Photo: Hdclipartall.com

January 18, 2023

- BoJ leaves rates and policy unchanged-surprise.

- US Retail Sales and Producer Prices lower than expected.

- US dollar drops across the board, except against JPY

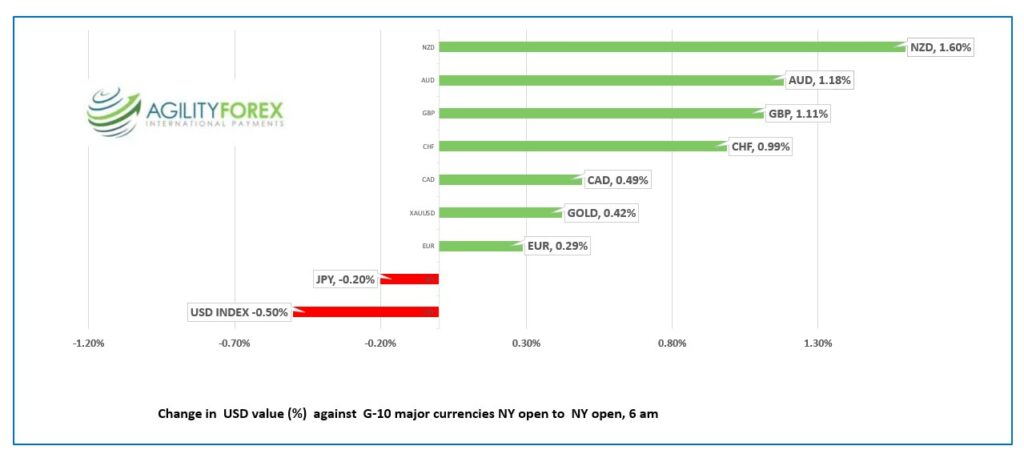

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3355-59, overnight range 1.3353-1.3408, close 1.3390

USDCAD drifted lower overnight on the back of broad US dollar weakness.

USDCAD did not react to yesterday’s top-tier CPI data so its lack of a reaction to Canadian Industrial Production and Raw Material Price index data is not surprise. For the record, they were both sharply lower than expected, supporting views that domestic inflation has peaked.

WTI oil prices are at the top of the overnight $80.58/b to $81.86 range. Prices rose after comments from Opec Secretary General Haitham Al Ghais and the IEA oil market report. Mr Ghais said that the combination of falling Russian crude supplies and increasing Asian demand for oil would underpin oil prices. The IEA predicts that oil demand will increase by 1.9mln BPD to a record of 101.7mln BPD.

USDCAD direction continues to be determined by risk sentiment moves as measured by the S&P 500.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3420 looking for a break below the 11.3340-1.3350 area to extend losses to 1.3310 then 1.3220. A break above 1.3420 suggests additional 1.3340-1.3480 consolidation.

A break below 1.3230 (50% retracement of Jun-Oct 22 range) puts the 61.8% Fibonacci retracement level of 1.3060 in play, which if broken targets 1.2840.

For today, USDCAD support is at 1.3340 and 1.3310. Resistance is at 1.3420 and 1.3460.

Today’s range 1.3340-1.3440

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

US Retail Sales were dismal in December, falling 1.1%, compared to a 1% drop in November as higher interest rates and high inflation turn consumers cautious.

Producer Prices fell 0.5% m/m in December dragging the year over year number to 6.2% from 7.3%. That result supports the “inflation has peaked” camp.

Overnight, the Bank of Japan took center stage in Asia.

Many traders anticipated that the BoJ would tweak policy again, perhaps by raising the 0.5% yield curve control cap. They didn’t. The Japanese yen tanked against the US dollar and from cross-currency demand, particularly NZDJPY and EURJPY.

Positive FX risk sentiment got an added boost from comments by Chinese Vice President Liu He comments from Davos yesterday. He declared China was open and saying, “foreign investments are welcome.”

The major Asia equity indexes closed with gains led by a 2.5% surge in Japan’s Nikkei 225 index. Australia’s ASX 200 squeaked out a 0.10% gain. European equity traders are cautious, with the major indexes trading on either side of unchanged. S&P 500 futures are 0.30% higher and gold has climbed 0.66% to $1921.49 (as of 6:am PT).

EURUSD rallied from 1.0767 to 1.0871 fueled by EURJPY demand after the BoJ left policy unchanged. The single currency has been whip-sawed by comments from ECB officials in the past 24 hours. Yesterday, Bloomberg quoted the ubiquitous “unnamed officials” who claimed the prospect of a 25 bp rate hike is gaining support, even though ECB President Christine Lagarde indicated in December that a 50 bp hike was likely. Today, another ECB official, Francois Villeroy said “We must stay the course in our battle against inflation; it’s not yet won.”

ECB Harmonized CPI fell 0.4% in December (forecast -0.3%) and EURUSD dipped modestly on the news.

GBPUSD is at the top of its 1.2256-1.2386 range after UK inflation was lower than expected in December CPI rose 10.5% y/y compared to the forecast for a 10.6% increase and the 10.7% level in November. Core-CPI rose 6.3% y/y, unchanged from November. The Retail Price index dipped to 13.4% y/y from 14% previously. GBPUSD rallied on the data in anticipation the BoE will hike rates by 50 bps at the next meeting.

USDJPY soared from 128.14 to 131.57 in the wake of the “no-change” BoJ monetary policy announcement. Traders were obviously positioned for a hawkish tweak and the steep rally is evidence of them unwinding positions. That rally is being rapidly unwound in Europe and early New York trading with USDJPY trading at 129.14 (as of 7:00 am) because a) the BoJ still plans to tighten policy this year and b) the US 10-year Treasury yield has slid down to 3.48% from its overnight peak of 3.56%.

AUDUSD and NZDUSD rallied on the back of the broad US dollar weakness and talk about China being open for business. NZDUSD traded in a 0.6425-0.6489 range, while AUDUSD traded in a 0.6975-0.7035 band. Australian employment data is due tomorrow.

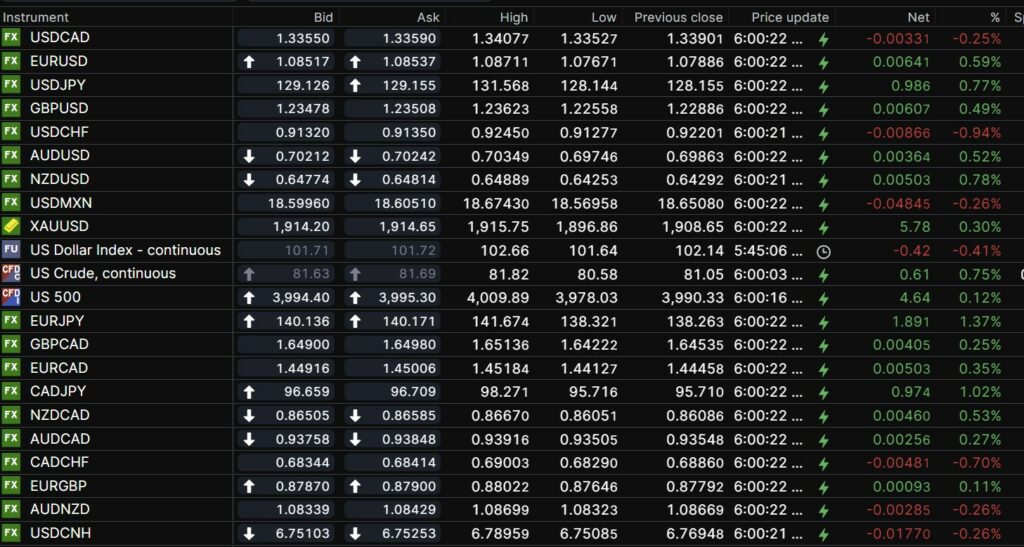

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

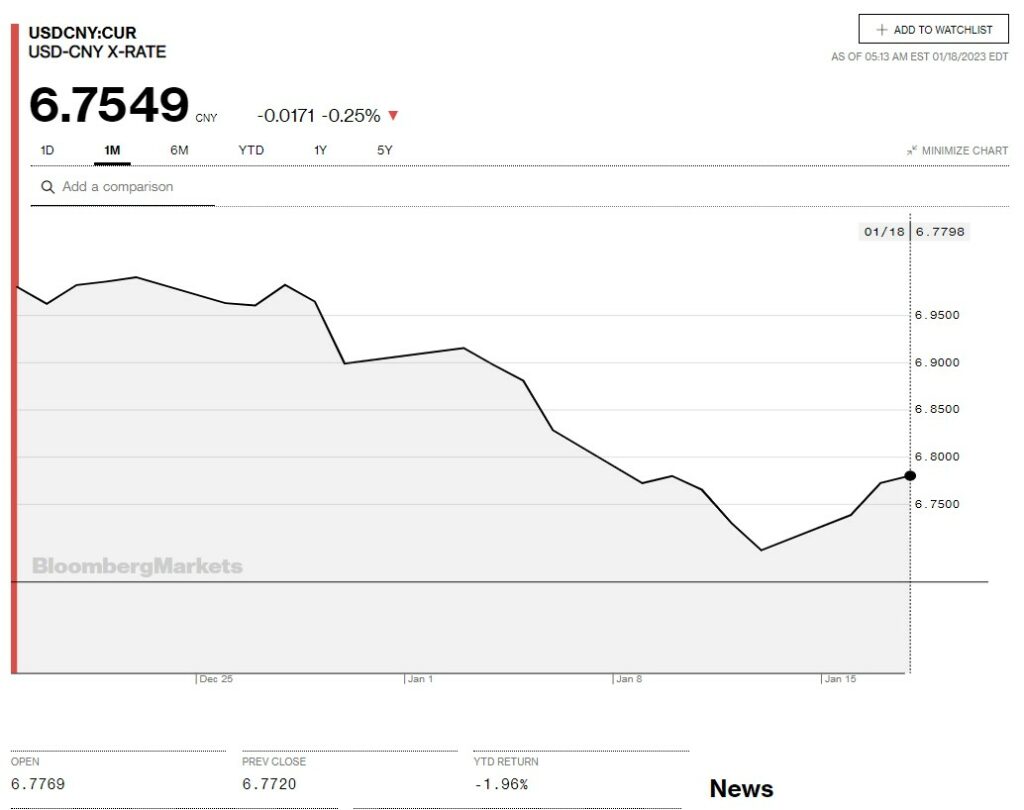

China Snapshot

Today’s Bank of China Fix: 6.7602, previous 6.7222

Shanghai Shenzhen CSI 300 fell 0.17% to 4130.32

Chart: USDCNY one month

Source: Bloomberg