Photo: Hdclipartall.com

January 19, 2023

- Global stocks fall on recession fears.

- US Jobless Claims, Philly Fed, Housing Starts data a tad better than expected

- US dollar rebounds-AUD underperforms.

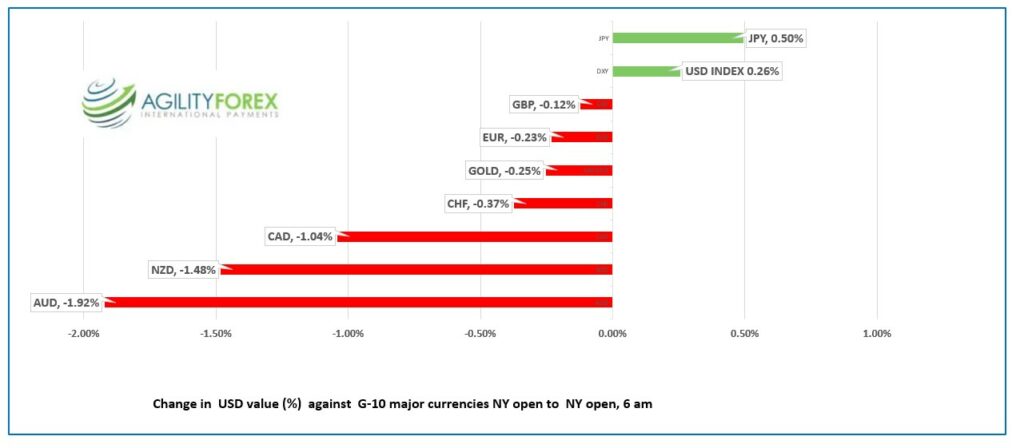

FX at a glance

Source: IFXA Ltd/RP

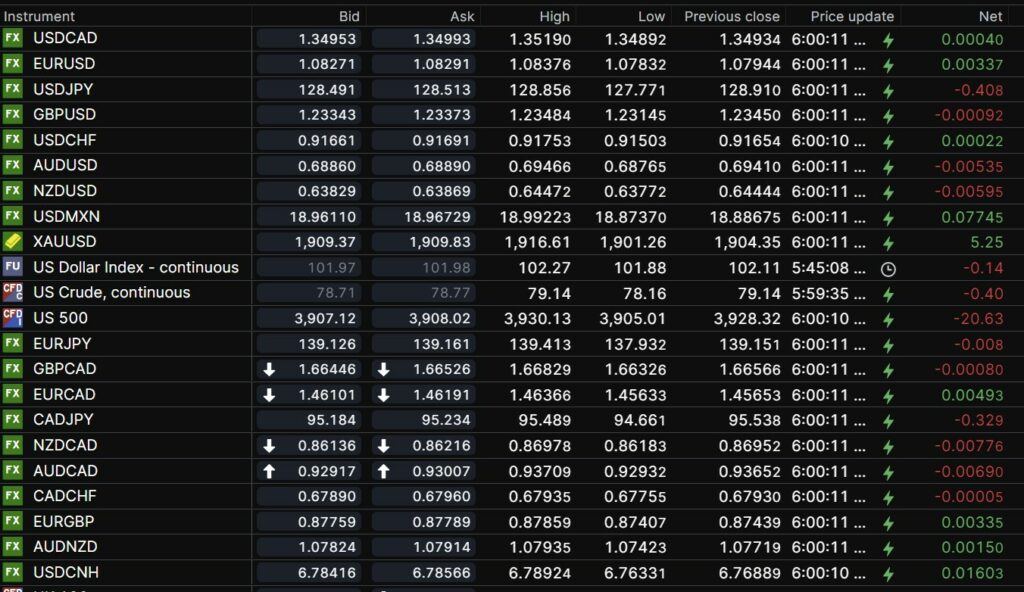

USDCAD Snapshot: open 1.3495-99, overnight range 1.3483-1.3519, close 1.3493

USDCAD rallied on the back of broad US dollar strength due to escalating recession fears. Weak US economic data and hawkish comments from voting members of the FOMC fueled yesterday’s rally and triggered stop loss buying on the move above 1.3460.

Traders took direction from Wall Street and the free-falling S&P 500 index propelled USD/CAD higher. S&P 500 futures are trading 0.83% lower this morning, just above its session low, which is underpinning the currency pair.

The rising dollar derailed the oil rally and WTI dropped from $82.30/barrel yesterday to $78.16/b overnight. API weekly crude stocks data showed inventories rose 7.6 million last week and that news, along with US recession fears ahead of next week’s Chinese New Year holidays weighs on prices.

USDCAD Technical Outlook

The intraday USDCAD technicals flipped to bullish with the break above 1.3460 and are looking for a test of resistance in the 1.3550 area, which is the 50% Fibonacci retracement of the 2023 range. A failure to break above 1.3550 argues for a wider 1.3350-1.3550 consolidation range.

For today, USDCAD support is at 1.3460 and 1.3420. Resistance is at 1.3520 and 1.3560.

Today’s range 1.3430-1.3520

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Recession fears re-emerge.

Weekly jobless claims were 24,000 lower than expected and 14,000 lower than last week, demonstrating the resilience of the US job market.

The Philadelphia Fed Manufacturing Survey was better than expected but still weak. The survey summary said responses “suggest continued overall declines in the region’s manufacturing sector this month. The indicators for current activity and new orders improved from their December readings but remained negative.

The results tempered the slide in S&P 500 futures while leaving the US dollar bid.

Yesterday’s weaker than expected US December data (Retail Sales -1.1%, previous -1.0%) and weaker Producer Prices (actual -0.5% m/m) raised recession fears and drove the US 10-year Treasury yield down from 5.62% to 3.37% at the close.

But even as Treasury yields were falling FOMC voting members were talking about the need for higher interest rates.

Philadelphia Fed President Patrick Harker said, “Hikes of 25 basis points will be appropriate going forward,” and at some point this year Fed policy will be at a level that will restrain activity to help lower inflation back toward its 2% target.”

Dallas Fed President Lorie Logan is in favour of slowing the pace of rate hikes but added “we can offset the effect by gradually raising rates to a higher level than previously expected.”

Wall Street closed with steep losses and the fear of recession theme continued overnight. Asian equity indexes closed mixed. The Nikkei 225 index dropped 1.44% on lingering concerns the BoJ will turn hawkish. Australia’s ASX 200 rose 0.57% despite disappointing jobs data.

European bourses open with losses and continue to slide. The German Dax index is down 1.24%, followed by a 1.23% in the French CAC 40 index. S&P 500 futures are down 0.80% as of 6:00 am.

EURUSD climbed from 1.0783 to 1.0838 in Europe then dropped to 1.0802 in NY trading. Broad US dollar demand post-US data is offsetting hawkish comments from ECB board member and Dutch Central Bank President Klaas Knot. He warned the ECB will hike 50 bps at the next meeting and then continue to raise rates. The EURUSD uptrend is intact above1.0760.

GBPUSD is adrift in a 1.2315-1.2348 range. Recent data argues that the Bank of England will hike rates 50 bps at the February 2 meeting. The intraday GBPUSD technicals are bullish above 1.2305.

USDJPY chopped about in a 127.77-128.86 range with the low seen in Asia. Prices were boosted by EURJPY and GBPJPY with gains capped by expectations for a hawkish tilt to BoJ monetary policy.

AUDUSD climbed from the bottom of its overnight 0.6877-0.6947 range following the US data. The weaker than expected Australian employment report which saw Australian lose 14,600 jobs fueled the selling.

NZDUSD traded in a 0.6367-0.6447 range with the news that Prime Minister Jacinda Arden resigned having no impact on trading.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

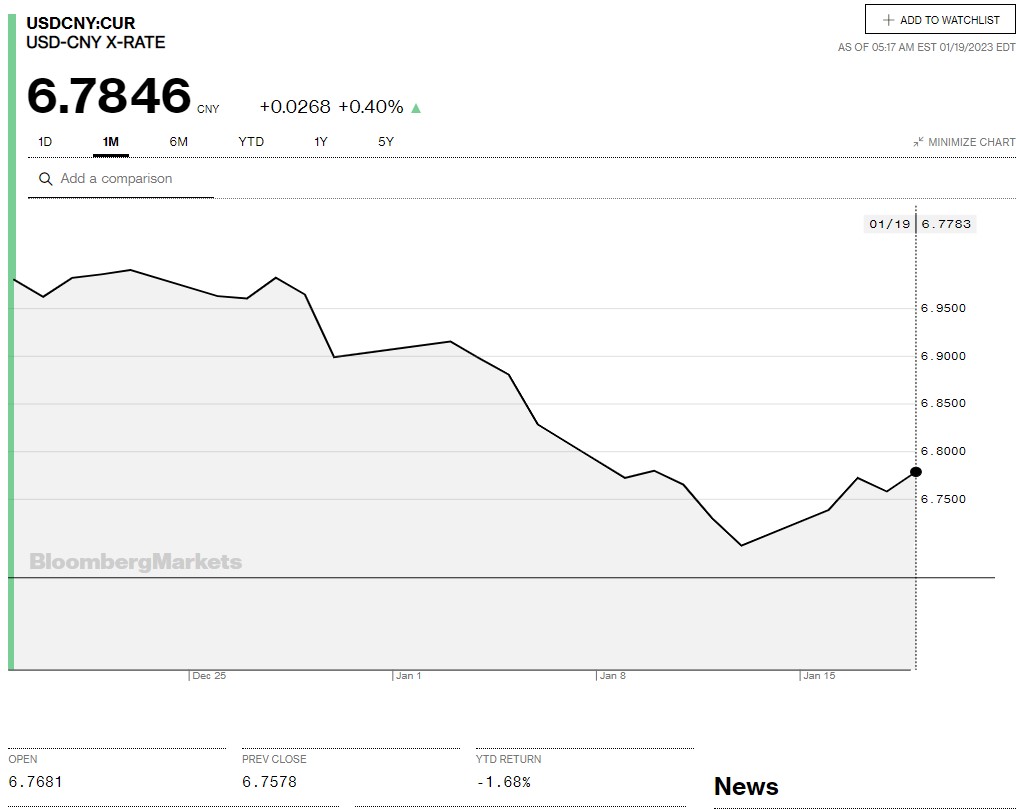

China Snapshot

Today’s Bank of China Fix: 6.7674, previous 6.7602

Shanghai Shenzhen CSI 300 rose 0.62% to 4156.01.

Chart: USDCNY one month

Source: Bloomberg