Photo:Bing Image Creator

August 29, 2023

- China considering further rate cuts.

- Equities posting gains.

- USD dollar opens mixed, but lower compared to Monday.

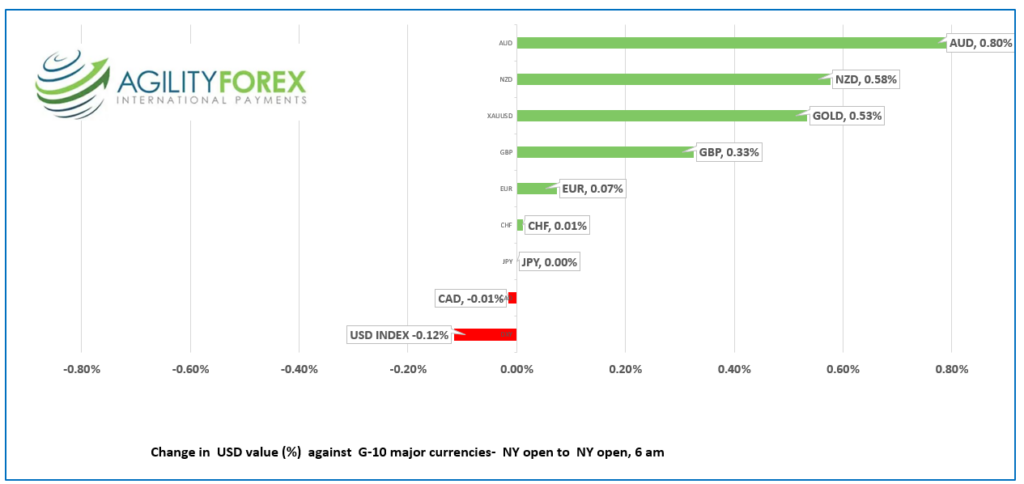

FX at a Glance

Source: IFXA/Raymond Peters

USDCAD Snapshot: open: 1.3599-03, overnight range: 1.3587-1.3638, close 1.3596

USDCAD was largely ignored overnight. Prices drifted in a narrow band and opened nearly unchanged from yesterday’s close. FX risk sentiment is rather blasé and it is reflected in USDCAD price action. This mornings USDCAD rally to 1.3638 followed on the heels of S&P 500 futures erasing overnight gains and turning negative.

USDCAD direction will be determined by how the S&P 500 reacts to this week’s US GDP, ISM and nonfarm payrolls data and the Caixin China Manufacturing PMI report.

Oil prices are stuck in a rut, with WTI trading in a $78.00-85.00/b range, which is also not doing the Canadian dollar any favours. WTI gains are capped by Chinese growth concerns while Opec production cuts limit the downside.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3550 looking for a break above 1.3660 to extend gains to 1.3690, then 1.3750. A break below 1.3550 negates the upside pressure and targets 1.3440.

Longer term, the USDCAD technicals are bullish after breaking above 1.3430, the downtrend line from March. A break above 1.3680 suggests further gains to 1.4000.

For today, USDCAD support is at 1.3580 and 1.3540. Resistance is at 1.3650 and 1.3680. Today’s range 1.3590-1.3660.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Traders are apathetic. There is not a whole lot of enthusiasm for getting involved in markets ahead of Friday’s US nonfarm payrolls report (forecast 170,000), despite a mess of economic data coming down the pipe, including JOLTS job openings, consumer confidence, and the Case-Shiller Home Price Index today.

JOLTS is expected to show that job openings in July declined to 9.465 million from 9.582 million in June, which could suggest the US economy is starting to weaken. Enthusiasm is also muted because it is the last week of summer ahead of the Labor Day weekend.

Asian equity markets followed Wall Street’s lead and closed higher, with Australia’s ASX 200 rising 0.71%. European bourses are in the green, with a 1.62% jump in the UK FTSE 100 leading the pack higher. S&P 500 futures gave up earlier gains and are modestly negative (down 0.10%). The US 10-year yield is at 4.23%.

EURUSD is at the bottom of its 1.0786-1.0839 range in NY, due to uncertainty ahead of next month’s ECB monetary policy meeting and a poor Consumer Sentiment report from Germany. GfK is forecasting -25.5 points in consumer sentiment for September, down 0.9 points from August of this year.

GBPUSD followed EURUSD lower in a 1.2563 to 1.2636 range with the low occurring in NY. Support from hopes that the BoE hikes rates by 25 bps even if the Fed leaves rates unchanged has faded and GBPUSD is drifting with shifts in risk sentiment.

USDJPY traded quietly in a 146.31-146.62 range then popped to 147.22 in NY trading with prices underpinned by the small rise in the US 10-year yield to 4.23% from 4.20% at yesterdays close. Economists made a bit of a fuss after Japan’s July unemployment rate unexpectedly rose above expectations to 2.7% (forecast and previous 2.5%). Toyota had a computer problem which forced the shutdown of all its auto plants in Japan.

AUDUSD traded in a 0.6423-0.6456 range overnight then dropped to 0.6401 in NY. The boost from talk of additional Chinese stimulus before year-end has given way to fears of higher US interest rates. Australian CPI is due Wednesday and is expected to dip to 5.2% from 5.4%

Top of Form

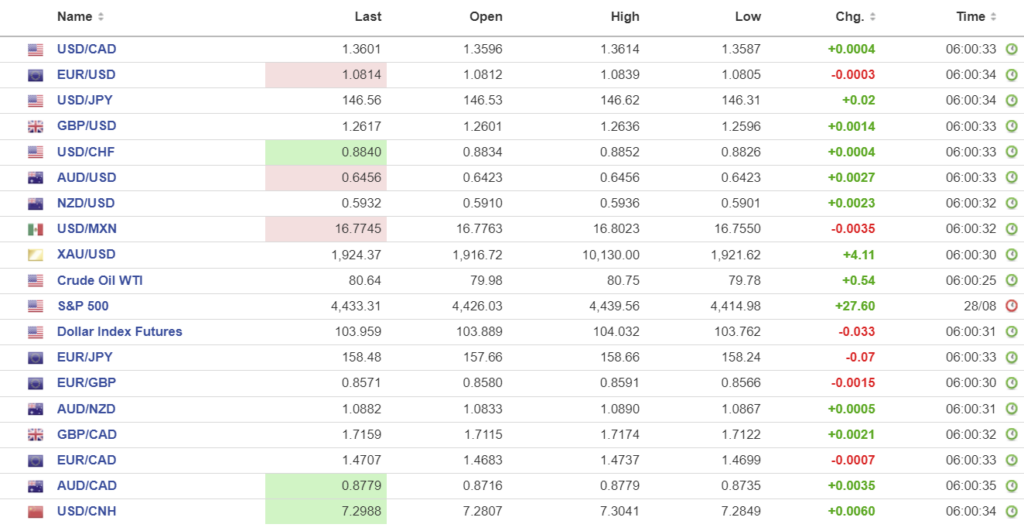

FX high, low, open

Source: Investing.com

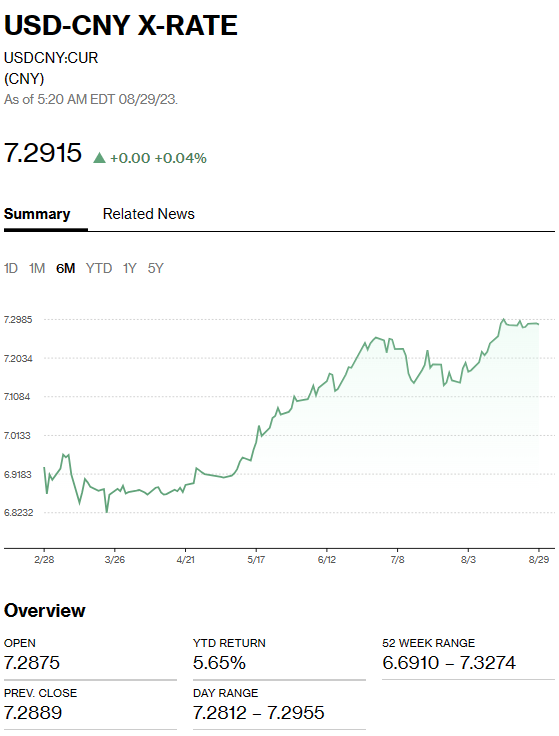

China Snapshot

Bank of China Fix: today 7.1851 previous 7.1856.

Shanghai Shenzhen CSI 300 rose 1.00% to 3790.11.

China State media reporting that the PboC may cut Reserve Requirement Rations before year end,

Chart: USDCNY 1 month

Source: Bloomberg