Photo: BingAI

July 12, 2023

- US headline and Core CPI lower than expected.

- Bank of Canada on deck

- USD continues to slide-JPY the big winner.

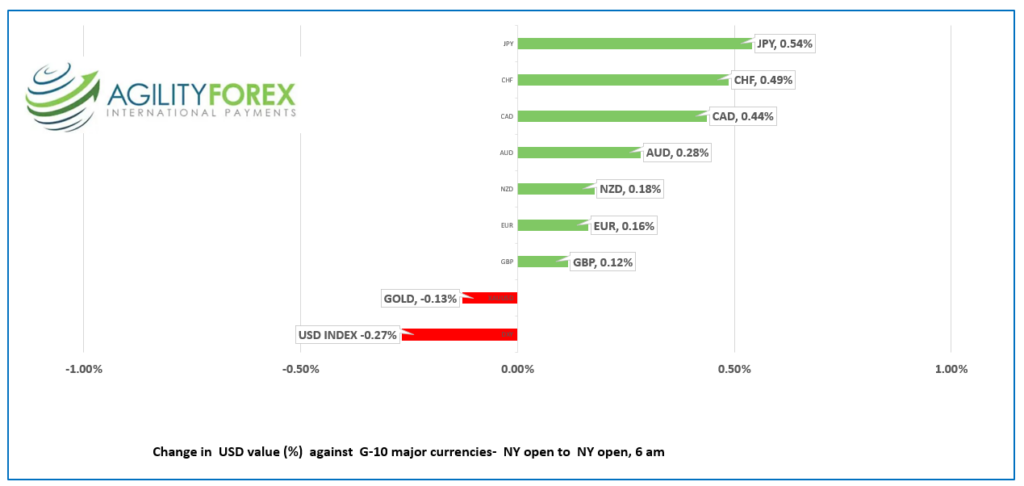

FX at a glance:

Source: IFXA Ltd

USDCAD Snapshot: open 1.3263-67, overnight range 1.3199-1.3280, close 1.3280

USDCAD consolidated yesterday’s losses in a narrow range overnight then probed support in the 1.3200 zone following the weaker than expected US inflation data.

USDCAD downside is exacerbated by broad US dollar weakness vs the G-10 majors and because the Bank of Canada is expected to raise rates by 25 bps today, although it is not a unanimous view the quarterly BoC Monetary Policy Report is also on tap which may provide some clues as to when and at what level, domestic rates will peak.

USDCAD is also under pressure from the resurgence in oil prices. WTI climbed from $73.00/barrel yesterday to $75.22/b overnight due to Russian and Saudi Arabian supply cuts and the IEA forecast predicting tighter supply into year end.

There are no Canadian economic reports today.

USDCAD Technical Outlook

The USDCAD intraday technicals are bearish below 1.3260, looking for a break of support at 1.3200 to extend losses to 1.3150, then 1.3110. A break above 1.3260 negates the downtrend and shifts the focus to 1.3350.

The long term uptrend comes into play in the 1.3000-1.3020 area.

For today, USDCAD support is at 1.3200 and 1.3150. Resistance is at 1.3260 and 1.3310.

Today’s range 1.3170-1.3260.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap

Hallelujah! The inflation beast has been tamed, and the mythical soft landing is about to become a reality. Maybe.

US CPI cooled more than expected in June. Headline CPI rose just 3.0% y/y compared to 4.0% in May and below the forecast for a 3.1% increase. Even better, Core CPI rose 4.8% y/y (forecast 5.0%, previous 5.3%).

The US dollar dropped, stocks rose, and Treasury yields dropped to 3.89% from 3.94% on the news.

Nevertheless, analysts still expect the Fed to hike on July 26, but a second rate hike is debatable.

EURUSD traded in a 1.1008-1.1036 range overnight then rallied to 1.1071 post-CPI supported by expectations of at least two more ECB rate increases before year end.

GBPUSD retreated from 1.2970 to 1.2922 in a mild bout of profit-taking prior to the release of the US CPI numbers then rebounded to 1.2975 after the better than expected result. The uptrend is intact above 1.2860.

USDJPY dropped to 139.32 from 140.36 overnight then fell to 138.77 after the CPI data. Traders are re-evaluating positions on speculation that the Fed is nearly done tightening, while the Bank of Japan is about to start.

AUDUSD tracked broad US dollar moves and chopped about in a 0.66684-0.6741 range with its cousin, NZDUSD in the spotlight.

NZDUSD rallied to 0.6237 then dropped to 0.6188, The RBNZ did not surprise anyone when they left rates unchanged at 5.0%. They were one of the first central banks to begin tightening and the statement suggests they may lead the pack in ending the tightening cycle.

It said “Interest rates are constraining spending and inflation pressures as anticipated and required. The committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range.”

Traders will be closely monitoring the reactions of Fed officials Neal Kashkari, Raphael Bostic, and Loretta Mester, who are scheduled to speak after the release of the CPI data.

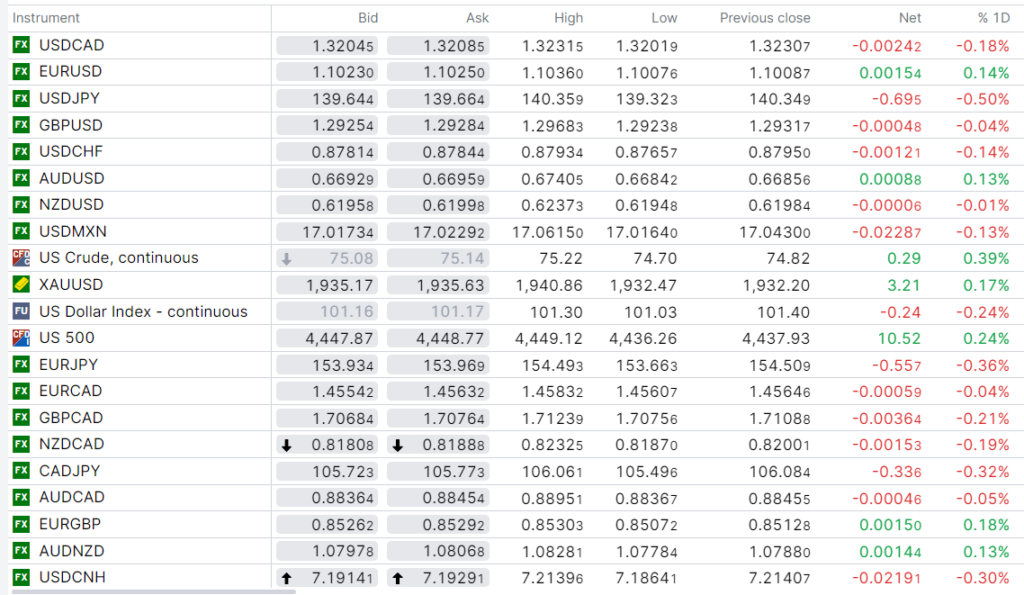

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

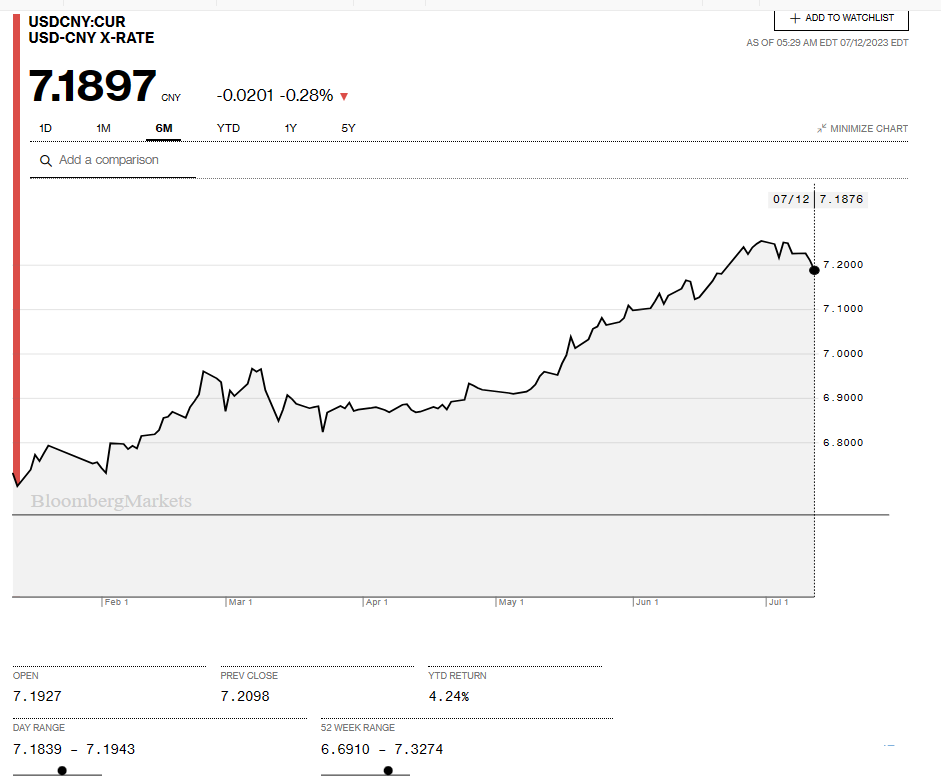

China Snapshot

Bank of China Fix: 7.1765 (expected 7.1935) Previous 7.1866

Shanghai Shenzhen CSI 300 fell 0.67% to 3843.44.

Chart: USDCNY 6 month

Source: Bloomberg