Photo:Bing Image Creator

August 14, 2023

- Global risk sentiment sours on China concerns.

- Busy week ahead-slow news day today.

- USD dollar steady in mildly risk averse environment.

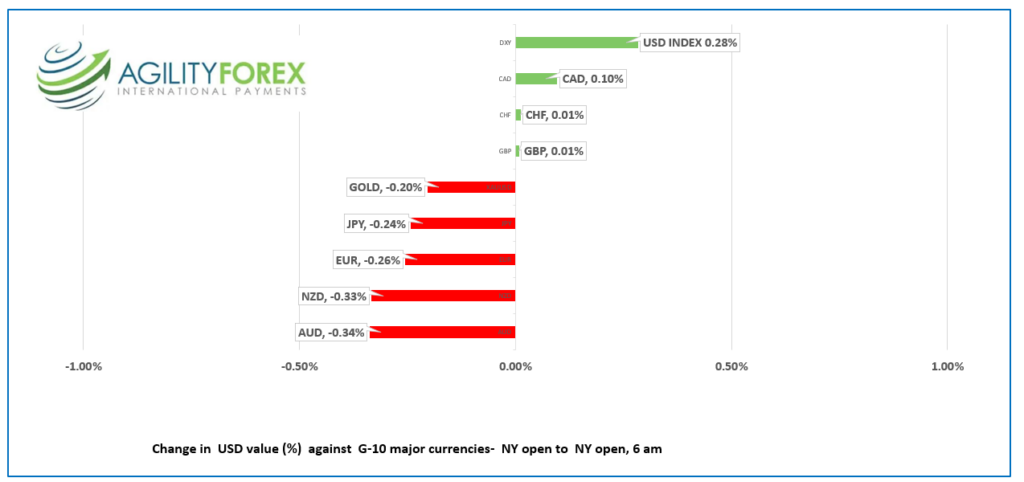

FX at a Glance

Source: IFXA/R

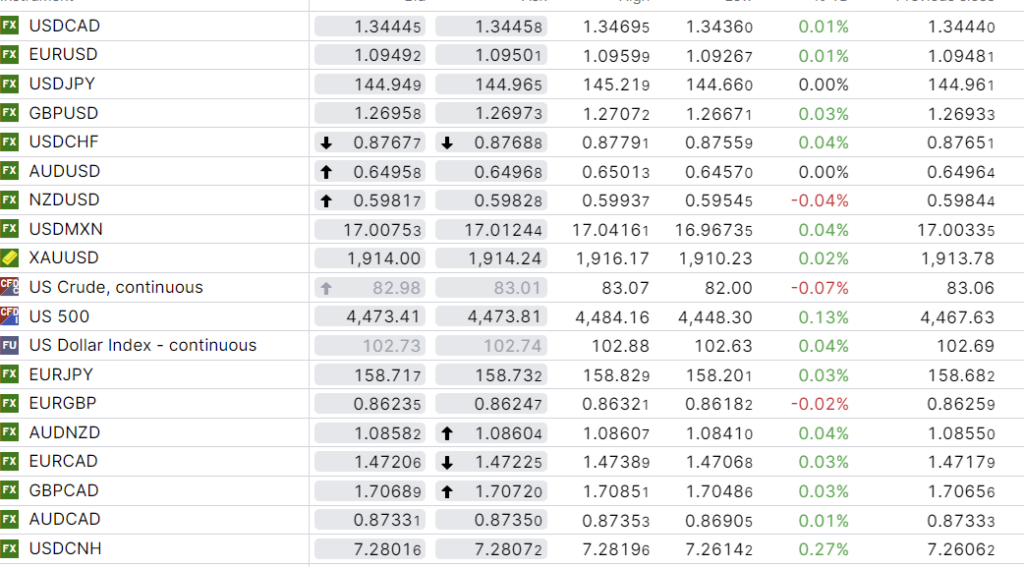

USDCAD Snapshot: open: 1.3443-47, overnight range: 1.3436-1.3470, close 1.3444

USDCAD was directionless overnight, content to mark-time inside Friday’s range while maintaining a mild bid tone.

Traders are hoping that Tuesday’s inflation report will provide some fresh direction. Headline CPI is expected to tick higher to 3.0% y/y from 2.8%, but it is the BoC ‘s Trim and Median measures (currently 3.7% and 3.9% respectively) that will determine whether the Bank hikes or leaves rates unchanged in September.

Oil prices drifted lower due to concerns about reduced Chinese demand. WTI dropped from $83/07 to $82.00 before improved risk sentiment in Europe lifted prices to $82.85 in NY.

The Canadian economic calendar is empty.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3410, looking for a break above 1.3500 to extend gains to 1.3560 then 1.3600. A drop below 1.3410 targets 1.3580, which if broken opens the door to further losses to 1.3280.

For today, USDCAD support is at 1.3410 and 1.3380. Resistance is at 1.3480 and 1.3510. Today’s range 1.3410-1.3490.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap

Last week concluded with Wall Street closing on a mixed note, partly due to the rising US 10-year Treasury yield, which climbed to 4.17% from 4.10%. Risk sentiment worsened further in Asia due to more negative news from China. This time, it was one of China’s largest wealth managers that spooked traders after missing payments on some high yield investment products.

The outlook improved in Europe as European equities rose, led by a 0.52% increase in the German DAX. The UK FTSE 100 was the outlier as it dropped by 0.26%.

Goldman Sachs has aligned with fellow bank economists in predicting that the Federal Reserve will maintain its current interest rates until the second quarter of 2024. At that point, they anticipate the commencement of an easing cycle, marked by an initial 25 basis points rate reduction.

EURUSD nursed Friday’s wounds and drifted in a 1.0927 and 1.0960 range. German Wholesale Price Index data met expectations and had no significant impact. Traders are expecting a 25 basis points rate hike from the Norges Bank on Thursday.

GBPUSD traded in a 1.2667 to 1.2714 band. Traders are in park until the release of the employment report tomorrow, followed by CPI, PPI, and the Retail Price Index on Wednesday.

USDJPY rallied to 145.22 from 144.66 due to rising US Treasury yields. Ministry of Finance and BoJ officials failed to publicly acknowledge their dissatisfaction with the move above 145.00, which, to some, suggests they may be waiting until prices get closer to 150.00.

AUDUSD chopped about in a range between 0.6457 and 0.6503. Prices were weighed down in Asia due to the Chinese news but saw some support after Europe wasn’t as risk averse.

NZDUSD traded in a range of 0.5954 to 0.5994 ahead of the RBNZ meeting on Wednesday. The bank is expected to leave rates unchanged at 5.5% due to the improving inflation outlook.

There are no significant US economic reports today.

FX high, low, close

Source: Saxo Bank

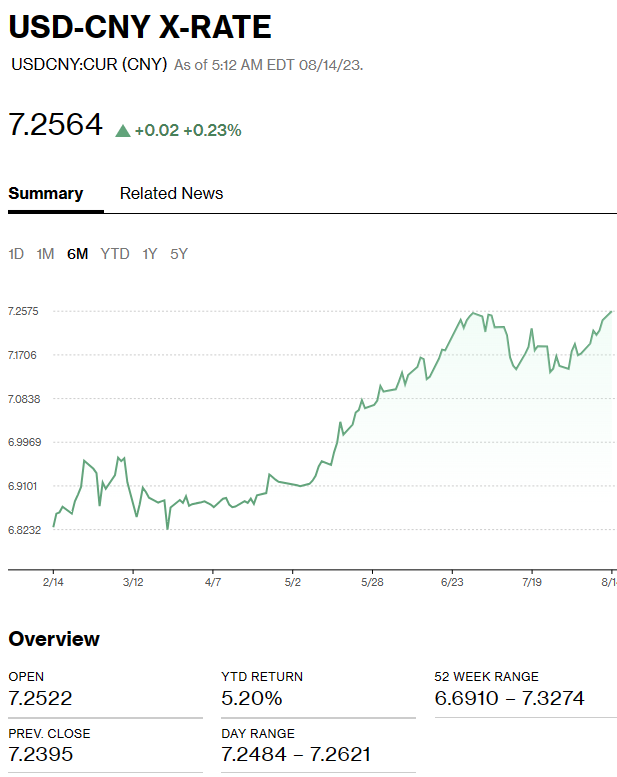

China Snapshot

Bank of China Fix: Today 7.1686 , expected 7.2461, previous 7.1587.

Shanghai Shenzhen CSI 300 fell 0.73% to 3855.91.

PboC leans against weakening yuan and sets the “fix” 775 points below expectations. The yuan is under pressure due to ongoing property developer issues and news that one of China’s largest wealth managers Zhongzhi Enterprise Group missed payments.

Chart: USDCNY 6 month

Source: Bloomberg