Image by DALL-E

December 5, 2023

- Wall Street weighed down by profit-taking.

- Traders looking for ISM Services and Jolts data for direction.

- US dollar extends yesterday’s gains-AUD underperforms.

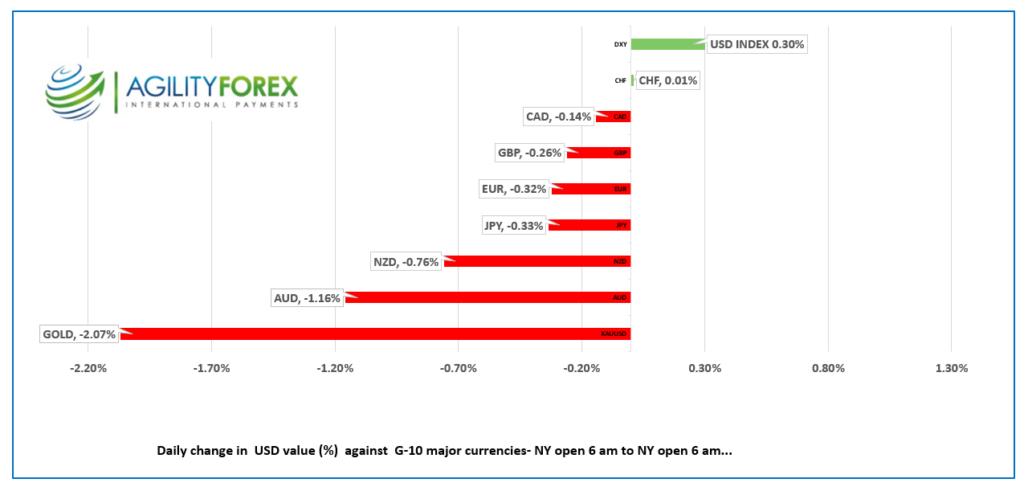

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3561-65, overnight range 1.3531-1.3592, close 1.3538

USDCAD is squeezing higher, somewhat reluctantly on the back of broad-based US dollar demand. There is not specific reason for the rally, but the sell-off on Wall Street is underpinning the greenback.

Wednesday’s Bank of Canada monetary policy meeting (a statement only affair) may be a non-event, mainly because Governor Tiff Macklem may be reluctant to raise or cut rates without having a press conference to explain the decision. The speech by Deputy Governor Toni Gravelle on Thursday may provide some insight.

Opec is not seeing the love after announcing additional production cuts with WTI trading at $72.95/b this morning, after dropping from $79.45 on November 30. Analysts are suggesting that the price drop is due to weaker demand and increased supply, from outside the cartel, including from the US, and Canada. US production has set records for two consecutive months.

The Canadian data calendar is empty.

USDCAD Technicals:

The intraday USDCAD technicals (1 -hour chart) are modestly bullish while prices are trading above 1.3550 and looking for a break above 1.3610 to extend gains to the 1.3660 area. A move below 1.3550 suggests further losses to 1.3470.

Longer term, the November USDCAD downtrend line comes into play at 1.3720 which is guiding prices lower towards the August line at 1.3470.

For today, USDCAD support at 1.3540 and 1.3490. Resistance is at 1.3610 and 1.3650. Today’s range 1.3560-1.3640

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Wall Street bulls have enjoyed a hugely profitable 2023, with November’s rally being the icing on the cake. It also helps to explain why the major equity indexes have retreated in the first couple of days of December. The final month of the year is known for exaggerated volatility and poor liquidity. It’s time to load the wheelbarrow and head to the bank.

The US dollar squeezed out some gains since yesterday’s opening. Fed Chair Jerome Powell’s comments have encouraged some profit-taking, even though traders aren’t really buying what he is selling. It is an election year after all, and the Fed is usually loath to change monetary policy to avoid being accused of favoring a particular party.

The US JOLTS job openings data for October and November ISM Services PMI (forecast 52 vs previous 51.8) will be catalysts for today’s price action.

Asian equity indexes followed the Wall Street lead and closed with losses. Japan’s Nikkei 225 index shed 1.37%, while the Australian ASX index lost 0.89%. European bourses are faring much better, led by a 0.16% rise in the German Dax after ECB member Isabel Schnabel suggested that further rate hikes are not likely. S&P 500 futures traders appear to still be in “take-profit” mode and the futures are down 0.44% (as of 6:00 am ET).

EURUSD traded uneventfully in a 1.0804-1.0848 range as traders largely ignored the latest HCOB Composite and Services PMI data. The statement said that both indexes “recorded sub 50.0 readings for the sixth consecutive month, signaling another month-on-month reduction in private sector output levels across the eurozone. While the latest reading of 47.6 was up from October’s 35-month low of 46.5 and the highest since July, it was still indicative of a solid deterioration in economic conditions.” ECB policymaker Isabel Schnabel said that additional interest rate hikes are not likely.

GBPUSD traded sideways in a 1.2607-1.2640 range with support from BRC Like-for-Like Retail Sales (actual 2.6% vs forecast 2.5%) and S&P Global Services PMI (actual 50.9 vs 50.5) underpinning prices. However, GBPUSD is seeing a bit of negative pressure due to demand for EURGBP as short-term technicals suggest the cross is oversold.

USDJPY traded in a 146.68-147.38 range amidst safe-haven demand for yen, falling inflation, and soft US Treasury yields. The Moody’s downgrade of China may have unnerved a few traders in Asia while the drop in headline Tokyo inflation to 2.3% from 2.7% in October provided some support.

AUDUSD traded negatively in a 0.6569-0.6627 range after the RBA left rates unchanged as expected but issued a somewhat dovish statement rather than the hawkish one that was expected. Traders dismissed warnings of “significant uncertainties around the outlook” and focused on the line that read “The monthly CPI indicator for October suggested that inflation is continuing to moderate, driven by the goods sector.

Chart of the Day-Oil (WTI hourly. Opec increased production cuts but traders did not care.

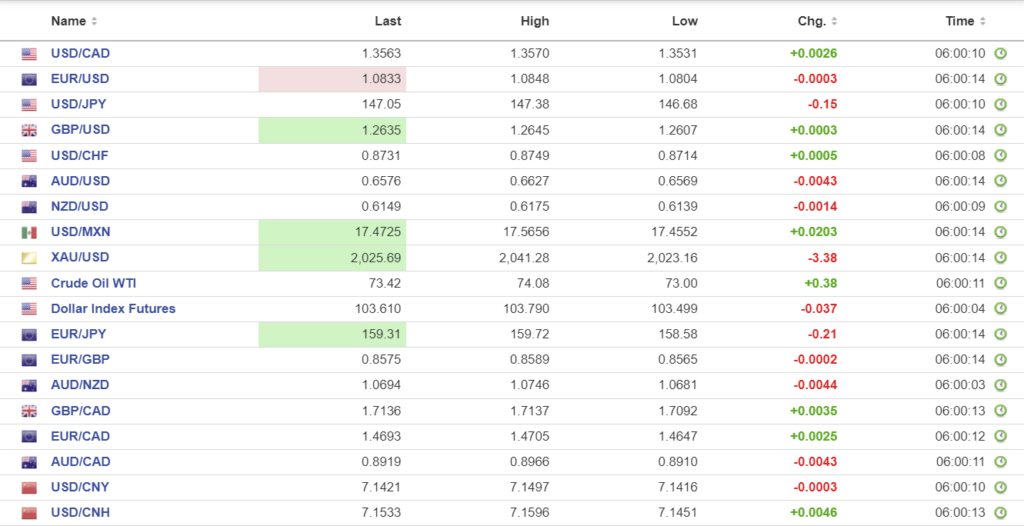

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1127, expected 7.1476, previous 7.1011.

Shanghai Shenzhen CSI 300 fell 1.90 % to 3394.26.

Caixin Services PMI rose to 51.5 from 50.4 in October.

Stock market traders were not happy after Moody’s downgraded China’s A1 rating from stable to negative. They wrote: “Moody’s expects that China’s annual GDP growth will be 4.0% in 2024 and 2025, and average 3.8% from 2026 to 2030, with structural factors including weaker demographics driving a decline in potential growth to around 3.5% by 2030.” As yet, Beijing has not issued an arrest warrant for the analyst.

Chart: USDCNY and USDCNH

Source: Bloomberg