April 29, 2020

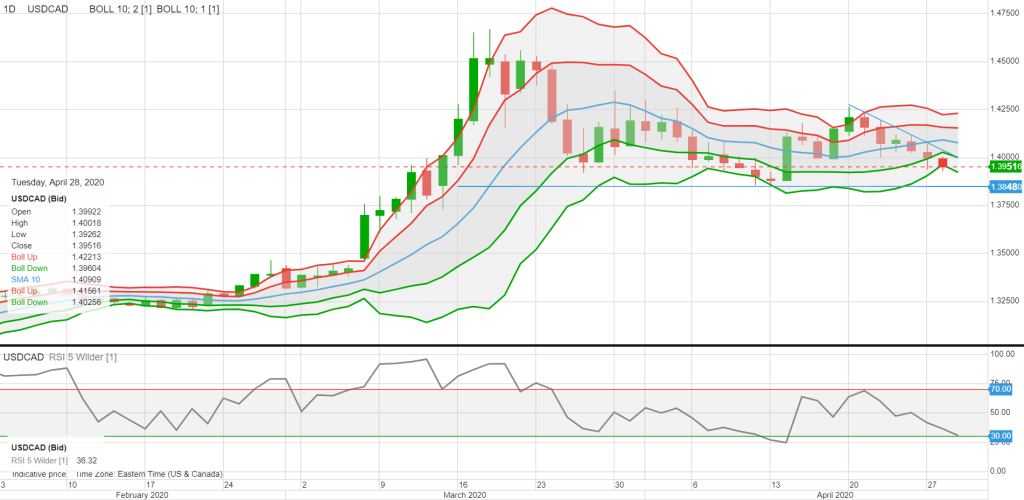

USDCAD open (6:00 am EST) 1.3938-42 Overnight Range 1.3930-1.4002

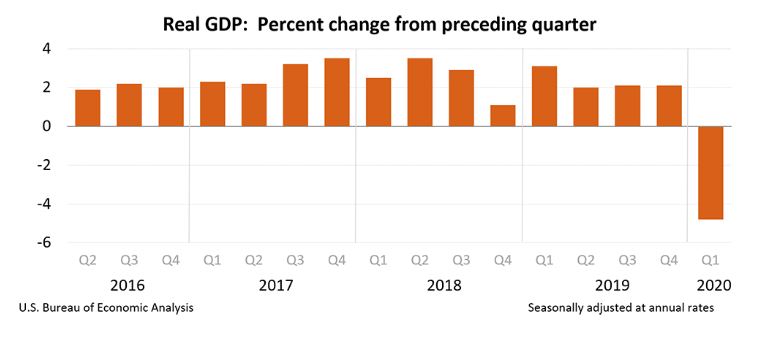

- Real GDP fell 4.8% in Q1 2020

- FOMC to stay in “wait-and-see” mode-no major policy announcements expected

- WTI oil prices surge 14% since yesterday’s close

- US dollar pares overnight gains in early NY trading

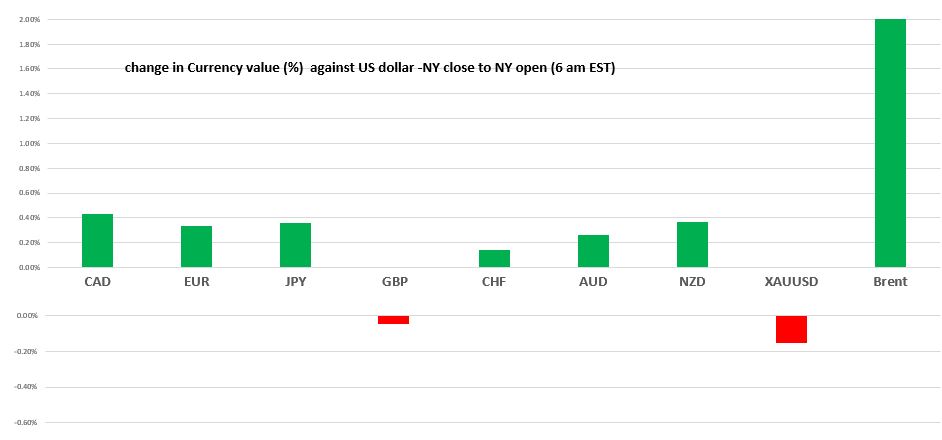

Chart: Change in currency value against US dollar

Source: Saxo Bank/IFXA

FX Recap and outlook: US Q1 2020 GDP was a tad weaker than expected, falling 4.4% compared to forecasts for a 4.0% decline. The US Bureau of Economic Analysis said “he decrease in real GDP in the first quarter reflected negative contributions from personal consumption expenditures (PCE), nonresidential fixed investment, exports, and private inventory investment that were partly offset by positive contributions from residential fixed investment, federal government spending, and state and local government spending.

The US dollar posted small gains following the data, while traders bided their time ahead of today’s FOMC meeting.

The FOMC normally holds eight regularly scheduled policy meetings each year. They held three in March, as they reacted to the coronavirus pandemic, which suggests today’s FOMC meeting will be a non-event for markets.

WTI oil prices jumped to $14.70/barrel from $12.34/b at yesterday’s close, bringing its 24 hour gain to 46%. The move comes on the heels of an ever-so-slightly better API crude inventories report. Weekly crude inventories rose 10 million barrels rather than the 10.5 million barrels expected. Price support stems from profit-taking after the decline since Monday and ahead of the onset of Opec production cuts which start on Friday.

EURUSD reversed yesterday’s New York session losses, climbing from the closing rate of 1.0820 to 1.0867, before dropping to 1.0845 in early New York trading today. Not surprisingly, April Eurozone sentiment data was extremely weak, falling to 67 from 94.7 in March.

GBPUSD rallied in Asia and then sank in Europe, as month-end demand flows were offset by bearish sentiment from recent weak economic reports, lay-off notices from Barclays Bank and British Air, and concerns around the EU/UK trade talks. Those concerns were not evident in the stock market as the FTSE100 is up 0.72% on the day.

USDJPY continued its week-long slide, falling from 106.87 to 106.37, in part due to a slide in US Treasury yields. The 10-year Treasury yield dropped to 0.584% from 0.66%.

AUDUSD and NZDUSD benefitted from better than expected data and demand due to month-end flows. Australia CPI rose 2.2%, y/y while New Zealand’s exports widened to %.14 billion.

USDCAD chopped about in a 1.3932-1.4002 range since yesterday and it currently just above the low. USDCAD selling pressure stems from the rebound in oil prices and rebalancing flow. Oil prices have a long way to go before they provide any real support to the Canadian economy and the rebalancing flows are temporary, which suggests further losses will be limited.

USDCAD technical outlook:

The intraday USDCAD technicals are bearish below 1.4010 looking for a break below 1.3930 to target 1.3870. A move above 1.4010 targets 1.4130. Longer term, RSI and Bollinger band indicators suggest the USDCAD retreat from the March 10 peak has run its course. For today, USDCAD support is at 1.3930 and 1.3870. Resistance is at 1.3990 and 1.4040. Today’s Range 1.3910-1.3990

Chart: USDCAD 1 hour.

Source: Saxo Bank