Source: Adobe stock

- Russia declares “occupied” Ukraine as part of Russia-will defend the motherland

- Economic data, Bonds, and month-end flows compete for dominance

- US opens softer but poised to close September with substantial gains.

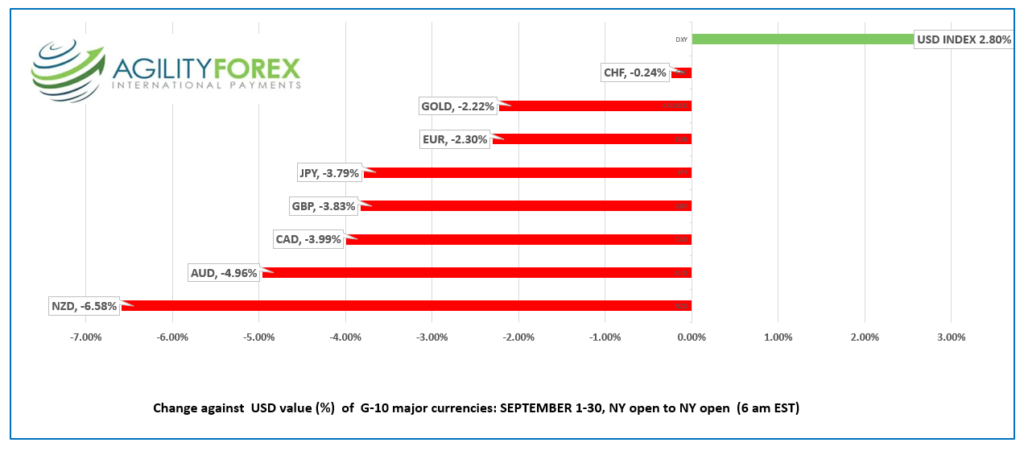

SEPTEMBER FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3693-97, overnight range 1.3660-1.3750, close 1.3685

USDCAD is the tail wagged by the FOMC dog. FX traders ignore domestic inputs, and even oil price swings (unless they are dramatic) and just focus on the prevailing US interest rate outlook and Wall street stock market direction.

For now, investors just want US dollars. USDCAD broke above the overnight high of 1.3722 to reach 1.3750 in NY when S&P 500 futures dipped to 3628.00.

WTI oil prices are in the middle of the $80.79-$82.52/barrel overnight range, supported by supply concerns from Hurricane Ian and Russian. There is talk that Opec is considering a large production cut to take effect November 1.

USDCAD trading may be subdued as Canadian banks and Federal government employees get a day off.

USDCAD Technical outlook

The intraday technicals are bullish above 1.3650, looking from a break above 1.3760 to extend gains to 1.3830. A move below 1.3650 targets 1.3605 then 1.3550.

Longer term, the USDCAD technicals are bullish but prices are consolidating recent gains in a 1.3560-1.3820 range.

For today, USDCAD support is at 1.3630 and 1.3610. Resistance is at 1.3760 and 1.3790. Today’s range: 1.3670-1.3760

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Global markets are finishing September in a state of flux.

Geopolitical tensions notched higher after Putin formally declared captured Ukraine territories as Russia and warned that attacks in those areas will be considered an act of aggression against Russia. That’s like your neighbour stealing your lawnmower then telling you he will blow up your house if try to take it back.

It’s also month-end and quarter end. Portfolio rebalancing flows may disrupt FX markets around the 11:00 am EDT fixing time.

Fed officials did their best to keep the trajectory for US interest rates at the top of the agenda. Cleveland Fed President Loretta Mester suggested that US rate may rise higher than the expected 4.6% terminal rate. She said “I probably am a little bit above that median path because I see more persistence in the inflation process. Getting above a 4% fed funds rate is important to helping to lower inflation.

The US 10-year Treasury yield had a wild ride this week, rising from 3.757% on September 26 to 4.01% on Wednesday, and is 3.70% in NY today. The retreat managed to put a floor under sliding US stock market prices.

Asia equity index closed with losses overnight and finished the month deep in negative territory. Japan’s Nikkei 225 index fell 7.67% in September while Australia’s ASX 200 dropped 7.34%. Hong Kong’s Hang Seng index plunged 13.69%.

European bourses are squeezing higher, but the monthly performance is negative. The German Dax index is 0.86% higher, but down 5.89% in September. S&P futures point to a positive open on Wall street but are down nearly 8.0% for the month.

The Fed’s preferred inflation gauge Personal Consumption Expenditure (PCE,) rose 0.3% m/m compared to 0.2% in July. The Michigan Consumer Sentiment Index (forecast unchanged at 59.5) rounds out the data dump.

EURUSD is in the middle of its overnight 0.9853 to 0.9756 range in NY. Traders are torn between buying EURUSD on elevated rate hike concerns following news inflation rose to 10.0% y/y in September and selling because of recession risks. The short term EURUSD technical picture is negative below 0.9850

GBPUSD fully recovered losses from the “mini-budget” debacle when prices reached 1.1233 overnight. Prices dropped steadily ever since and touched 1.1027 in NY. The gains were in anticipation that Prime Minister Liz Truss, and Chancellor Kwasi Kwarteng, would retract some of the tax cuts, and prices dropped when it didn’t happen. GBPUSD garnered a bit of support on news Q2 GDP rose 0.2% q/q far better than the expected drop of 0.1%.

USDJPY is trading sideways in a 144.22-144.76 band. Japanese Industrial Production, Retail Trade and Construction Orders data was better than expected. Gains were limited by softer US treasury yields and negative global risk sentiment.

AUDUSD traded in a 0.6453-0.6523 range due to broad month end US dollar demand.

The Michigan Consumer Sentiment Index is expected to remain unchanged at 59.5.

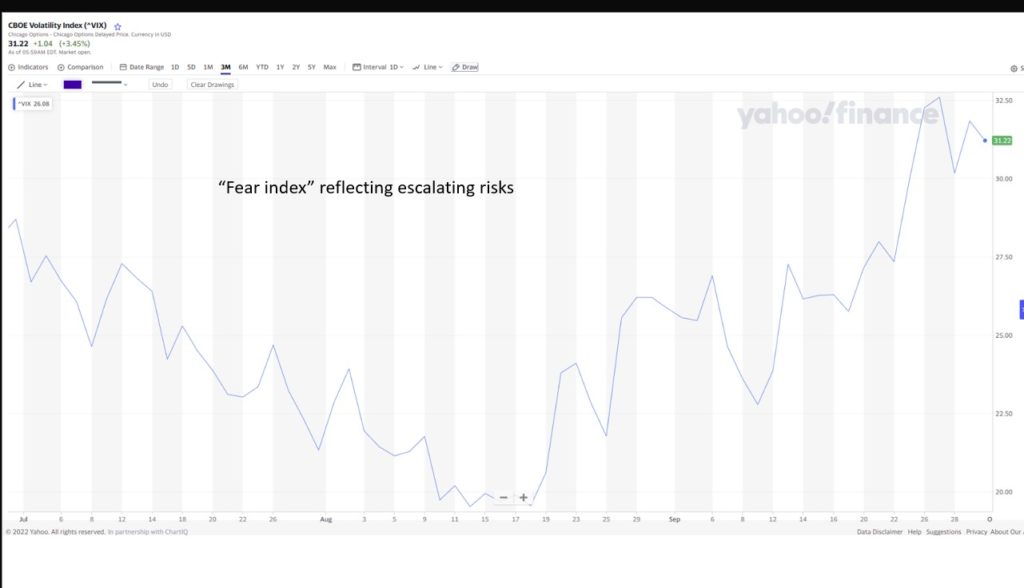

The thirty-minute, one week, US dollar index chart clearly reflects the FX volatility and indecision in markets

Chart of the Day: CBOE Volatility Index-5 days

Source: Yahoo Finance

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

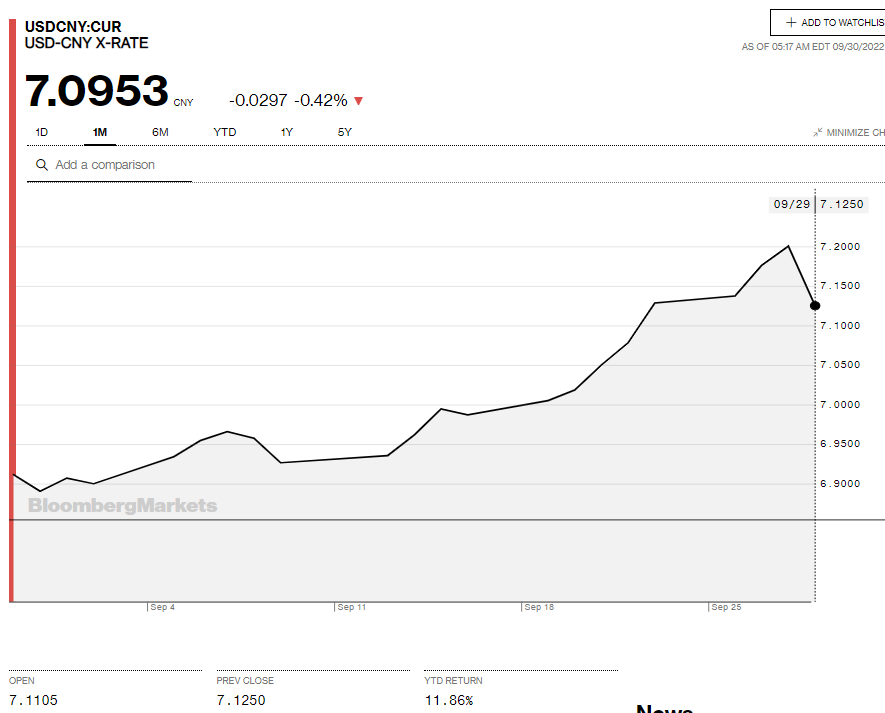

China Snapshot

Today’s Bank of China Fix: 7.0998, previous 7.1102

Shanghai Shenzhen CSI 300 fell 0.58% to 3,804.89

Caixin September Manufacturing PMI 49.1 (forecast 49.5, August 49.5)

NOTE: Chinese markets closed next week for Golden Week.

Chart: USDCNY 1 month

Source: Bloomberg