalled when the International Energy Agency downgraded its 2020 demand forecast by 140,000 barrels/day. They blamed weakness in aviation and the high number of COVID-19 cases for the move.

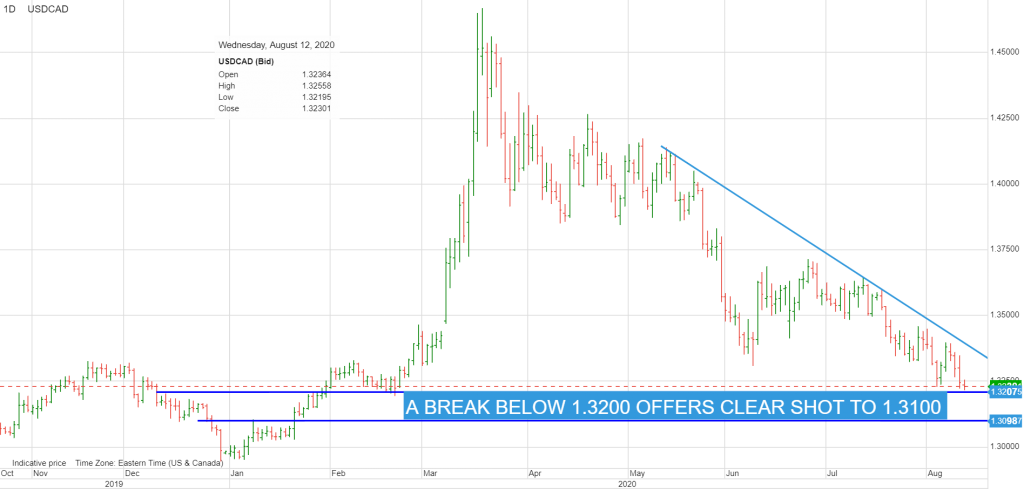

USDCAD is probing support in the 1.3220 area and looking to grind through additional support between 1.3190-1.3210. If so, it could free-fall to 1.3100. The currency pair is tracking broad US moves, garnering a bit of support from firm, steady crude prices. Traders ignored domestic politics. The Bloc-Quebecois (PQ) party is threatening to force an election unless Prime Minister Trudeau and Finance Minister Morneau resign. Most believe it is just wishful thinking. The Progressive Conservative party doesn’t even have a leader as Andrew Scheer resigned and as there isn’t a viable alternative party

USDCAD Technicals: The technicals are bearish below 1.3340 looking for a decisive break below 1.3200. It that happens, there isn’t much support until 1.3100. A break above 1.3340 negates the near-term downside pressure but only a move above 1.3750 would turn the daily technicals bullish. For today, USDCAD support is at 1.3220 and 1.3190. Resistance is at 1.3270 and 1.3320. Today’s Range 1.3190-1.3260

Chart: USDCAD daily

Source: Saxo Bank