June 17, 2024

- French politics leave Euro on defensive.

- Monetary Policy meetings for RBA, BoE, SNB, and Norges Bank this week.

- US dollar opens higher from close, mixed from Friday open.

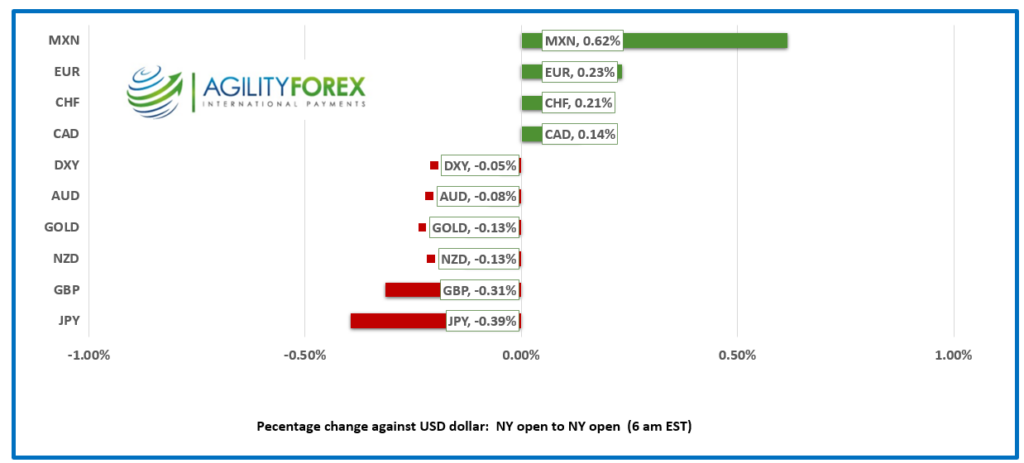

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3742, overnight range 1.3729-1.3752, close 1.3738

USDCAD traded sideways and uneventfully overnight. It will remain at the mercy of broad US dollar sentiment this week due to a dearth of domestic economic data.

There is not a whole lot of anything to support USDCAD weakness. The economy is sluggish and underperforming that of the US. Job market gains cannot keep pace with new immigrants, most of which find their way to Toronto. (Toronto’s unemployment rate exceeds that of the Province of Quebec, largely because Quebec bussed its illegal immigrants to Toronto). The BoC and Fed are on divergent interest rate paths. The Federal government budget is a mess and oil prices are sluggish. But that is not news, which is why USDCAD long positions have surged and that suggests USDCAD gains will be sluggish.

USDCAD trading should be sticky around the 10:00 am option expiry window as 2.365 billion of strikes in the 1.3750-1.3780 area mature.

WTI oil prices are steady in a 77.58-78.45 band range with potential supply increases offsetting concerns of increased demand. Downbeat Chinese Industrial Production data may limit gains.

Canada Manufacturing Sales and Wholesale sales data are on tap as is the Michigan Consumer Sentiment Index.

Canadian Housing Starts and the NY Empire State Manufacturing Index are on tap.

USDCAD Technicals

The intraday technical are bullish above 1.3730, looking for a break above 1.3760 to extend gains to 1.3810. A move below 1.3730 targets 1.3710.

Longer term, USDCAD is in an uptrend channel between 1.3700 and 1.3850 on a daily chart with neutral Bollinger Bands and RSI levels.s

For Today, USDCAD support is at 1.3710 and 1.3680. Resistance is at 1.3760 and 1.3790. Today’s Range 1.3690-1.3770.

Chart: USDCAD daily

Source: DailyFX

Bond Traders (Sharks) vs FX Markets and FOMC (Jets)

If this was a remake of West Side Story, US bond traders would be the Sharks and the FOMC would be the Jets. Bond traders looked at the FOMC dot-plot projections and call Bulls**T, then knocked the US 10-year Treasury yield from 4.426% pre-FOMC to 4.238% today. They do not believe the dot-plots projecting just one rate cut in 2024 are close to reality. Fed officials disagree. Outgoing Cleveland Fed President Loretta Mester said her view agrees with the median dot-plot while Minneapolis Fed President Neel Kashkari wants to see more evidence of slowing inflation. FX traders have sided with the Fed and the US dollar index (DXY) rallied from 103.96 pre-FOMC to 105.19 today. Can you hear the fingers snapping?

EURUSD

EURUSD got a reprieve and rose from 1.0685 to 1.0715 after National Party leader Marine LePen said that if she is elected, she would not seek President Emmanuel Macron’s resignation. However, the rest of her party and her potential coalition partners may think differently. EURUSD continues to be undermined by wide French/German bond spreads and last week’s hawkish FOMC rate projections. China is unhappy with Eurozone tariffs on its EV exports and is opening an anti-dumping investigation into EU pork exports.

GBPUSD

GBP is trading poorly and is sitting at the bottom of its 1.2659-1.2691 range, mostly due to EURGBP demand. It is almost a 100% certainty that the BoE will leave rates unchanged on Thursday. In addition, the statement is unlikely to provide much insight due to the pending July 4 election. Prime Minister Rishi Sunak’s decision to call a snap election is proving to be a mistake, if the polls are correct. One pollster said the Conservatives face “electoral extinction,” which is exactly why Canadian Prime Minister Justin Trudeau will hang on to power until the absolute final minute.

USDJPY

USDJPY climbed steadily, rising from 157.17 to 157.70 despite soft US Treasury yields. Traders are cautious ahead of BoJ President Kazuo Ueda’s testimony before parliament on Tuesday. Friday’s announcement that the BoJ would announce bond purchase trimming plans in July didn’t do much for rate hike expectations. Reuters surveyed 29 economists on Monday and only 31% expect a rate hike next month, 20% think it will happen in September, 41% in October and 20% do not see any change until 2025.

AUDUSD and NZDUSD

AUDUSD traded quietly and bearishly in a 0.6592-0.6619 range. Prices were undermined by soft Chinese Industrial Production data which weighed on iron ore prices. Premier Li Qiang’s visit down under is paying dividends. Australians can travel to China visa-free if they get tired of looking at a pair of Giant Pandas, which China is providing to their new BFF.

NZDUSD traded in a 0.6109-0.6141 range due to steady US dollar demand and weak domestic economic data.

USDMXN

USDMXN is in the middle of its 18.4322-18.5441 range with markets continuing to balance the more hawkish than expected FOMC result last week with concerns about Mexican President Claudia Sheinbaum’s proposed political reforms introduced by her predecessor.

BTCUSD (Bitcoin)

BTCUSD is under pressure, trading at the bottom of its 65,936-66,947 range. Last week’s FOMC dot-plot projections of just one rate cut in 2024 are underpinning the greenback and weighing on BTCUSD sentiment. The short-term technicals are bearish below 68,800, looking for a break below 64,600 to extend losses to 61,300.

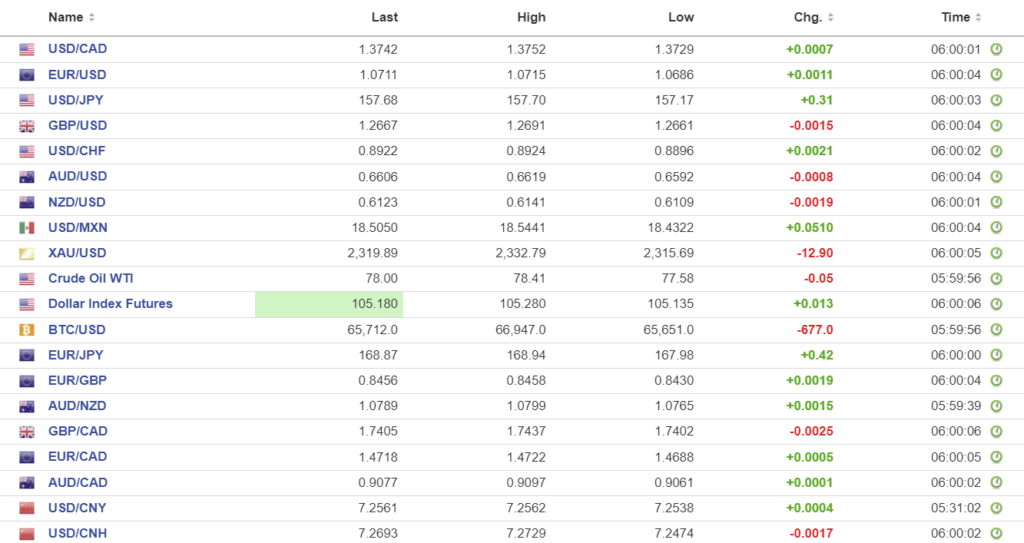

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1149 vs exp. 7.2574 (prev. 7.1151).

Shanghai Shenzhen CSI 300 fell 0.15% to 3536.20

PBoC leaves 1-year Medium-term Lending Facility (MLF) rate unchanged at 2.50%.

May House Price Index -3.9% vs April -3.1%) Industrial Production index 5.6%y/y (forecast 6.0%, April 6.7%) Retail Sales 3.7% y/y (forecast 3.0%, April 2.3%).

Chinese authorities are likely very unhappy that despite a slew of housing support measures, housing prices remained soft.

Chart: USDCNY and USDCNH

Source: Investing.com