Photo: Wikimedia commons

- Markets very dull awaiting FOMC

- US Durable Goods rise 1.9%m/m in June

- US dollar modestly lower EUR underperforms

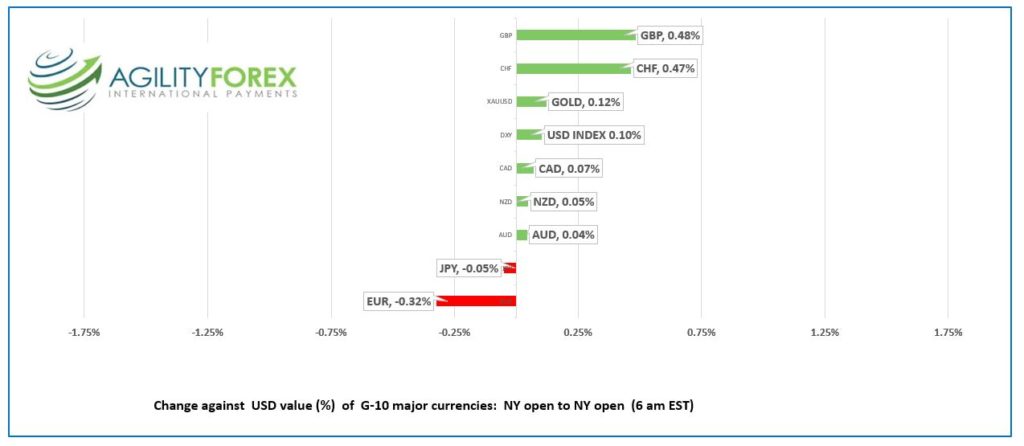

FX at a glance:

Source: IFXA Ltd/RP

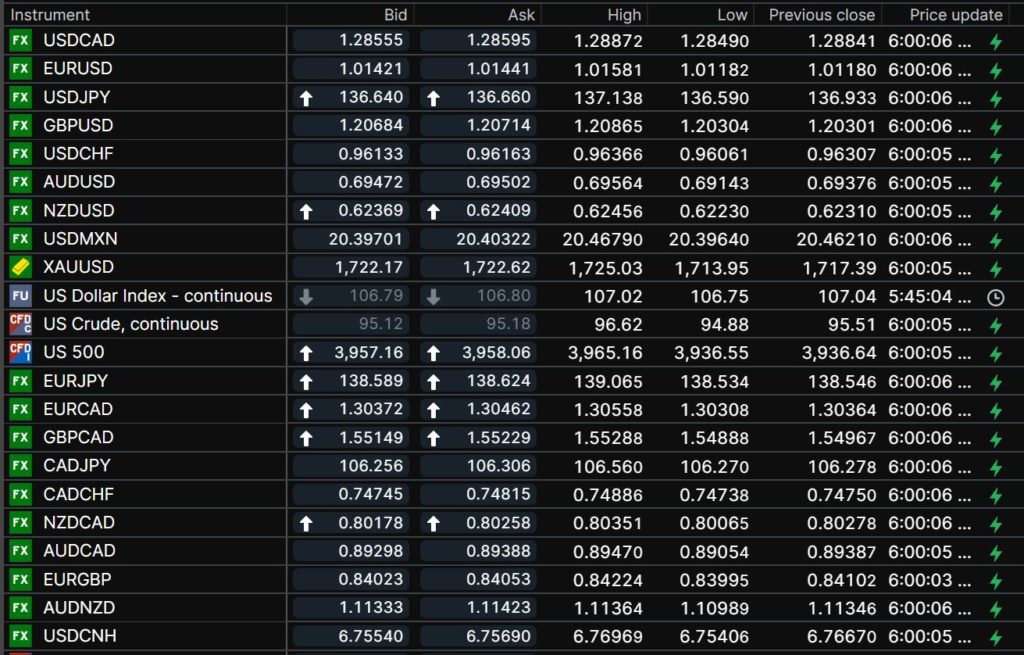

USDCAD Snapshot: open 1.2856-60, overnight range 1.2849-1.2887, close 1.2884

USDCAD continues to trade erratically in 1.2810-1.2950 range, which has contained price action for the past week.

The Canadian economy is similar to that of the US. The labour market is tight, inflation is high, and arguably, the BoC is more aggressive than the Fed. In addition, WTI oil and natural gas prices are at elevated levels, which suggests USDCAD should be trading closer to 1.2000 then 1.3000. The reason it isn’t may be found in the bond market where US and Canadian 10-year yields are almost identical.

In addition, for the time being the US dollar is the only currency that counts. The rest of the G-10 majors are at the mercy of US economic growth sentiment and S&P 500 moves.

The domestic calendar is empty,

USDCAD technical outlook

The intraday USDCAD technicals are bearish below 1.2910 looking for a decisive break below 1.2810 to target 1.2750. A move above 1.2910 suggests a retest of 1.3050.

For today, USDCAD support is at 1.2810 and 1.2780. Resistance is at 1.2870 and 1.2910. Today’s Range 1.2820-1.2910

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

It was a rather dull overnight session, which is usually the case on FOMC meeting day.

The FOMC is almost universally expected to hike 75 bps today, bringing the Fed funds rate to 2.25%, just below the mid-point of the Fed’s “neutral rate.” Traders will look for clues as to whether the September rate hike will be 50 or 75 bps.

US Durable Goods orders rose 1.9% m/m in June, well-above the forecast for a 0.4% decline, and beating the upwardly revised 0.8% result in May.

EURUSD dropped steadily yesterday, falling from 102.49 in Asia to 1.0110 by lunchtime in NY, and consolidated those losses in a 1.0118-1.0158 range overnight. The single currency continues to suffer from recession worries, an energy crisis, political uncertainty in Italy, and bearish technicals. Nevertheless, EURUSD has support in the 1.0110 area and the market is short, suggesting scope for a sell the rumour buy the news, post-FOMC rally.

GBPUSD squeezed out gains overnight, rising from 1.2030 to 1.2087 before easing to 1.2060 in NY. Prices were boosted by EURGBP selling after European gas prices surged close to levels seen when Russia invaded Ukraine. A massive train strike does not help the UK’s economic woes. The union turned down a 4% increase for the rest of 2022 and 2023.

USDJPY traded in a 136.54-137.14 band. The currency pair is pressure by reports that Japanese investors are repatriating proceeds from foreign bond sales and by the soft 10-year Treasury yield which is at 2.80%.

AUDUSD rose, fell, then rallied in a 0.6914-56 range. Australia’s CPI rose 6.1% y/y, a tick lower than the 6.2% expected, which led Goldman Sachs and Deutsche Bank to lower their rate hike predictions to 0.50% from 0.75%, at next week’s meeting.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

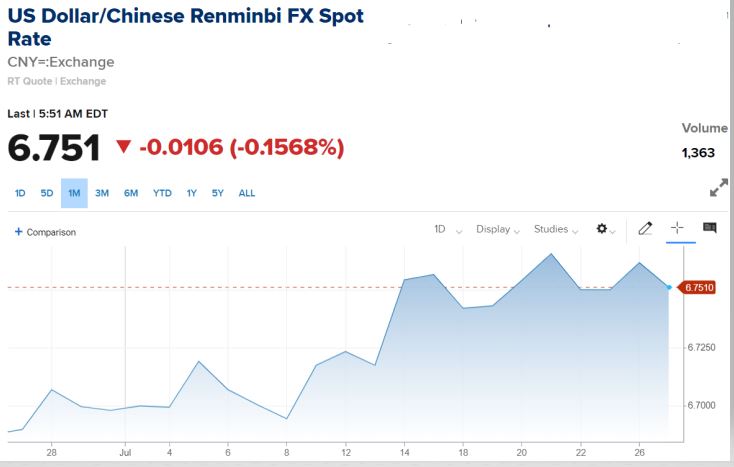

China Snapshot

Today’s Bank of China Fix 6.7731, previous 6.7483

Shanghai Shenzhen CSI 300 fell 0.49% to 4,225.04

Biden/Xi Jinping call scheduled for Thursday

Chart: USDCNY 1 month

Source: CNBC