March 4, 2020

USDCAD open (6:00 am EST) 1.3359-63 Overnight Range 1.3347-1.3385

The Fed’s surprise 0.50% interest rate cut yesterday morning did not have the desired effect. It was meant to support the US economy (stock markets, especially) in the face of a corona-virus triggered economic growth slow-down. That didn’t happen. Wall Street tanked, with the three major equity indexes losing just under 3.0% by the close. Traders quickly realized that the FOMC was out to lunch. A US rate cut wouldn’t do anything to fix the broken supply chain, or find an antidote to COVID-19.

FX markets ignored the US “Super Tuesday” hype as Democrats try to select a candidate to lose the 2020 election to President Trump. However, some pundits are attributing Biden’s “Super Tuesday” win to the rally in US equity futures, which suggest the DJIA will open 700 points higher.

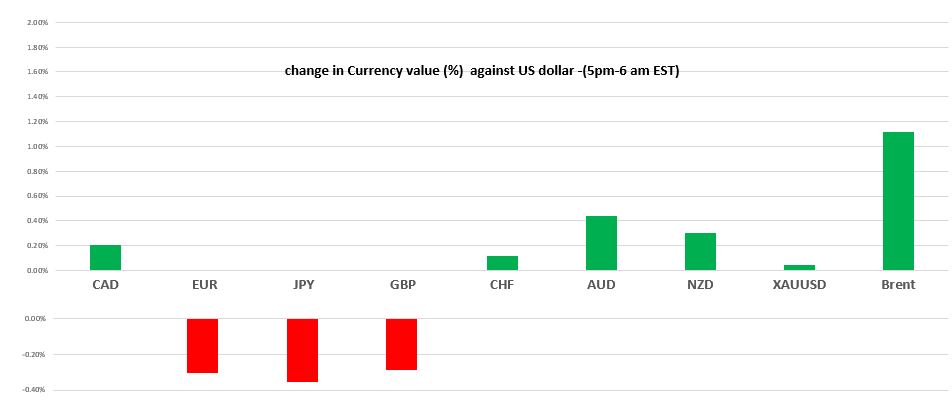

The US dollar closed with loses across the board except against the Canadian dollar. That changed overnight, as weak Eurozone data, rising bond prices, and a rebound in crude prices, undermined EUR, JPY, and GBP, while CHF and the commodity currency bloc inched higher.

Chart: Currency gain/loss (%) against the US dollar from NY close to NY open (6:00 EST)

Source: Saxo Bank/IFXA

FX Recap and outlook: The Bank of Canada (BoC) is in the spotlight today.

Analysts and traders expected the BoC to chop the overnight rate by 0.25% until yesterday’s Fed action. Now, there is a high risk of a 0.50% rate cut, if Mr Poloz wants to maintain the status quo for the US/CAD rate differential.

Arguably, the domestic economy has suffered far more than its neighbour to the south. Railway, blockades, fleeing energy investment, and coronavirus, suggest weaker-than-expected Q1 GDP growth which suggests a 0.50% rate cut is in the cards. If so, USDCAD will retest 1.3450.

EURUSD chopped about in a 1.1140-1.1210 after the surprise Fed action and is trading in New York just above the low. A host of soft Euro-area economic reports including German Retail Sales (January actual 0.9% m/n vs forecast 1.0% m/m), and a series of Services PMI data, offset better than expected, but unchanged, Eurozone January Retail Sales data for Actual 1.7% y/y vs forecast 1.0%). Traders were also disappointed by the ECB’s response to coronavirus. They talked and agreed to talk later. EURUSD is vulnerable to steeper losses on a break below 1.1140.

GBPUSD mostly ignored the Markit Services PMI dip to 53.2 from 53.3. Traders are more worried about the EU/UK trade talks and how COVID-19 will affect the UK economy.

USDJPY is clawing back losses suffered when the Fed cut rates and drove 10-year US Treasury yields to a low of 0.933% yesterday. Yields are at 0.978% in New York, today. BoJ Governor Kuroda said the coronavirus derailed his expectations that the domestic economy would recover in the January-March timeframe. They are considering lowering their economic assessment in March.

AUDUSD got a lift better-than-expected Q4 GDP which rose 0.5% q/q, while the previous results were upgraded to 0.6% from 0.4% q/q. NZDUSD underperformed, in part because domestic data was a tad soft.

Oil prices jumped on rumours that Saudi Arabia and Opec were talking about a deep 1.2 million barrels/day production cut. The rally was stifled by the weak China Services PMI data and fears of a prolonged slump in crude demand.

Today’s US data, (ISM Non-Manufacturing PMI, ADP employment report) will not have an impact on FX markets, thanks to yesterday’s Fed action.

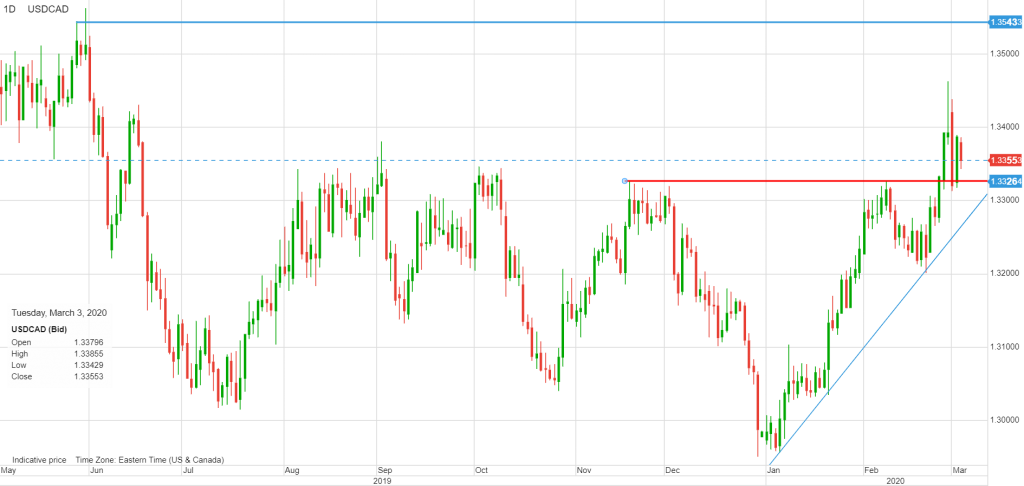

USDCAD Technical Outlook

The USDCAD technicals are bullish above 1.3280, looking for a break above 1.3440 to extend gains to 1.3550. A break below 1.3280, targets 1.3150. For today, USDCAD support is at 1.3320 and 1.3280. Resistance is at 1.3390 and 1.3420. Today’s range 1.3320-1.3420

Chart: USDCAD daily