December 10, 2024

- Greenback firms in quiet trading ahead of Wednesday CPI.

- RBA leaves rates unchanged-as expected.

- US dollar grinds out gains-AUD underperforms.

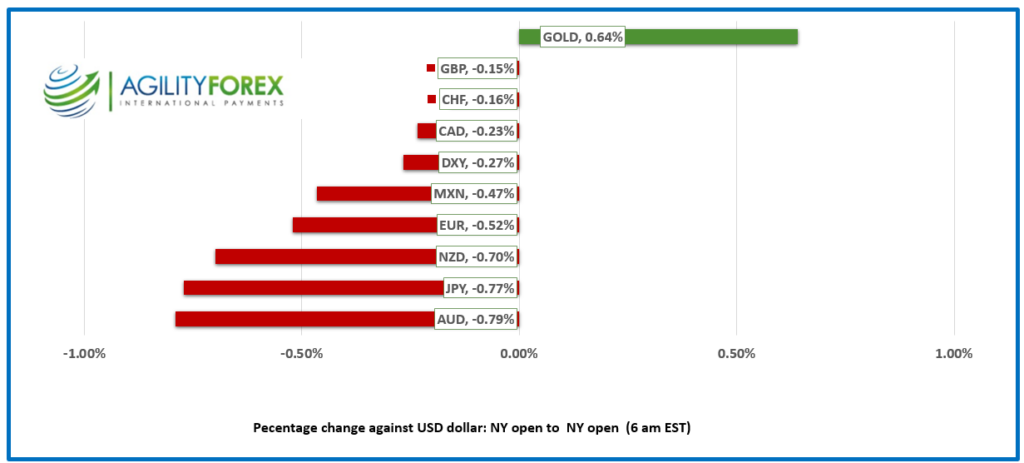

FX at a Glance

Source: IFXA/RP

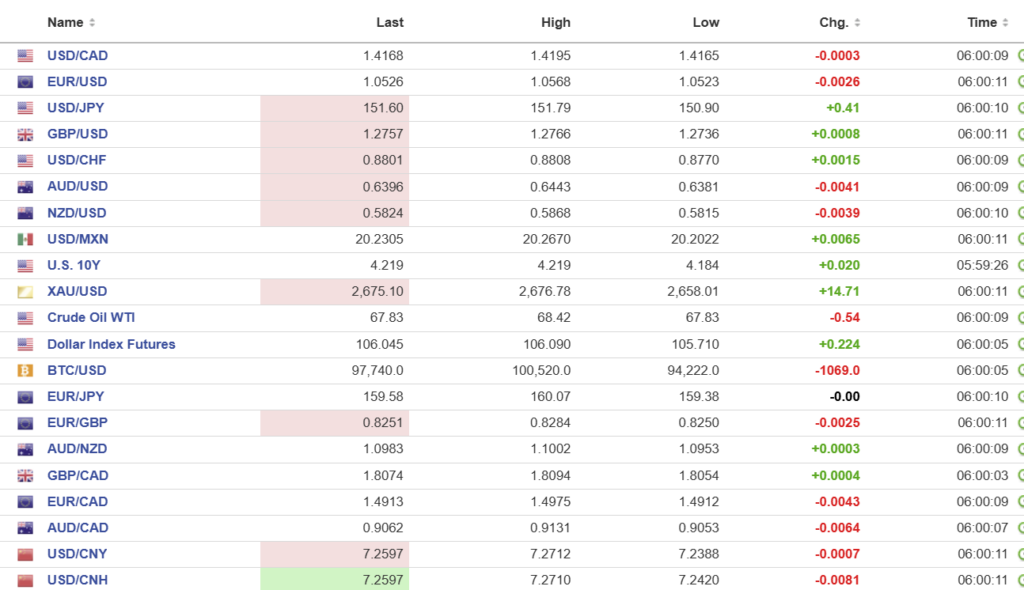

USDCAD open 1.4168, overnight range,1.4165-1.4195, close 1.4172

USDCAD retreated yesterday but the drop was short-lived and USDCAD recouped all of the days losses by the close.

President Trump (he is-its just not official yet) boasted about the effectiveness of his tariff threats, bragging about how Canada’s Justin Trudeau “flew to Mar-a-Lago within about 15 seconds after the call ended.” Later Trump tweeted. “It was a pleasure to have dinner the other night with Governor Justin Trudeau of the Great State of Canada. I look forward to seeing the Governor again soon so that we may continue our in-depth talks on Tariffs and Trade, the results of which will be truly spectacular for all! DJT.”

It’s hard to believe that Canada will be able successfully negotiate when Trump thinks Trudeau is a muppet.

USDCAD is buoyed by expectations that the Bank of Canada will deliver a 50-basis-point rate cut on Wednesday—a move that seems almost inevitable. Governor Tiff Macklem effectively cornered himself by declaring inflation defeated and dismissing any price increases as mere blips. This stance, combined with a weak employment report and sluggish economic growth, leaves little room for the Bank to hold back on a significant rate cut.

There is no US or Canadian economic data of note today.

USDCAD Technicals

The intraday technicals are bullish. The break above resistance at 1.4100 on Friday, reverted to support and that contained yesterday’s downside move. However, the rally has stalled at 1.4195 which suggests further 1.4100-1.4200 range trading is likely until Wednesday’s US CPI release and the Bank of Canada meeting.

The uptrend channel from the beginning of December is intact while prices are above 1.4050 with the top of the band in the 1.4250 area.

For today, USDCAD support is 1.4130 and 1.4100. Resistance is 1.4200 and 1.4250.

Today’s Range: 1.4120-1.4220.

Chart: USDCAD daily

Source: Oanda.com

China Blowing Hot-Air to Boost Economy

Chinese politicians are forever yammering on about plans, initiatives, schemes, proposals, etc., and are never at a loss for words to describe how these actions will fuel widespread economic gains. The latest rhetoric includes claims that the government’s focus is shifting to cultivate “new quality productive forces,” while remaining oblivious to the negative impact of locking up business leaders. President Xi Jinping chimed in, asserting that there would be no winner in a tariff or tech war between China and the US. Except there will be—and it won’t be China.

Equity Rally Pauses

Asian equity indexes closed mixed, with Australia’s ASX 200 losing 0.36%, while Japan’s Topix rose 0.25%. European bourses are down modestly, except for the German Dax, which is flat. S&P 500 futures are also flat. Gold (XAUUSD) is trading at 2672.49, and the US 10-year Treasury yield is 4.23%. The US dollar index (DXY) has climbed to 106.09 from 105.71.

EURUSD

EURUSD drifted lower in a 1.0523-1.0568 range ahead of what most expect will be a 25 bp rate cut by the ECB on Thursday. Some analysts warn of dovish forward guidance due to poor Eurozone economic performance. The currency pair is also weighed down by contrasting ECB and Fed monetary policy outlooks. USDCHF is underpinned by expectations for the SNB to cut rates by 25 bps on December 12.

GBPUSD

GBPUSD is doing a slow dance in a 1.2738-1.2766 range. Traders are sidelined due to a lack of economic data and other catalysts. GBPUSD is also underpinned by EURGBP selling ahead of Thursday’s ECB meeting.

USDJPY

USDJPY traded with a bullish bias, rising from 150.90 to 151.79 due to diminishing odds of a BoJ rate hike this month. In addition, the 10-year US Treasury yield ticked higher, rising to 4.23% from 4.18%.

AUDUSD and NZDUSD

AUDUSD dropped from 0.6443 to 0.6381 after the RBA left rates unchanged at 4.35%, which was widely expected. It has not recovered yet. Governor Michelle Bulloch cited sticky inflation for the decision, but the guidance was dovish, opening the door to a rate cut in early 2025.

NZDUSD is near the bottom of its 0.5815-0.5868 range due to the belief that the RBNZ will adopt a more aggressive easing strategy and weak Chinese trade data.

USDMXN

USDMXN is trading sideways in a 20.1775-20.2670 range after prices rebounded from yesterday’s post-Mexican CPI low. Headline and core CPI rose less than expected in November, and the year-over-year results were lower (4.55% y/y vs. previous 4.76% y/y) as well. Analysts do not believe that the inflation dip was enough to encourage Banxico to cut interest rates, especially in the face of Trump’s tariff threats. Mexican consumer confidence slipped to 47.4 from 48.9 in October.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC Fix: 7.1876 vs exp. 7.2806 (prev. 7.1870)

Shanghai Shenzhen CSI 300 rose 0.73% to 3995.64

China November trade surplus widens to $97.44b from $95.27 billion. Exports rise 6.7% (forecast 8.5% y/y) while imports fell 3.9% y/y (forecast 0.3%).

China said it would impose visa restrictions on US officials in retaliation for the US slapping restrictions on Chinese officials for implementing the National Security Law in Hong Kong.

SCMP reports: “China’s infrastructure spending may surge in 2025 to meet 5-year goals”

Chart: USDCNY and USDCNH

Source: Investing.com