Source: Pixabay

- Fed-speak and recession talk sink stocks, lift greenback

- Euro-area inflation was 10.6% in October vs 9.9% in September

- US dollar recoups Post-PPI losses, AUD underperforms

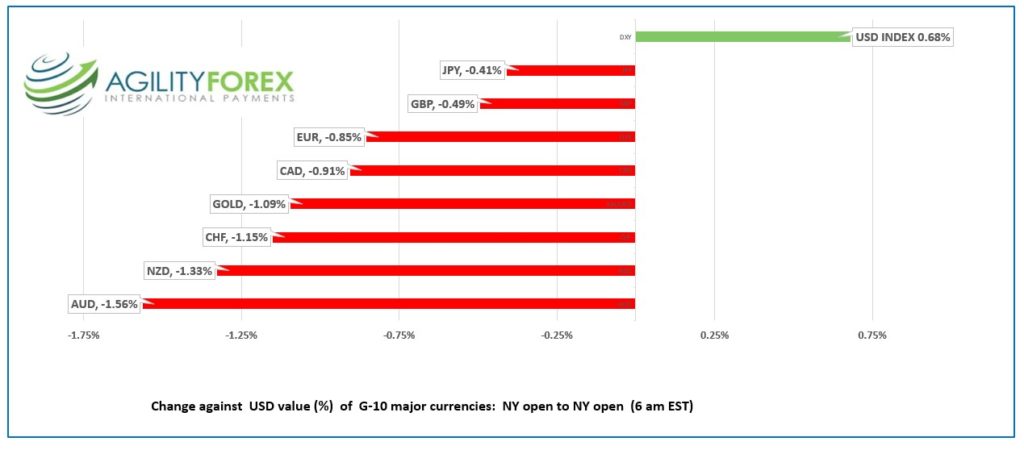

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3367-71, overnight range 1.3307-1.3399, close 1.3328

The USDCAD price action around the October inflation release was muddled as it coincided with the better-than-expected US Retail Sales report. The US data trumped the Canadian news as the strong retail sales data gave the US dollar legs.

Canada CPI was as expected (actual 6.9% y/y) but the results opened a debate about inflation peaking. If you visit a store, restaurant or buy anything, then you know prices are still rising.

WTI oil prices slipped from $85.41/b to $83.93/b due to fears the increase in Covid cases in China will delay the easing of Covid-zero restrictions.

USDCAD price action will track S&P 500 moves and at the S&P 500 futures are down 1.33%.

USDCAD Technical outlook

The USDCAD technicals are trading flipped to bullish with the break of 1.3340, the downtrend line that started November 4. A break above 1.3450 will extend gains to the 1.3580 area. A move below 1.3280 targets 1.3230 then 1.3210.

For today, USDCAD support is at 1.3330 and 1.3280. Resistance is at 1.3410 and 1.3450

Today’s range 1.3330-1.3430

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar rallied overnight following another round of hawkish Fed-speak that pushed back against the notion of a Fed pause.

San Francisco Fed President Mary Daly told CNBC news yesterday that “Pausing is off the table right now. It’s not even part of the discussion.”

Fed Governor Christopher Walker didn’t buy into the inflation peaking narrative after the recent CPI and PPI data. He said “I will not be head-faked by one report. We’ve seen this movie before.”

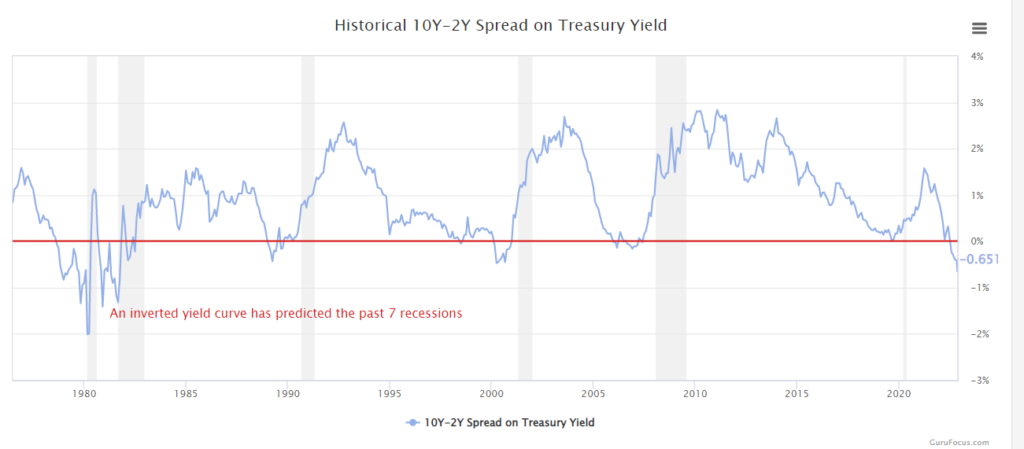

Bond traders concluded that the risk of higher Fed rates from current levels underscored the risk of a recession and drove the 10-year Treasury yield to 3.736% as of 6:27 am in NY today.

The favoured recession barometer, the US 10-year-2-year yield spread, widened to a negative 65.1.

Today, weekly jobless claims were a tad better than expected, falling 4,000 to 222,000 last week, another sign that the US economy is still perky. In addition, October building permits were 1.425 million, beating the estimate but below last month.

Asia equity indexes closed on a mixed note. The Nikkei 225 dipped 0.35% while Australia’s ASX 200 ticked up 0.19%. European bourses are trading lower, led by the French CAC 40 which lo is down 0.90%. which is unchanged. S&P 500 futures are down 1.33%. WTI oil lost 1.83% while gold prices fell 0.68%.

EURUSD dropped from 1.0406 in Asia to 1.0316 in NY due to negative risk sentiment and wide-spread US dollar demand. EuroStat reported “The euro area annual inflation rate was 10.6% in October 2022, up from 9.9% in September. A year earlier, the rate was 4.1%. European Union annual inflation was 11.5% in October 2022, up from 10.9% in September. A year earlier, the rate was 4.4%.”

GBPUSD plunged from 1.1956 in Asia to 1.1780 in NY. Chancellor Jeremy Hunt delivered his Autumn Statement which is described as an austerity budget and includes £55 billion of tax increases. A break below 1.1750 will extend losses to 1.1350

USDJPY closed at 139.54 then traded in a 138.88-140.52 range overnight. Prices slid in Asia then rebounded in Europe due to renewed US dollar strength vs the majors. Traders ignored remarks by BoJ Governor Haruhiko Kuroda who continued to yammer about the need for monetary easing to support the economy.

AUDUSD traded in a 0.6638-0.6750 range. The currency pair rallied in Asia after a traders were surprised by a stronger-than-expected employment report. Australia gained 32,200 new jobs (forecast 15,000) and the unemployment rate dropped to 3.4$ from 3.6%. Analysts suggested the results meant the RBA rate hikes would continue with the odds for a 25 bp bump at 50-50.

NZDUSD mirrored AUDUSD moves and is trading at the bottom of its 0.6070-0.6167 range in NY.

Fed Vice Chair Michelle Bowman speaks today.

Chart of the Day- US Yield Curve Inversion

Source: gurufocus.com

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

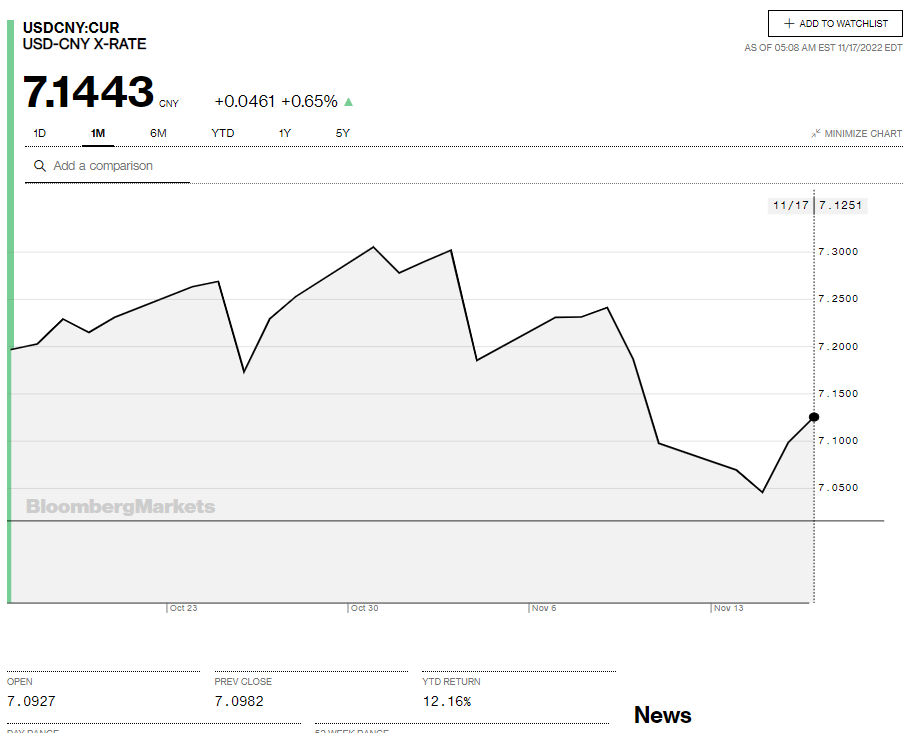

China Snapshot

Today’s Bank of China Fix: 7.0655, previous 7.0363

Shanghai Shenzhen CSI 300 fell 0.41% to 3818.66

New Covid cases rise to 2,388 from 1,623 yesterday. The Peoples Daily reports China is able to achieve Covid-Zero.

Chart: USDCNY 1 month

Source: Bloomberg