Photo: HDClipartAll.com

January 11, 2023

- Markets tepid while awaiting Thursday’s US CPI data

- Risk sentiment mildly positive after Powell avoids commenting on economy

- US dollar opens mixed-AUD outperforms

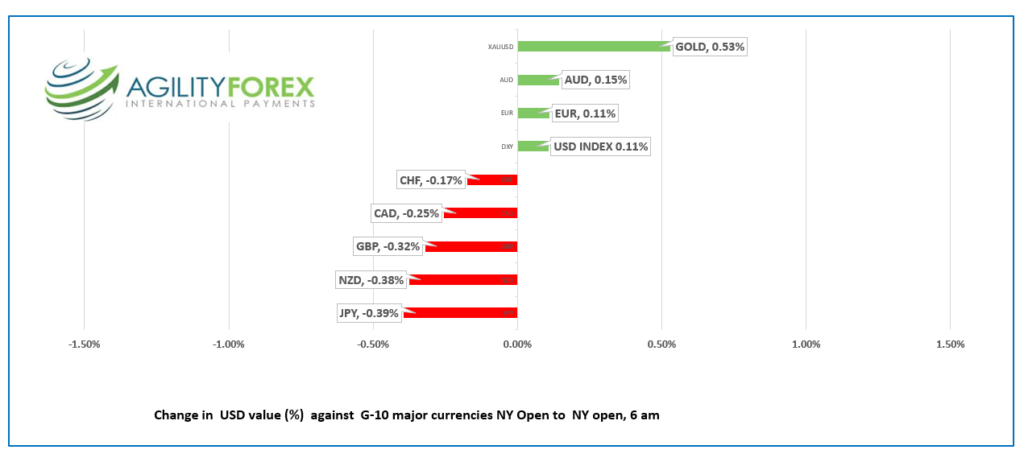

FX at a glance

Source: IFXA Ltd/RP

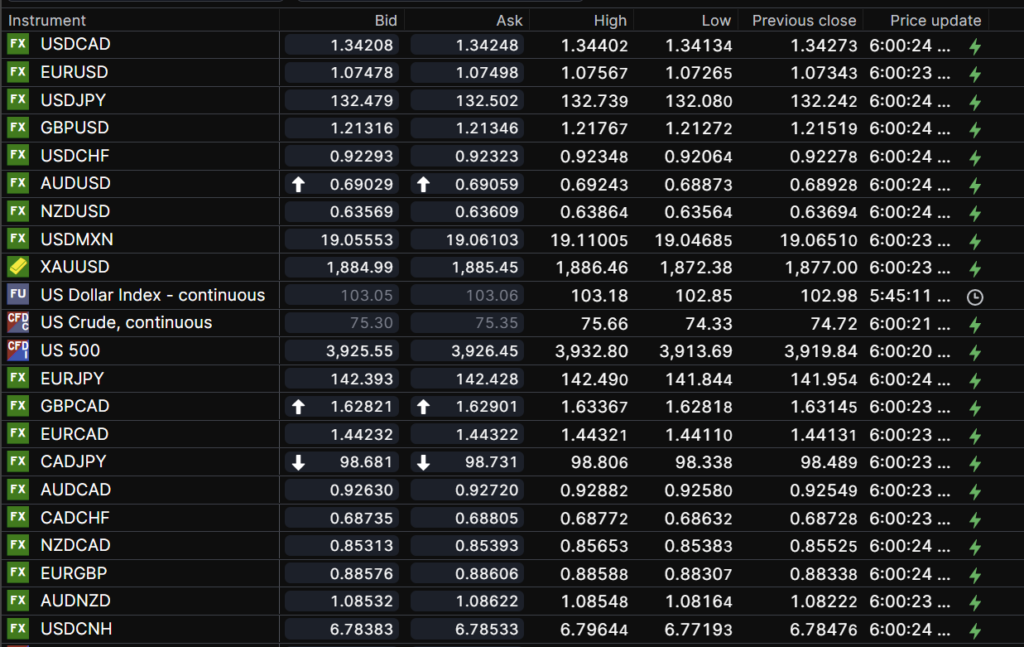

USDCAD Snapshot: open 1.3421-25, overnight range 1.3413-1.3444, close 1.3427

USDCAD is directionless, although still basking in the residual glow from Friday’s strong employment data. That result suggests the Bank of Canada will hike rates by 25 bps on January 25 and leave the door open for another rate hike in March.

USDCAD is not getting much support from WTI oil prices, which have fallen from $81.45 at the beginning of the year to $75.37/b today. Traders are hoping that Russian sanctions, China’s reopening, and Opec production cuts would fuel a rally towards $100.00/b. However, concern around Thursday’s US CPI data and the American Petroleum Institute reporting crude inventories rose 14.9 million barrels last week, has limited gains.

There are no Canadian economic reports today.

USDCAD technical outlook.

The USDCAD technical outlook is neutral inside the current 1.3340-1.3450 range. The intraday technicals are mildly bullish while prices are above 1.3405, looking for a break above 1.3450 to extend gains to 1.3520. A break below 1.3405 targets 1.3340, which if broken, opens the door to further losses to 1.3220.

For today, USDCAD support is at 1.3405 and 1.3370. Resistance is at 1.3450 and 1.3490

Today’s range 1.3390-1.3490

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Global markets are twiddling their thumbs and waiting for Thursday’s key US inflation report.

Friday’s lower average hourly earnings data and a weak ISM Services PMI report sparked chatter that the Fed will need to cut rates in 2023 despite FOMC statements to the contrary. If JP Morgan analysts are correct, the market view will trump the Fed outlook.

JPM analysts predicted CPI will spark a “big move in either direction.” They said the consensus estimate is that headline inflation will be 6.5% y/y and Core-inflation at 5.7% y/y. They predicted that if the results are at consensus (probability of 65%) the S&P 500 will soar 1.5-2.0%.

If CPI is lower than expected (20% probability) the S&P 500 would rally 3-3.5%.

If CPI is higher than consensus, (15% probability), the S&P 500 would fall 2.5-3.0%.

Fed chair Jerome Powell disappointed markets yesterday when he failed to discuss the US economic outlook. Instead, he took a shot at “woke” policymakers, saying the Fed must avoid straying into political issues specifically “We are not, and will not be, a ‘climate policy maker.’” Brrrr-humbug!

Asian equity indexes followed Wall Street’s lead and closed with gains. Japan’s Nikkei 225 index rose 1.03 % while Australia’s ASX 200 gained 0.90%. European bourses opened in positive territory then extended gains. The German Dax index is up 0.80% while the UK FTSE 100 index is 0.63% higher (as of 6:30 am). S&P 500 futures have risen 0.19% and the US 10-year Treasury yield ticked down to 3.574% from 3.611% yesterday. Gold and oil prices are modestly higher.

EURUSD is near the top of its 1.0727-1.0757 overnight range. Prices are supported by hawkish ECB-speak. Bank of France Governor Francois Villeroy said “In 2023, new interest rate hikes will very likely be needed in the coming months at a pragmatic pace in order to bring inflation towards 2%.” His colleague, Austrian Central Bank Governor Robert Holzmann agrees and said it was too early to discuss a terminal rate. EURUSD has support at 1.0680 and resistance 1.0710.

GBPUSD is trading with a modestly negative bias in a 1.2119-1.2177 range. GBPUSD is underpinned by the modestly positive global risk sentiment due to hopes the Fed’s hiking cycle ends in Q1. Traders are looking past weak domestic data and hoping that a break above 1.2210 extends GBPUSD gains to 1.2480.

USDJPY is trading sideways in a 132.08-132.74 range with prices tracking see-saw US 10-year Treasury yield moves. The US and Japan are shoring up defences in the Okinawa Islands, as a buffer towards Chinese aggression towards Taiwan. That buffer includes significant increase in anti-ship missile capabilities.

AUDUSD traded in a 0.6887-0.6924 range, supported by hot inflation number and higher than expected retail sales. November CPI rose 7.3% y/y (forecast 7.3%, previous 0.9%). Bad weather inflating food costs and high energy prices were to blame. Retail Sales rose 1.4% m/m in November compared to forecasts for a 0.6% increase.

The US data calendar is empty.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

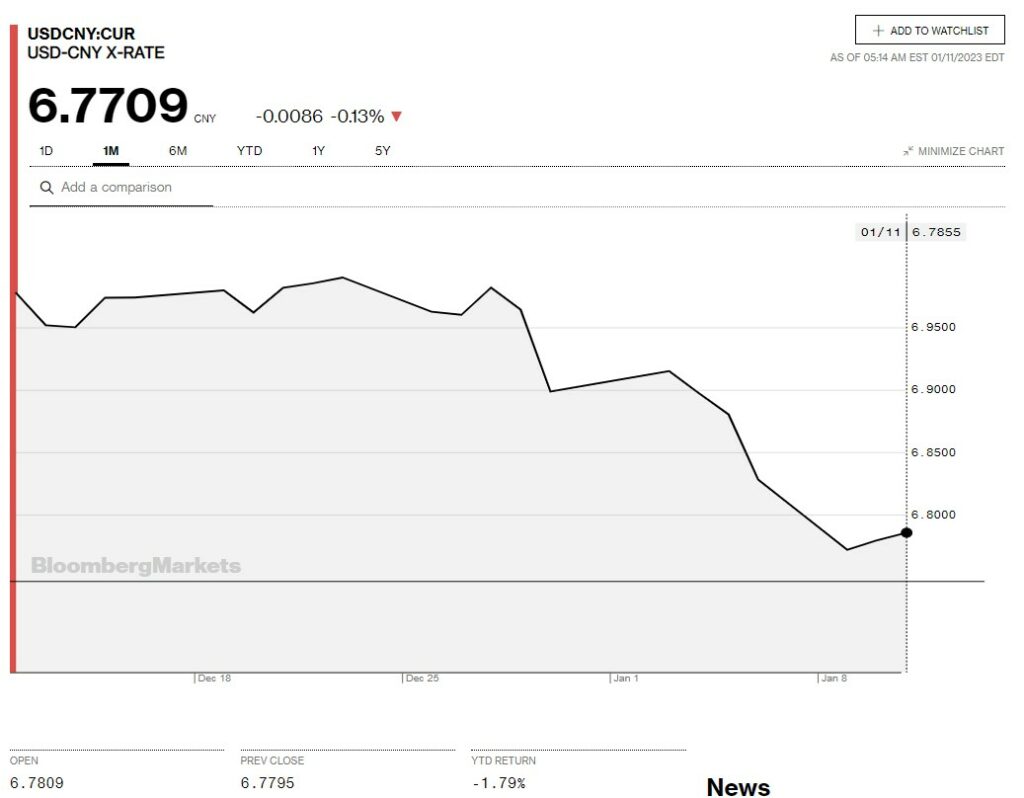

China Snapshot

Today’s Bank of China Fix: 6.7756, previous 6.7611

Shanghai Shenzhen CSI 300 fell 0.19% to 4010.03

Chart: USDCNY one month

Source: Bloomberg