Picture: IFXA Ltd

- US PPI data rises 0.6% in October (forecast 0.5% m/m)

- Investor confidence improves in Germany

- US dollar on the defensive as Treasury yields slide

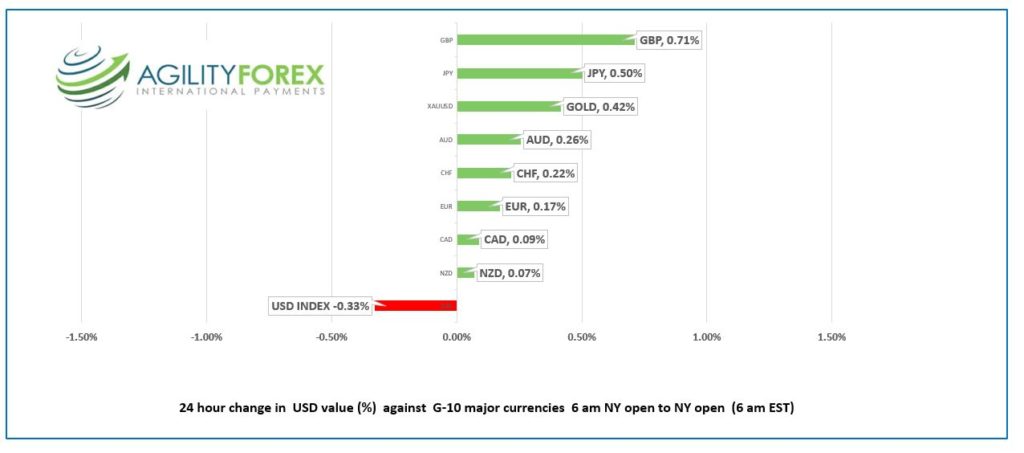

FX at a Glance:

Source: IFXA Ltd/RP

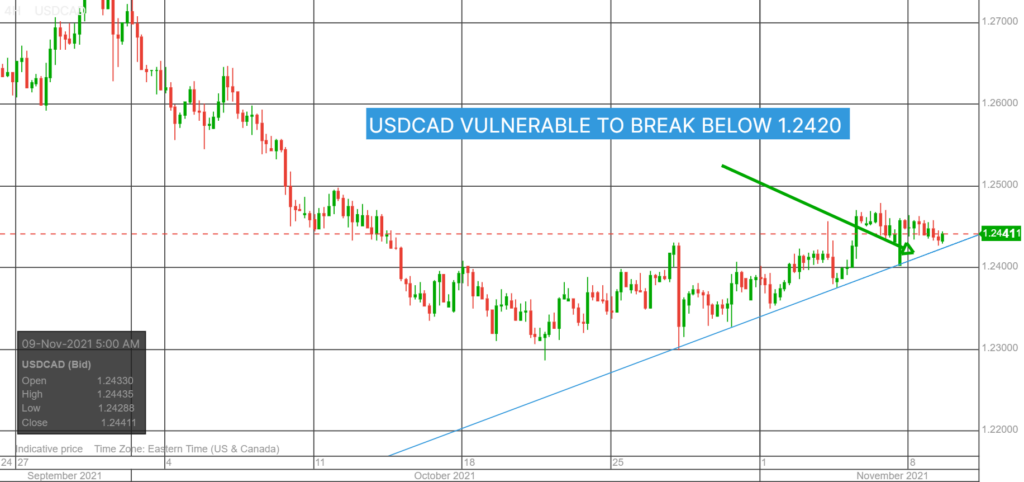

USDCAD Snapshot Open 1.2435-39, Overnight Range 1.2431-1.2458, Previous close 1.2442

USDCAD drifted lower with prices weighed down by rising oil prices, and lower US 10-year Treasury yields. USDCAD is consolidating recent gains but remains well below significant resistance in the 1.2500 area.

WTI is trading with a bullish bias and analysts continue to expect prices to reach $100.00/barrel. The Biden administration is blaming Opec for the price gains. The UAE oil minister countered by saying western nations have discouraged investments in fossil fuels, which has exacerbated supply pressures.

USDCAD did not react to the US PPI data.

Technical view: The intraday USDCAD technicals are bullish while trading above 1.2420 but that level is vulnerable after the currency pair failed to sustain gains above 1.2500. A break below 1.2420 negates the uptrend line from October 27 and suggests further losses to 1.2350.

For today, USDCAD support is at 1.2420 and 1.2390. Resistance is 1.2480 and 1.2510. Today’s range 1.2420-1.2480

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Asia equity markets ignored the positive close on Wall Street and closed with small losses.

European bourses are trading with modest gains while DJIA and S&P 500 futures are flat. Oil prices ticked higher, gold is close to unchanged, and US 10-year Treasury yields are down.

FX markets had a topsy-turvy overnight session as traders adopted a cautious tone following and ahead of a gale of central banker-speak about inflation and inflation reports.

Yesterday, Fed Governor Michelle Bowman speculated that higher house prices would underpin inflation. Chicago Fed President Charles Evans said he believes the jump in inflation is temporary but acknowledged an upside risk to his forecast.

Bank of England Governor Andrew Baily was more wishy-washy. He blamed the rise in inflation on reopening after Covid and said the BoE would have to act if they saw inflation feeding into wages.

ECB President Christine Lagarde repeated her mantra that inflation is transitory.

Today brings more of the same. Christine Lagarde is at it again addressing the 4th ECB Forum on Banking Supervision, talking about “Tomorrow’s banking navigating change.” Fed Chair Powell, BoC Governor Macklem, and BoE Governor Bailey are speaking via videoconference at a Diversity event.

Overshadowing all the central banker angst about inflation are rumours that President Biden interviewed Fed Governor Lael Brainard to replace Fed Chair Powell. She is reportedly on the dovish side of dovish.

US October PPI rose 0.6% m/m and Core PPI rose 0.4%. Both results were higher than they were in September. A large part of the gains were due to higher energy costs

EURUSD inched above 1.1600, reaching 1.1607 before dipping to 1.1589 in NY. Prices got a bit of a boost after ZEW Economic Confidence jumped to 31.7 in October compared to 22.3 in September. The Euro area immigration crisis has flared up. Polish police are preventing hundreds of illegals from entering the country as Belarus authorities escort them to the border. The last time Poland saw this many people massed on their borders in 1939. A dovish ECB, a slowing economy, and a refugee crisis should limit EURUSD gains.

GBPUSD traded in a 1.3550-1.3606 range. The currency pair is underpinned by ongoing expectations that the BoE will raise interest rates in December. Gains may be limited if the European Union follows through on its threat to impose short and medium term sanctions on the UK because the Brits threatened to trigger Article 16.

USDJPY dropped from 113.28 to 112.74 when US 10-year Treasury yields fell to 1.462% in NY after closing at 1.492%.

AUDUSD bounced between 0.7392 and 0.7430 as prices tracked broad US dollar sentiment. NZDUSD outperformed against AUDUSD. Both currency pairs are steady, awaiting US CPI on Wednesday.

Chart of the Day: Gold

Source: Investing.com

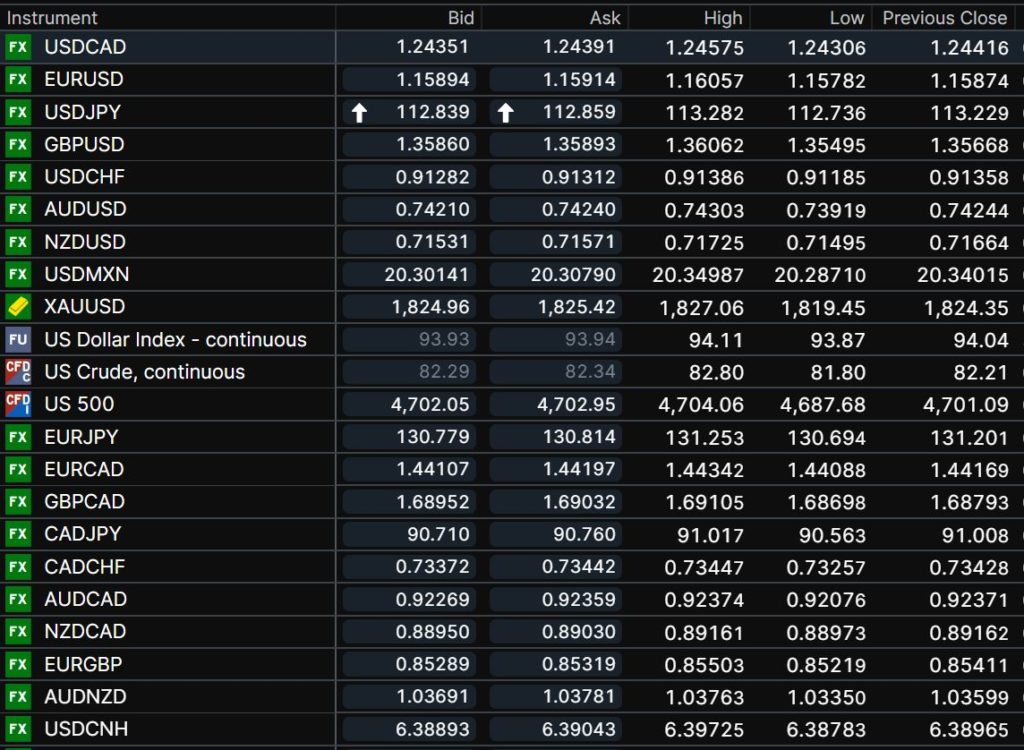

FX open, high, low, previous close

Chart: Saxo Bank

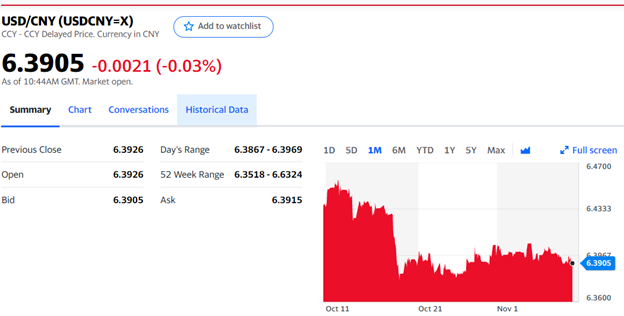

China Snapshot

Today’s Bank of China Fix 6.3903, Previous 6.3959

Shanghai Shenzhen CSI 300 fell 0.03% to 4.846.74

Reports suggesting China unlikely to cut interest rates

Chart: USDCNY 1 month

Source: Yahoo Finance