Photo: publicdomainpictures.net

February 16, 2023

- S&P Futures drop, US dollar rises after PPI rises more than expected.

- BoC Governor and two Deputy governors speaking today.

- US dollar opens mixed but rallies after data.

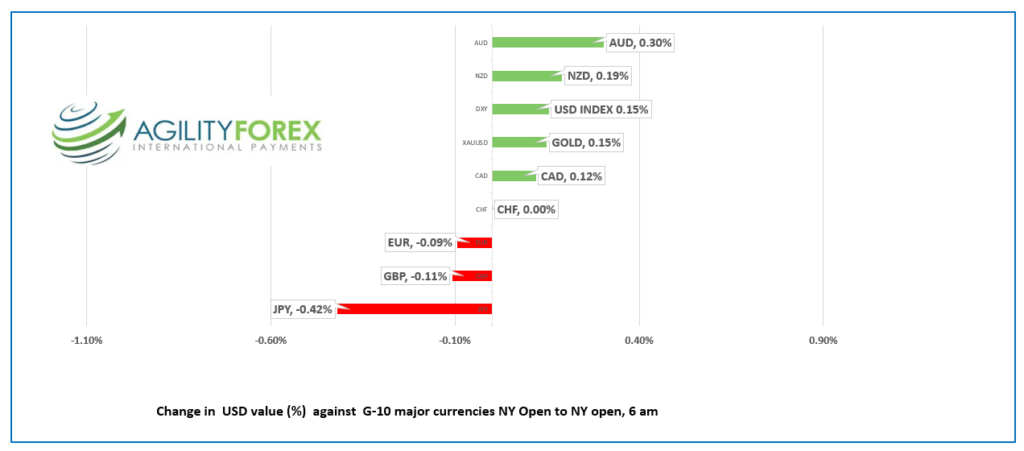

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3483-87, overnight range 1.3360-1.3430, close 1.3394

USDCAD continues to ping-pong between 1.3270 and 1.3460 with domestic data overshadowed by the US interest rate outlook.

BoC Governor Tiff Macklem and Deputy Governor Carolyn Rogers testimony to the House of Commons Standing Committee on Finance. Another Deputy Governor, Paul Beaudry is speaking about “The importance of the Bank of Canada’s 2% inflation target.” In Edmonton at the end of the day.

Last Friday’s stellar employment report led to speculation that the BoC may have announced a pause in rate hikes prematurely. Analysts are hoping the BoC speakers address the issue.

WTI oil traded in a $78.08/b-$79.51/b range. Yesterday, the EIA reported a steep rise in US crude inventories (16.283 million barrels) in the week ending February 10, which weighed on prices. Meanwhile China is expected to increase its import of Russian crude by 500,000 m/bd to 2.2 million b/pd. Xi Jinping thanks the west for imposing Russian sanctions as cheap oil helps him to jumpstart China’s post-covid zero economy.

USDCAD Technical Outlook

The intraday USDCAD technicals are mildly bullish above 1.3320, looking for a break above 1.3450 to extend gains to 1.3510. A move below 1.3320 targets support congestion in the 1.3270-1.3320 zone

Longer term, USDCAD is directionless between the 100-day moving average at 1.3517 and the 200-day moving average at 1.3240.

For today, USDCAD support is at 1.3340 and 1.3310. Resistance is at 1.3460 and 1.3510

Today’s range 1.3370-1.3460

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Yesterday, equity traders dismissed economic reports, which not only suggested that the US economy is still firing on all cylinders but also that the Fed still needed to raise interest rates. Higher interest rate? Big deal. They bought stocks, feeling empowered by the US 10-year yield gains seemingly capped at 3.80%, and the S&P 500 closed with a 0.35% gain,

Well, they changed their minds this morning. The US employment picture remains tight with weekly jobless claims rising 194,000, below the forecast for a 200,000 increase. In addition, January Producer Prices surged 0.7% m/m (forecast 0.4%, previous -0.2% m/m) and 6.0% y/y (forecast 5.4%). Those results do not do anything for the “inflation is falling” story and further support Fed Chair Powell’s hawkish rate outlook.

The Philadelphia Fed Manufacturing survey was fa weaker than expected at -24 (forecast -74, previous -8.9)

All of the above results boosted the US dollar and knocked S&P 500 futures down 1.14%.

EURUSD fell to 1.0671, post-data, after drifting in a 1.0688-1.0722 range overnight.

Hawkish comments from ECB President Christine Lagarde repeating that rates would rise 50 bps in March, were somewhat tempered by comments from Italian Central Bank Deputy governor Fabio Panetta. He injected a note of caution saying “With rates now moving into restrictive territory, it is the extent and duration of monetary policy restriction that matters. By smoothing our policy rate hikes, that is, moving in small steps, we can ensure that we calibrate both elements more precisely in the light of the incoming information and our reaction function.”

GBPUSD dropped to 1.1980 in NY after peaking at 1.2073 in Europe. before retreating. Traders have shrugged off the modestly softer UK inflation data which some believed would temper the Bank of England’s enthusiasm for raising rates. In addition, prices firmed on the back of mildly improved risk sentiment.

USDJPY jumped to 134.33 after spending the overnight session in a 133.61-134.16 range, coinciding with the US 10 -year Treasury yield touching 3.842% in NY trading.

AUDUSD dropped, popped, then dropped again, trading in a 0.6869-0.6935 range. The Australian employment report was far weaker than expected (jobs -11,500 vs forecast 20,000) with the unemployment rate ticking higher to to 3.7% from 3.5%.

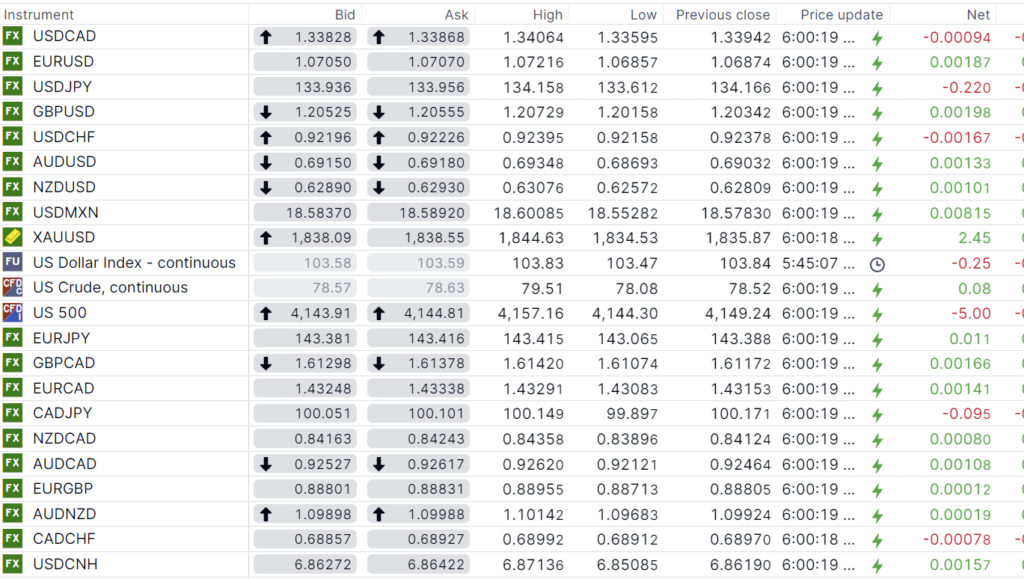

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

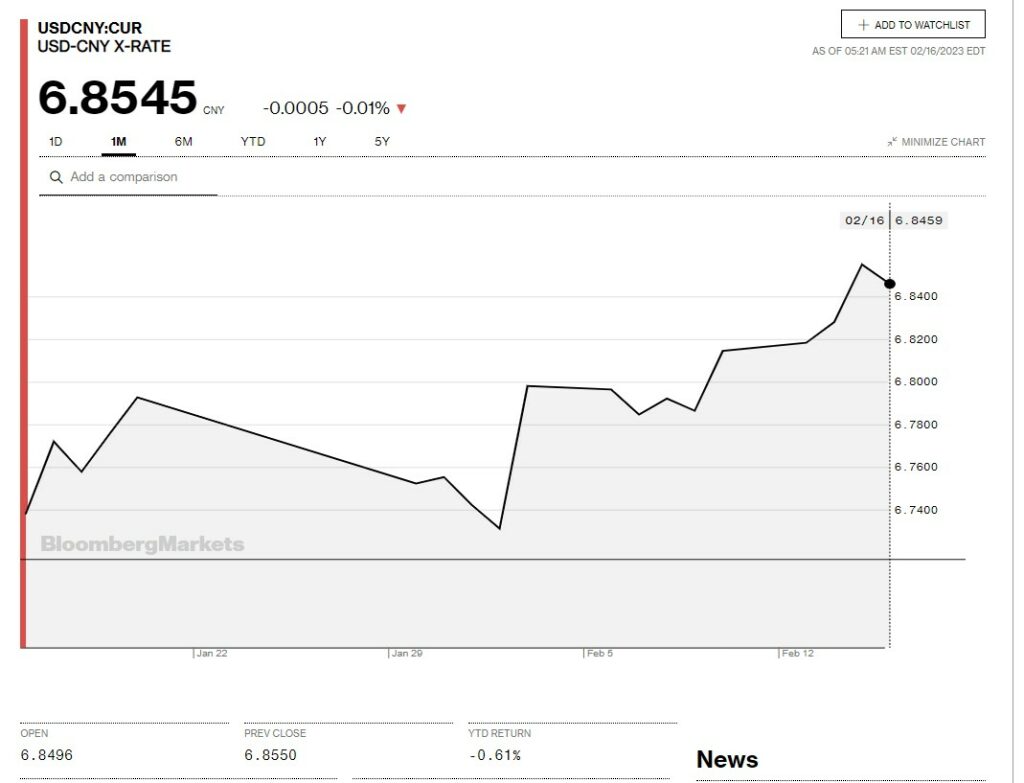

China Snapshot

Bank of China Fix: 6.8519, Previous: 6.8196

Shanghai Shenzhen CSI 300 fell 0.73% to 4093.49.

PboC to increase capital market support for logistics and infrastructure projects.

Chart: USDCNY 1 month

Source: Bloomberg