January 8, 2024

- Soft oil prices weighing on Loonie.

- Friday’s mixed US data muddies interest rate outlook.

- US dollar trading with modest bid.

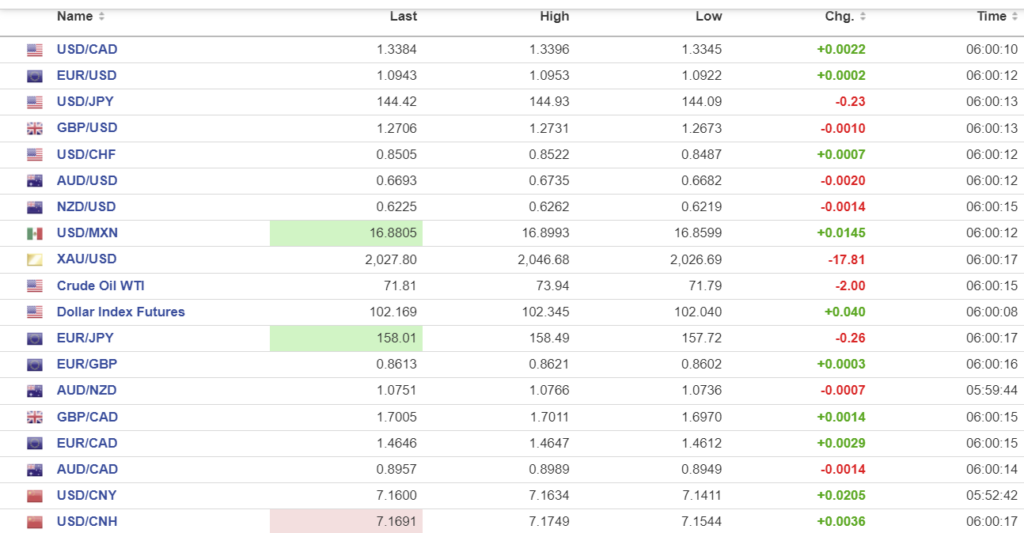

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3382-86, overnight range 1.3345-1.3396, close 1.3366.

USDCAD rallied hard and fast after Friday’s ISM data failed to stem concerns that the Fed may not cut rates as quickly or as low as traders expected. USDCAD did not derive much (if any) benefit from the Canadian employment data even though the unemployment rate was unchanged and average hourly earnings rose. Those result suggest the BoC will be on hold for longer than expected.

Soft oil prices are also underpinning USDCAD. WTI dropped from $73.94/b on Friday to $71.53/b today. Saudi Arabia Aramco cut is price for Arab light to Asian clients by $2.00/b starting February 1. The move suggests that talk of further Opec production cuts being announced Feb. 1 may be premature.

The Canadian data calendar is empty.

USDCAD Technicals:

The intraday USDCAD technicals are bullish above 1.3305 but needing to decisively breech resistance in the 1.3440-50 area to extend the rally. If not, USDCAD is likely to meander inside a 1.3200-1.3350 range.

Longer term, USDCAD is in a uptrend from 2014 that comes into play at 1.2780. that level is guarded by the uptrend from June 2021 at 1.3220 and previous bottoms at 1.3180.

For today, USDCAD support is at 1.334o and 1.3310. Resistance is at 1.3410 and 1.3440. Todays range 1.3330-1.3430.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

“If the most surprising economic performances by a country in the G-10 were Golden Globes categories, the US economy would win a pair of them: Best Economic Growth Performance and Best Employment Data.

Today, traders are reluctantly adjusting to the revised outlook for US interest rates after Friday’s nonfarm payrolls report. The headline numbers suggested that America was still creating jobs, with the unemployment rate being a robust 3.7% and wages rising more than expected. However, it is not as simple as that. Optimistic traders zeroed in on the ISM Services data, which showed ISM Services PMI and ISM employment slowing. They were in the minority, and it led to whip-saw trading.

There isn’t any notable US data today or tomorrow, leaving traders in limbo until Thursday’s inflation report. Asian equity indexes closed negatively, with Australia’s ASX down 0.50%. Japan was closed for a holiday. European bourses are modestly in the red, while S&P 500 futures are down 0.15%. The US 10-year Treasury yield is unchanged at 4.04%.

EURUSD is in the middle of its 1.4409-1.4493 range after a choppy overnight session. Mixed factory orders (actual 0.3% month-over-month but -4.4% year-over-year) offset better-than-expected trade data (Exports 3.7% month-over-month, Imports 1.9%). The EURUSD technicals are bullish while trading above 1.0860.

GBPUSD dropped from 1.2731 to 1.2673, then bounced back to 1.2706 in early New York trading. There wasn’t any UK data, leaving sterling to track Euro moves and US dollar sentiment. GBPUSD is underpinned by speculation that expected Bank of England rate cuts will be delayed and by technicals that are bullish above 1.2610.

USDJPY chopped about in a 144.09-144.93 range, with liquidity hampered by the Japanese holiday. The price action was fueled by US 10-year Treasury yields which traded in a 4.02-4.07% range overnight.

AUDUSD is at the bottom of its 0.6682-0.6735 range due to negative risk sentiment from Chinese growth concerns and the risk of US interest rates remaining unchanged for longer than previously expected.

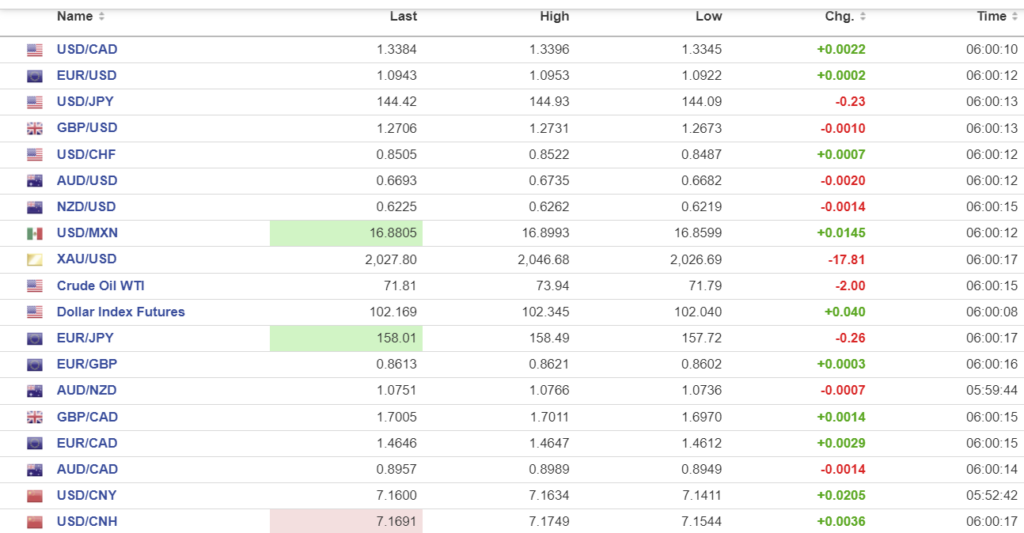

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1006, expected 7.1499, previous 7.1028.

Shanghai Shenzhen CSI 300 fell 1.29% to 3286.06.

Chart: USDCNY and USDCNH hourly from Dec. 21

Chinese stocks are slumping due to a mix of weak data, and fears over domestic growth.

Source: Investing.com