Photo: Wikimedia

- UK Inflation tops 10% in July

- RBNZ hikes rates 50 bps to 3.00%

- US dollar opens mixed ahead of FOMC minutes

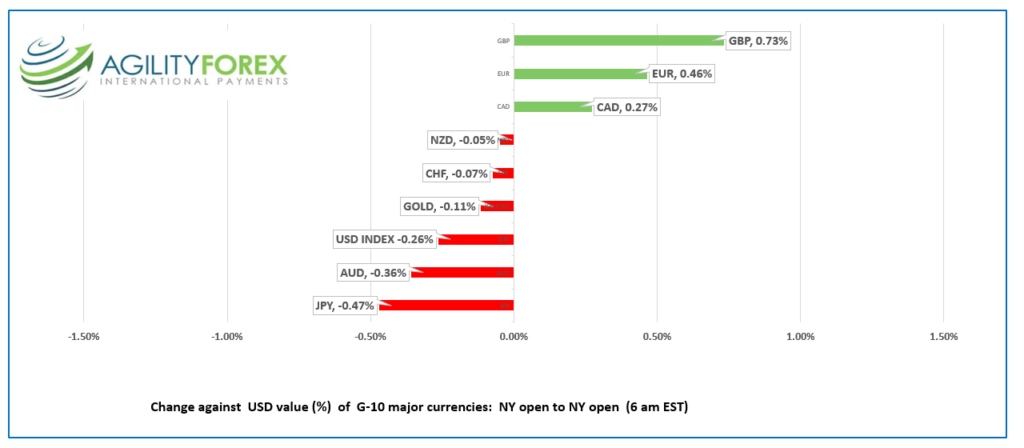

FX at a glance:

Source: IFXA Ltd/RP

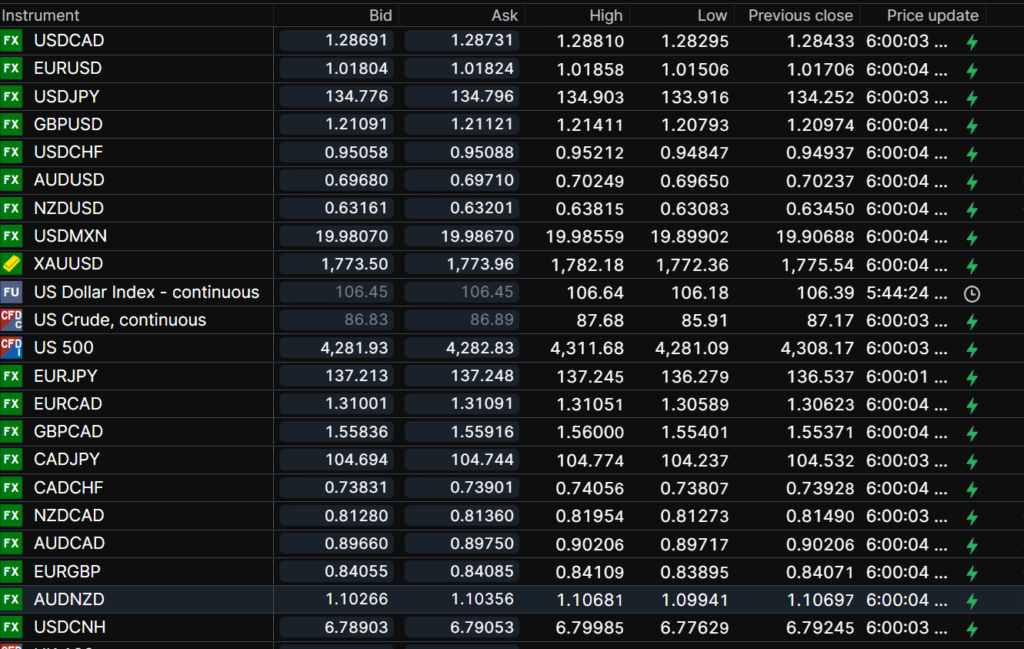

USDCAD Snapshot: open 1.2869-73, overnight range 1.2830-1.2917, close 1.2843

USDCAD staged a full-fledged retreat yesterday after Canada’s inflation report was released. Headline CPI dipped to 7.6% y/y in July, while Core-CPI-ticked down to 6.1% from 6.2%.

USDCAD dropped from 1.2910 just prior to the release and reached 1.2826 by mid-afternoon. The media rejoiced. Hallelujah! Inflation has peaked.

Saying inflation has peaked sounds a tad premature. Food, natural gas, airfares and hotel prices are still climbing, and the Bank of Canada will still need to raise rates aggressively.

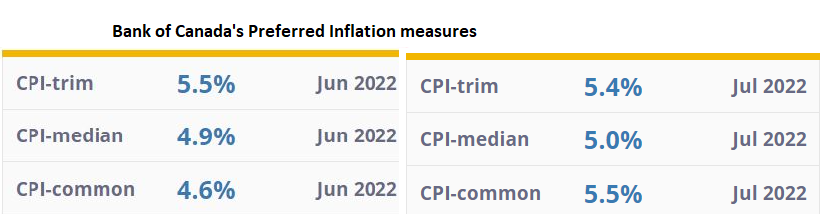

The BoC’s preferred inflation gauges moved higher, which makes a 75 bp rate bump in September likely.

Source: BoC

Claiming yesterday’s USDCAD sell-off was all because of the inflation numbers is not accurate. CPI was part of the story, but the S&P 500 index rally from 4276 to 4325 was the true catalyst. If life is good in America, traders gravitate to more riskier assets. Thin, summer liquidity was another factor.

WTI oil prices plunged to $85.75/barrel yesterday morning from $90.61/b then consolidated those losses in a $85.90-$87.65 band overnight. The volatility stemmed from conflicting Iran/US nuclear deal rumours and modestly lower US crude inventory data.

USDCAD recouped all its post-CPI losses and tested resistance in the 1.2920 area in NY today.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish above 1.2830, looking for a move above 1.2930 for a retest of the 1.3000 resistance zone. A break below 1.2830 targets 1.2805 then 1.2760. Longer term, the summer range of 1.2730-1.3080 remains intact. For today, USDCAD support is at 1.2830, and 1.2805. Resistance is at 1.2920 and 1.2950. Today’s range: 1.2860-1.2950

Chart: USDCAD Daily

Source: Saxo Bank

G-10 FX recap and outlook

US July Retail Sales were a mixed bag but largely positive. Retail Sales were 0.0% in July, a tick below the 0.1% forecast but Retail Sales, ex-autos rose 0.4% m/m, beating the forecast of 0.1% decline.

Irrational exuberance is alive and well in America. Bed Bath & Beyond Shares surged 349% in just three weeks. Walmart’s quarterly earnings results lit a fire on Wall Street, with traders conveniently ignoring the retailers warning that inflation has shifted sales into less high-margin products. Target Corp) TGT: NYSE) reported a 90% drop in quarterly earnings today.

Markets are emboldened by speculation that inflation has peaked, and recession fears are unwarranted, blissfully ignoring warning signs worldwide.

China’s economy is slumping, and the PboC is cutting interest rates. The Reserve Bank of New Zealand hiked rates by 50% and said another 100 bps increase is in the pipeline. The Eurozone is a basket case, exacerbated by the Russia/Ukraine war. Middle East countries continue to trade missiles with each other, and $5.00/gallon US gas prices have helped turn Iran’s nuclear ambitions into an acceptable solution in return for oil.

FX traders are twiddling their thumbs ahead of the 2:00 pm release of the FOMC minutes from the July 27 meeting. The minutes may be stale, but they may shift the dialogue to the risk of higher rates rather than suggesting this rate hike cycle will end in December.

EURUSD drifted in a 1.0151-1.0186 band. The single currency continues to consolidate its losses from Monday while ignoring Eurozone data. Eurozone Q2 GDP dipped to 3.9% y/y compared to the forecast of 4.0% y/y, and employment increased 0.3%

GBPUSD traded erratically in a 1.2079-1.2141 range. UK inflation hit a forty year peak, rising 10.1% y/y, compared to 9.4% in June and above the forecast of 9.8%. The news wasn’t unexpected, and GBPUSD was underpinned by speculation the Bank of England would be forced to hike rates further and faster.

USDJPY is on a tear, rising from an overnight low of 133.92 to 135.39 following the US Retail Sales data and a rise in the US 10-year Treasury yield to 2.889%. Japanese economic data (Machine Orders and Trade) was ignored.

AUDUSD plunged from its Asian peak of 0.7025 to 0.6920 in NY due to position due to broad US dollar demand from retreating Wall Street Futures and position adjusting ahead of the FOMC minutes.

NZDUSD jumped to 0.6382 after the RBNZ hiked rates by 50 bps and issued a hawkish statement suggesting another 100 bps of increases were in the cards. Those gains evaporated in Europe and NY and prices plunged to 0.6274,

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

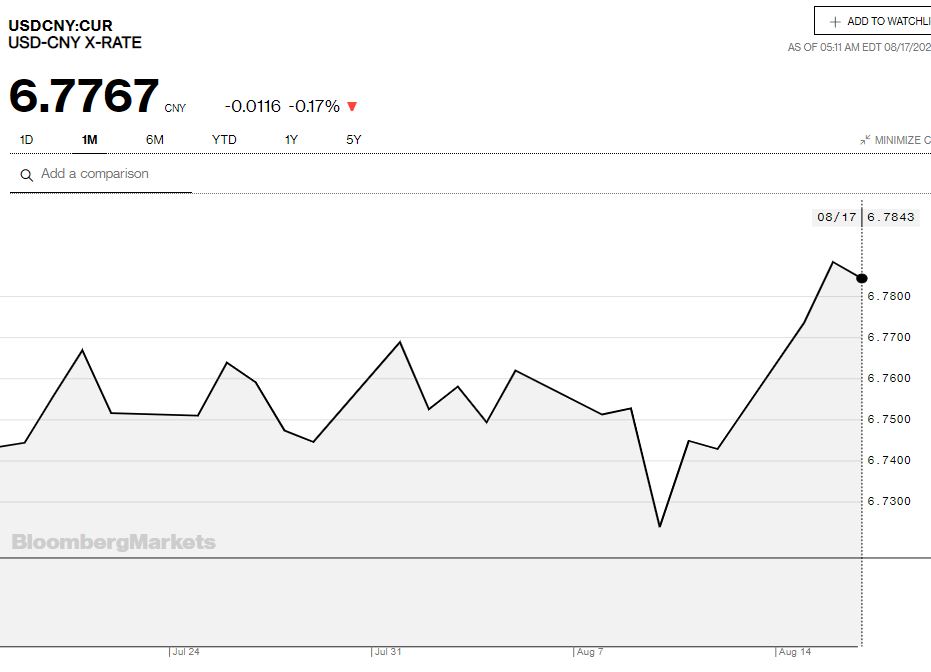

China Snapshot

Today’s Bank of China Fix: 6.7863, previous 6.7730

Shanghai Shenzhen CSI 300 rose 0.94% to 4,216.96

Bloomberg columnist John Authors suggests the recent 10 bp cut in the 1 year rate is evidence that central bankers believe the Chinese economy is in a worse state than it appears.

Chart: USDCNY 1 month

Source: Bloomberg