Source: Pixabay/IFXA Ltd

10-year US Treasury yields drop to 1.438% ( 1.581% last Friday)

European equities rise, S&P 500 flat, WTI reclaims $70.00 handle

Brexit issues a drag on UK growth

USDCAD open 1.2099-03, Overnight range 1.2082-1.2114 Previous close 1.2096

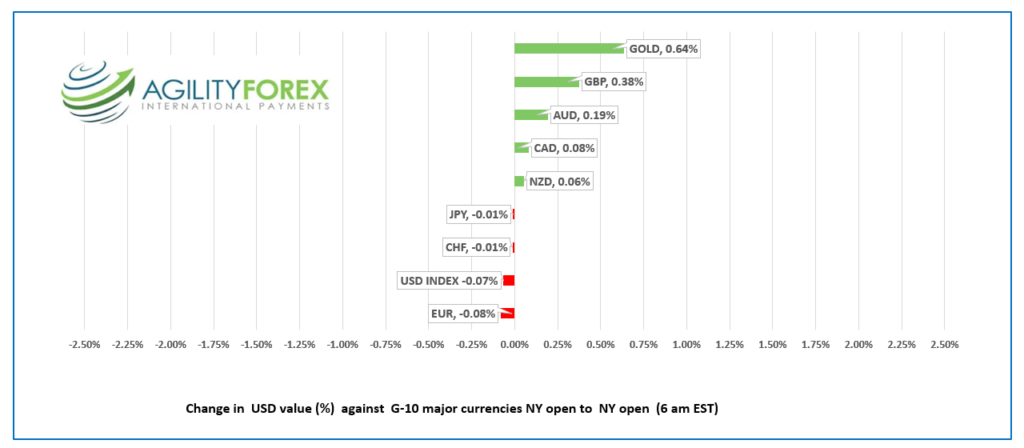

FX at a Glance

FX Recap and outlook

“Don’t fight the Fed” is a long-known financial market proverb. Unfortunately, bond bears are re-learning why the adage is true. Fed Chair Jerome Powell and most of his colleagues insisted that US inflation rates would rise, but the rise would be transitory, and the Fed would ignore price increases.

The message hit home again yesterday after US May CPI rose 5.0% y/y and Core-CPI gained 3.8% y/y.

Analysts cited a mess of price increases but attributed them to a surge in demand as pandemic restrictions eased, and therefore not sustainable Bond Traders got the message. 10-year US Treasury yields dropped from a pre CPI reading of 1.496% to an overnight low of 1.43%.

Oil price action turned violent yesterday. WTI plunged from $70.35/barrel to $68.98/b, nearly 2% in a 2 ½ hour window following a misleading headline suggesting Iran nuclear sanctions were lifted. In reality, only a few Iranian individuals had sanctions removed. Prices quickly recovered, and WTI is trading at $70.48 in NY.

WTI prices received additional support from the International Energy Agency (IEA) June Oil report. The IEA forecasts that “Global oil demand is set to return to pre-pandemic levels by the end of 2022, rising 5.4 mb/d in 2021 and a further 3.1 mb/d next year.”

EURUSD did not get any traction from the ECB meeting. Prices continue to bounce in a 1.2140-1.2190 range after the ECB left interest rates and the size of PEPP purchases unchanged. ECB policymaker Francois Villeroy said there is no need to alter policy. His colleague Klaas Knot appeared to disagree. He said there was “some upside risks slipping into the inflation outlook.” EURUSD started sliding in NY and prices are testing support at 1.2120, which if broken targets 1.2000.

GBPUSD consolidated yesterday’s post-US CPI gains in Asia, trading in a 1.4157-1.4184 range. A rash of somewhat mixed data knocked GBPUSD to 1.4140 before prices rebounded to 1.4160 in NY. Industrial and Manufacturing Production were weaker than forecast. April GDP rose 2.3% m/m, below estimates but better than the March result.

However, ongoing Brexit issues around the Irish border are a drag to gains. GBPUSD continues to bounce in the 1.4067-1.4250 range that has contained price action since May 17.

USDJPY rallied from a pre-CPI level of 109.44 to 109.78 before plunging Treasury yields drove prices to 109.33 when the session ended. Prices inched higher overnight and USDJPY is hovering around the 109.50 level. Japanese officials are planning to lift pandemic restriction in Tokyo on June 20.

AUDUSD and NZDUSD dipsy-doodled following yesterdays CPI data, then price action mirrored EURUSD moves. New Zealand PMI was 58.6 in May, compared to 58.4 in April.

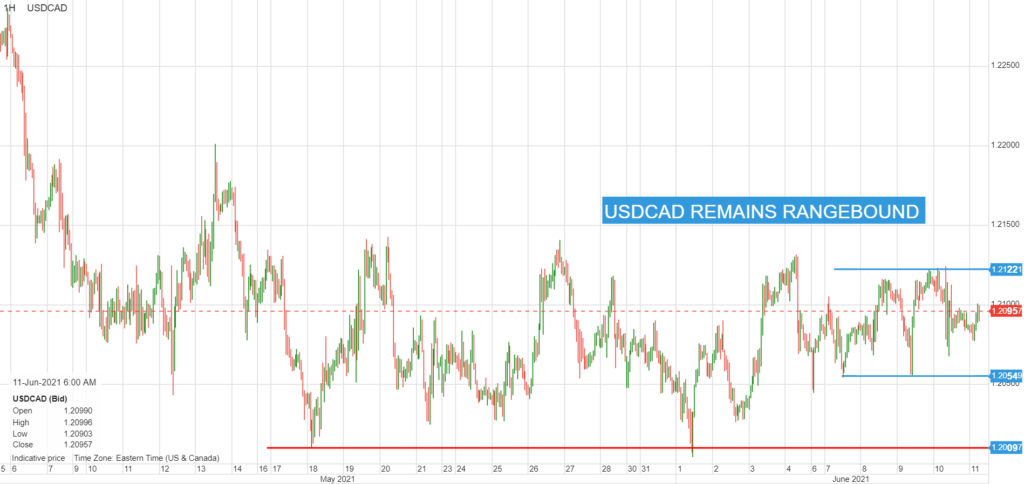

USDCAD is the currency pair that time forgot. Prices traded narrowly in a 1.2082-1.2101 range overnight after bouncing in a 1.2054-1.2122 range the entire week. Bank of Canada Deputy Governor Timothy Lane’s speech yesterday did not provide any insight Wednesday’s BoC decision. The BoC is reading from the Fed’s script saying that inflation isn’t an issue, but they have concerns with labour market challenges creating additional slack in the economy.

USDCAD price may get messy in the run-up to 10:00 am due to chunky option strikes rolling off.

The Michigan Consumer Sentiment Index (forecast 84) is the data highlight of the day.

USDCAD technical outlook

The USDCAD technicals are unchanged. Prices are trapped inside a 1.2000-1.2150 range until fresh fundamentals or data drive prices outside that band. For today, USDCAD support is at 1.2070 and 1.2040. Resistance is at 1.2120 and 1.2140 Today’s range 1.2070-1.2130

Chart USDCAD 4 hour

Source: Saxo Bank

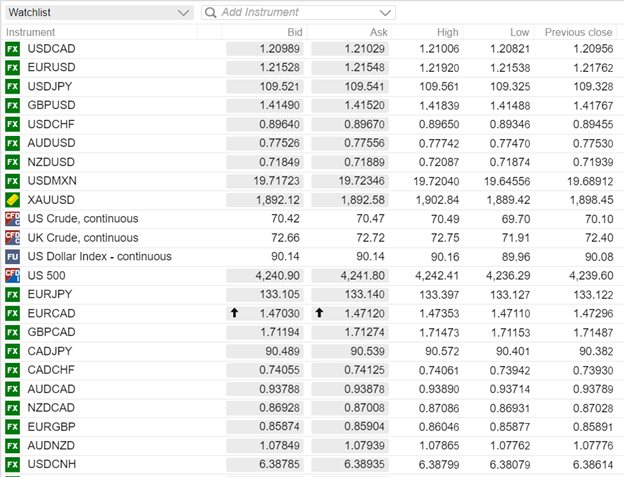

FX open, high, low, previous close

Source: Saxo Bank