April 2, 2020

USDCAD open (6:00 am EST) 1.4112-16 Overnight Range 1.4082-1.4195

- WTI prices surge 8.3% on Trump comments and China buying plans

- S&P Futures are nearly flat after paring gains following jobless claims data

- US dollar closed yesterday with small losses and opened this morning on a mixed note

US dollar closed yesterday with small losses and opened this morning on a mixed note

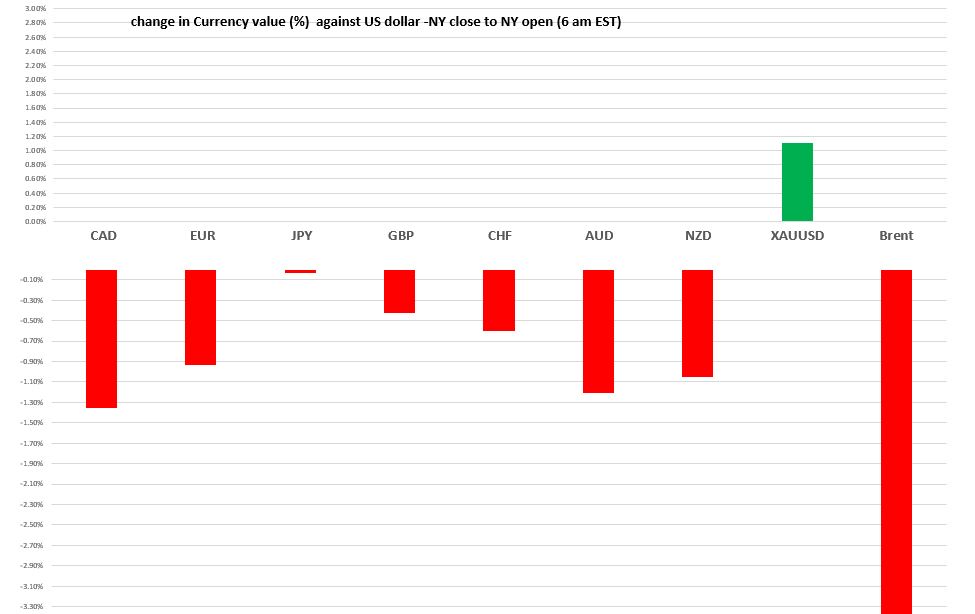

Chart: Currency gain/loss (%) against the US dollar from NY close to NY open (6:00 EST)

Source: Saxo Bank/IFXA

FX Recap and outlook: There was a tiny whiff of positive risk sentiment flitting around FX markets overnight, as evidenced by the slight gains seen in the commodity currency bloc, and tiny losses in the safe-haven currencies, JPY, and CHF. It is hard to see that sentiment lasting, especially with a butt-ugly weekly jobless claims report on tap this morning. And it didn’t.

US jobless claims soared to 6,648,000 in the week ending March 27. They were higher than forecast but it should not have surprised anyone, due to the sheer number of business closures, layoffs and mandatory lockdowns announced in the past week. Nevertheless, the talking heads and print media will be scrambling to outdo themselves with hyperbolic adjectives, which undermined equities and lifted the US dollar.

President Trump said that after speaking with leaders in Russia and Saudi Arabia, he believes a deal to end the oil price war is likely “in a few days.” WTI oil prices were trading around $20.10/barrel following the Energy Information Administration report that US crude inventories rose 13.8 million barrels, as of March 27. Trump’s comments sparked a rally which accelerated when China announced it would begin buying crude for its Strategic Reserves. WTI touched $22.52 before slipping to $22.20 at the New York open.

Expectations for a sharp spike in COVID-19 cases and deaths in Canada and the US will put a damper on trading again today. Worldwide coronavirus cases will soon reach 1 million while deaths are close to 50,000, which has led to wide-scale lockdowns, business closures, and layoffs. They all contribute to poor FX liquidity and volumes.

Sentiment will worsen if the US goes ahead with plans to cancel all domestic flights.

Yesterday’s better than expected US ISM Manufacturing PMI contrasted with the weaker than forecast PMI results for Germany and the Eurozone, which helped drive EURUSD from 1.0968 to 1.0915 overnight. The single currency opened in NY at 1.0935.

GBPUSD traded sideways in Asia, but rallied in Europe, in part due to sales of EURGBP. The UK government’s coronavirus fiscal stimulus package puts the spotlight on the EU’s rather anaemic reaction and disappointment in some quarters with the EU’s refusal to issue the so-called Coronabond. GBPUSD got an added lift from the 0.8% rise in house prices in March.

USDJPY chopped about in a fairly tight 107.06-107.56 range with residual Japanese year-end flows and large option expiries containing price action. There is reportedly around $4.6 billion worth of options expiring today with strikes in the 106.90 and 107.50, areas. Soft US Treasury yields capped topside moves.

AUDUSD and NZDUSD consolidate above recent lows with prices supported by mild US dollar weakness and hopes for an improved growth outlook for China, as it slowly recovers from COVID-19.

USDCAD direction continues to be married to US dollar sentiment and WTI price action. The Federal government and Bank of Canada stimulus actions are in line with those of the G-10, which negates any benefit to the Canadian dollar. Traders are ignoring domestic data because it is stale and for the most part, pre-dates the pandemic.

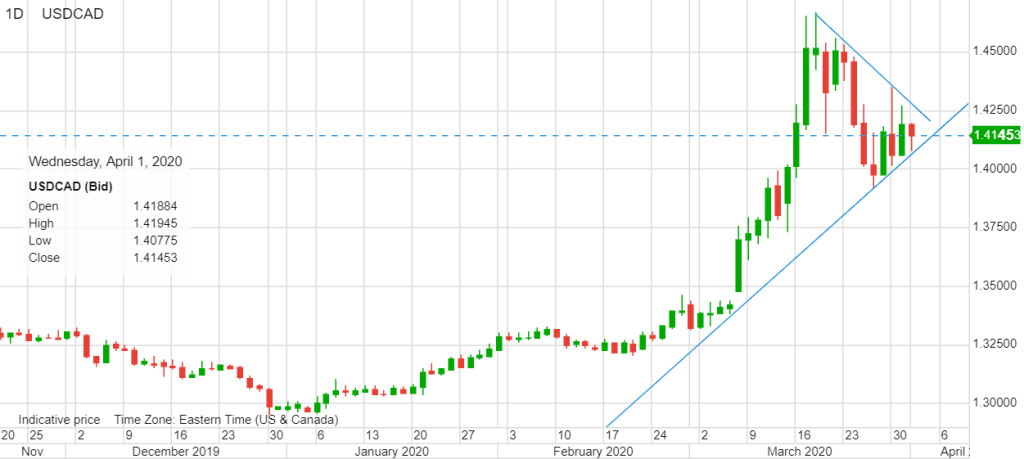

USDCAD technical outlook

USDCAD continues to bounce inside a narrowing wedge between 1.4050 and 1.4295. A break of either side could see a 0.0400 point move. The intraday technicals are modestly bullish above 1.4080, looking for a break of 1.4250 to extend gains to 1.4300. For today, USDCAD support is at 1.4120and 1.4080. Resistance is at 1.4230 and 1.4280

Chart: USDCAD daily

Source: Saxo Bank