June 6, 2024

- No surprise-ECB cuts 25 bps.

- Risk sentiment improves on hopes for early Fed rate cut.

- US dollar trading defensively, opens little changed from close.

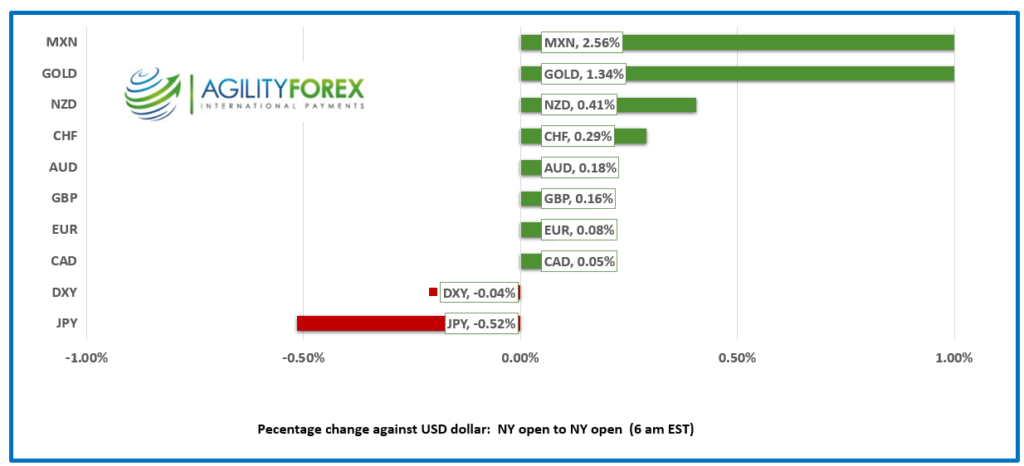

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3687, overnight range 1.3666-1.3698, close 1.3695

USDCAD rallied after the Bank of Canada cut rates, rising from a low of 1.3665 to 1.3743 before reversing the entire move yesterday afternoon and overnight. BoC officials can thank “rate-cut” friendly US data and improved risk sentiment for the USDCAD sell-off.

Scotiabank’s Head of Capital Markets Economics Derek Holt was unimpressed with the BoC decision, blaming Tiff Macklem’s “untrustworthy” forward guidance for his disappointment. He justifies his comment by pointing to a Macklem comment that said, “In the months ahead, we will be closely watching the evolution of core inflation,” and then cuts rates barely one month later.

Unless the Fed comes out and supports the idea of a September rate cut, USDCAD downside is likely limited to 1.3600.

Oil prices traded in a 74.14-74.84 range, torn between improved risk sentiment from Fed rate cut speculation and OPEC’s decision to phase in production increases starting in October.

US initial jobless claims were 229,000 (forecast 220,000) and the US Trade deficit widened but less than expected. Canada’s trade deficit narrowed to $1.05 billion.

USDCAD Technicals

The intraday technicals are bullish above 1.3660 and looking for another attempt for a sustainable break of the downtrend line from mid-April, which comes into play at 1.3720. A topside move would target 1.3790, but another failure suggests a retest of support in the 1.3600 area.

The daily chart technicals are unchanged. The uptrend line at 1.3600 is intact. A decisive move above 1.3720 targets the 1.3775-85 area, while a failure suggests more 1.3600-1.3720 range trading.

For today, USDCAD support is at 1.3650 and 1.3610. Resistance is at 1.3720 and 1.3760. Today’s range is 1.3640-1.3730.

Chart: USDCAD daily

Source: DailyFX

Saving Private Ryan, But Not Many Others

Allied troops stormed the beaches of Normandy 80 years ago today, the first stop in a bloody journey to Berlin. 4,414 soldiers lost their lives while total casualties exceeded 10,000. It was a great victory for General Dwight D. Eisenhower who oversaw the invasion from the comfort of Southwick House, a 19th-century luxury manor in Hampshire, England.

Less is More, More or Less.

Yesterday’s ISM Services PMI and ADP Employment Change reports encouraged September Fed rate cut speculation. The slower ADP employment growth and the slight drop in ISM Services Prices Paid suggest manageable economic expansion and inflation support lower rates.

EURUSD

EURUSD is probing 1.0900 after trading in a 1.0869-1.0896 range which is a rather tepid reaction to the first ECB rate move since raising them on September 20,2023. The new Deposit facility rate is 3.75%, Fixed rate 4.25% and Minimum bid rate is 4.50%, effective from June 12. The analyst reaction is mixed (so far) Deutsche Bank’s Chief European Economist Mark Wall calls it a “hawkish cut” while another analyst from a no-name firm claims “it is not likely to be a single with signals for further cuts this year.” EURUSD did not get any support from April Retail Sales, which fell 0.5% (forecast -0.3%, and March 0.7% m/m).

GBPUSD

GBPUSD gave up early gains while trading in a 1.2775-1.2809 range. Prices were supported by UK Construction PMI, which rose to 54.7 from 53.0 in April, which S&P Global described as “building good momentum” and that firms were gearing up for further growth. The GBPUSD technicals are bullish above 1.2700, with a break above 1.2830 targeting 1.2900.

USDJPY

USDJPY rose from 155.38 in Asia to 156.38 in the European morning before sliding to 155.95 as NY opened. The gains are capped by intervention fears and speculation that the BoJ will soon raise rates while the Fed could be cutting sooner than expected. Yesterday, BoJ Board Member Toyoaki Nakamura said, “It is too soon for a rate hike.” Governor Ueda pointed out that although inflation expectations are rising, they have yet to reach 2.0%.

AUDUSD and NZDUSD

AUDUSD peaked in Asia at 0.6683 then slid to 0.6643 in NY trading after support from the improved trade and building data faded ahead of the ECB meeting and US weekly jobless claims. Australia’s trade surplus widened by $1.707 million in April to $6.548 million.

NZDUSD is trading at the bottom of its 0.6185-0.6215 range with price action tracking AUDUSD moves. NZDUSD is underpinned by forecasts suggesting that the RBNZ will leave rates unchanged until February 2025.

USDMXN

USDMXN is consolidating its post-election gains in a 17.4459-17.5290 range. For the moment, the latest US economic data that raised the odds for the Fed to cut rates in September is overshadowing concerns about economic fallout from the Mexican election.

BTCUSD (Bitcoin)

BTCUSD rose from 70,409 to 71,717 due to the improvement in risk sentiment following yesterday’s ISM data and the surge in the S&P 500 index. BTCUSD is bullish above 68,400 and looking for a break above 72,000 for a retest of the all-time high of 73,794 set on March 13, 2024.

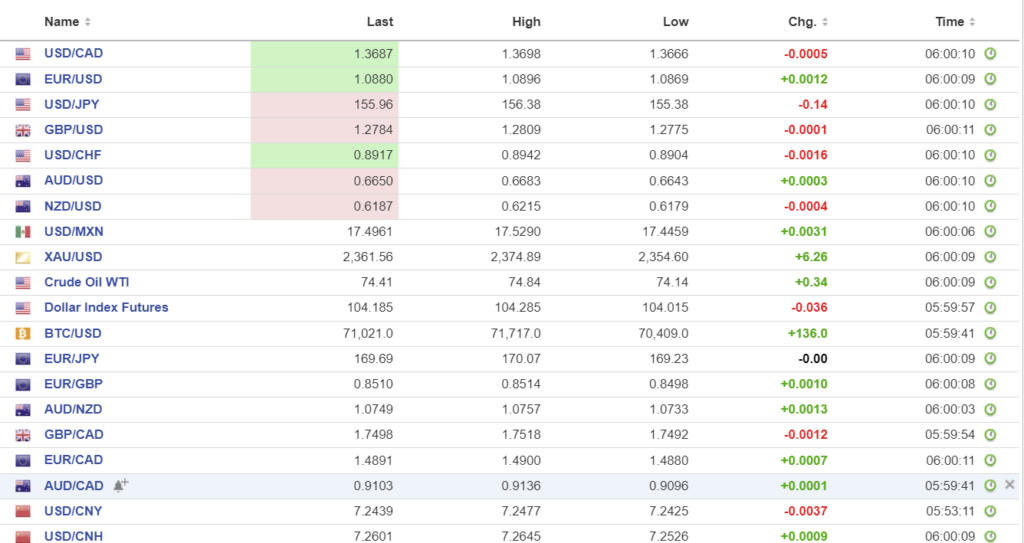

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

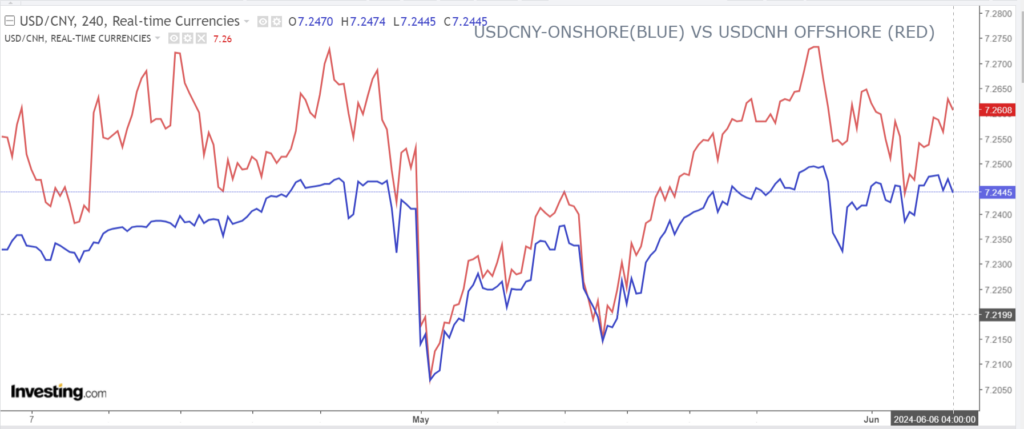

China Snapshot

PBoC fix: 7.1108 vs exp. 7.2436 (prev. 7.1097).

Shanghai Shenzhen CSI 300 fell 0.07% to 3592.28

Bloomberg reports that the shares in China’s property stocks entered a bear market, despite Beijing’s efforts to shore up the sector.

Chart: USDCNY and USDCNH

Source: Investing.com