Photo: publicdomainvectors.org

- FOMC statement and SEP at 2:00 pm ET/Powell press conference at 2:30 pm ET

- Analysts debate slower pace of US rate hikes, but higher terminal rate

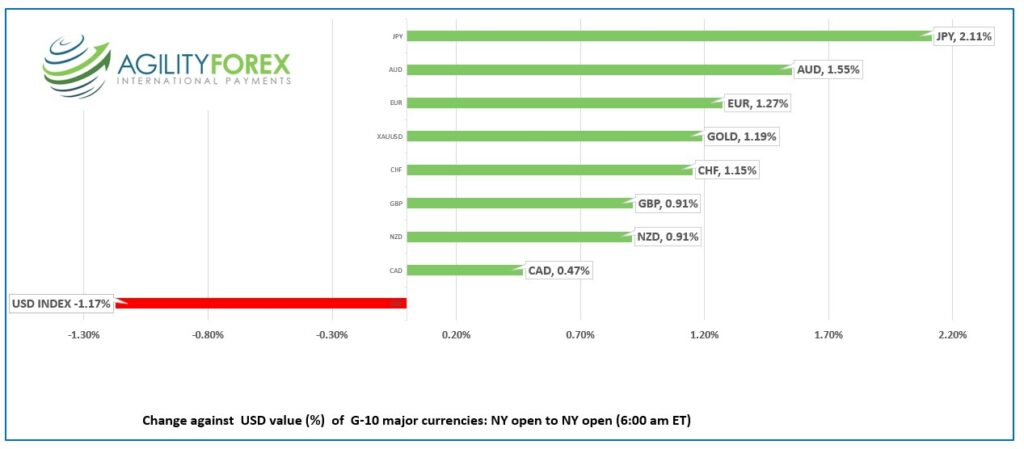

- US dollar consolidates yesterday’s losses-JPY gains 2.11%

FX at a glance:

Source: IFXA Ltd/RP

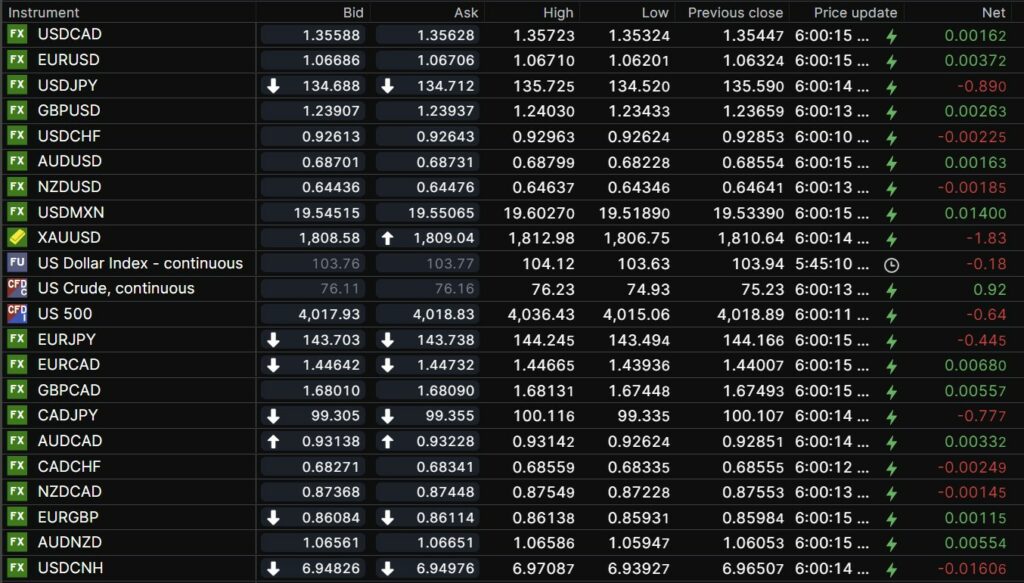

USDCAD Snapshot: open 1.3559-63, overnight range 1.3532-1.3572, close 1.3545

USDCAD dropped to 1.3524 from 1.3622 yesterday then consolidated the gains overnight.

USDCAD has not seen much benefit from the 8.0% jump in WTI prices this week. Traders ignored the API report of a 7.81-million-barrel increase in US crude inventories, preferring the Opec and IEA forecast for a modest increase in demand in 2023, compared to their previous guesses.

The FOMC statement, Summary of Economic Projections (SEP), and Powell’s press conference are key to USDCAD direction with risk sentiment measured by S&P 500 price action.

Canada Manufacturing Sales (forecast 2.0%, previous 0) are due but not a factor for traders.

USDCAD technical outlook.

The intraday USDCAD technicals are bearish below 1.3580, looking for a break below 1.3510 to extend losses to 1.3390. A break above 1.3580 targets 1.3650. However, on this important FOMC day, the intraday technicals are useless.

The weekly chart tells a different story. Fibonacci retracement analysis of the 1.2020-1.4650 covid-range suggests the retracement from the low completed in October at 1.3970. The failure to remain above the 61.8% retracement level at the 1.3640-50 area suggests further losses to 1.2760, the uptrend line from May 2021.

For today, USDCAD support is at 1.3510 and 1.3470. Resistance is at 1.3580 and 1.3640

Today’s range 1.3520-1.3620.

Chart: USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

Yesterday’s cooler than expected US November inflation report (CPI ex food/energy 6.0% y/y vs Oct. 6.3% and 0.2% m/m vs Oct 0.3% m/m) knocked the US dollar head over heels. The price swings were greatly exaggerated by thin markets as many participants were waiting for the outcome of todays FOMC meeting or have closed their books for 2022.

Pundits described the CPI report as subdued which is a tad misleading. Inflation may have dipped a few ticks from October, but Powell’s favourite measure (Core CPI) is still three times higher than the Fed’s 2.0% target. Furthermore, food and services prices continued to climb, so ya, prices are subdued if you skip eating,

Some analysts suggested yesterday’s data could lead to a 25 bp rate hike today, rather than the 50 bps that is expected. Psshaw! Mr Powell is likely to push back against suggestions inflation has peaked and US rates are close to the terminal level.

S&P 500 futures soared from 4009 to 4140 in the wake of the CPI report, but all the gains had evaporated by noon hour. Futures are sitting at the bottom of the narrow 4010.57-4036.43 overnight range.

Asian equity indexes closed with gains across the board. Japan’s Nikkei 225 index climbed 0.72% while Australia’s ASX 200 gained 0.67%.

European bourses did not follow Asia’s lead mainly due to caution ahead of four central bank meetings in the region (Norges Bank, Swiss National Bank, Bank of England, and ECB) on Thursday. The German Dax is down 0.76% while the UK FTSE 100 is down 0.36%.

The US 10-year Treasury yield dropped from 3.607% to 3.421% in the aftermath of the inflation data then closed at 3.505%. Prices were little changed overnight.

Gold (XAUSD) rose from $1782.48 to $1823.80; post CPI then consolidated the gains in a $1806.75-$1812/98 range overnight.

EURUSD is consolidating yesterday’s gains in a quiet session. The single currency spiked to 1.0673 from 1.0529 Tuesday, then opened at the top of its overnight 1.0620-1.0670 range in NY. Eurozone Industrial Production fell 2.0% in November (forecast -1.5%). The EURUSD technicals are bullish above 1.0570 looking for a test of 1.0780.

GBPUSD rallied from 1.2250 to 1.2443 yesterday then consolidated the gains in a 1.2343-1.2403 range overnight. UK inflation was lower than expected, dropping 10.7% y/y from 11.1% in October. The news ensures the BoE will hike rates by 50 bps tomorrow.

USDJPY plunged from 137.96 yesterday to 1.3452 overnight and is sitting at 134.90 in early NY trading. The steep drop in US Treasury yields and talk that the BoJ will review the need for its dovish monetary policy in 2023 is weighing on prices. The Tankan survey showed business sentiment was weakening.

AUDUSD traded in a 0.6823-0.6880 range on the back of the US dollar weakness and NZDUSD bounced in a 0.6435-0.6464 range. NZD underperformed against AUD after the New Zealand Treasury predicted a recession starting in Q2.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

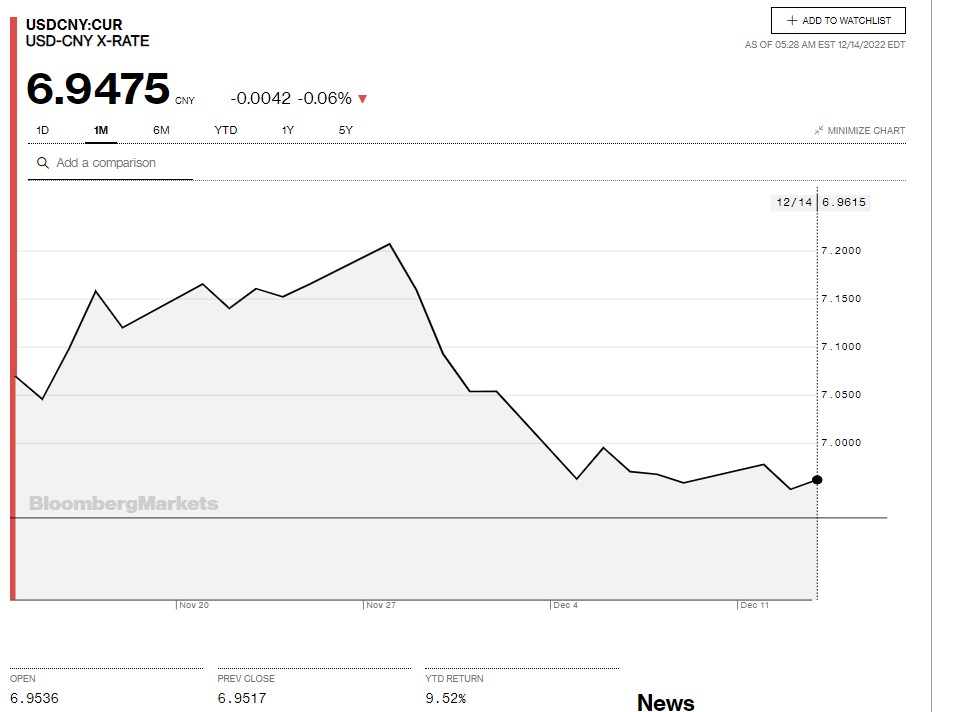

China Snapshot

Today’s Bank of China Fix: 6.9535, previous 6.9746

Shanghai Shenzhen CSI 300 rose 0.23%% to 3954.89

Chart: USDCNY 1 month

Source: Bloomberg