Image created by DAL-E

November 14, 2023

- Core-CPI rises 4.0% y/y, lower than expected.

- 10-year Treasury yield plunges 16 bps to 4.46%

- US dollar opens mixed , then falls after inflation data.

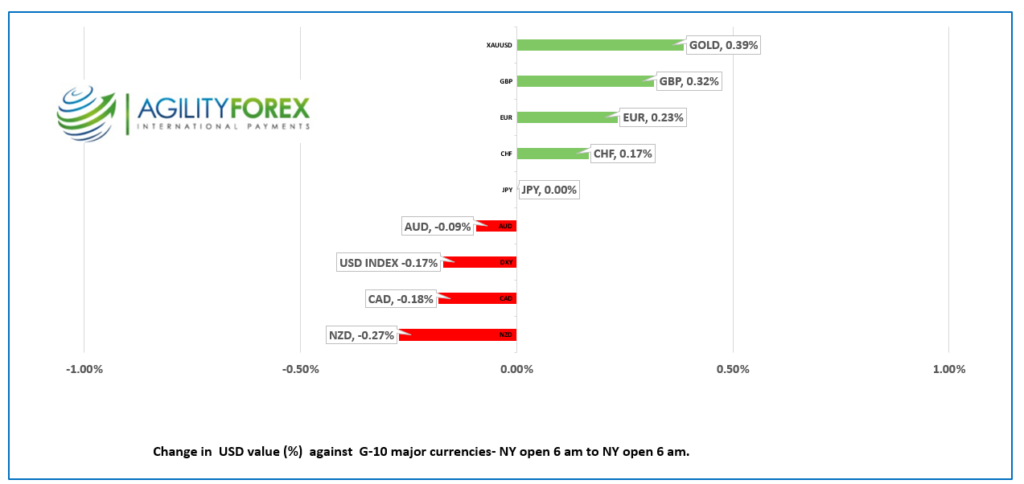

FX at a Glance

Source: IFXA/RP

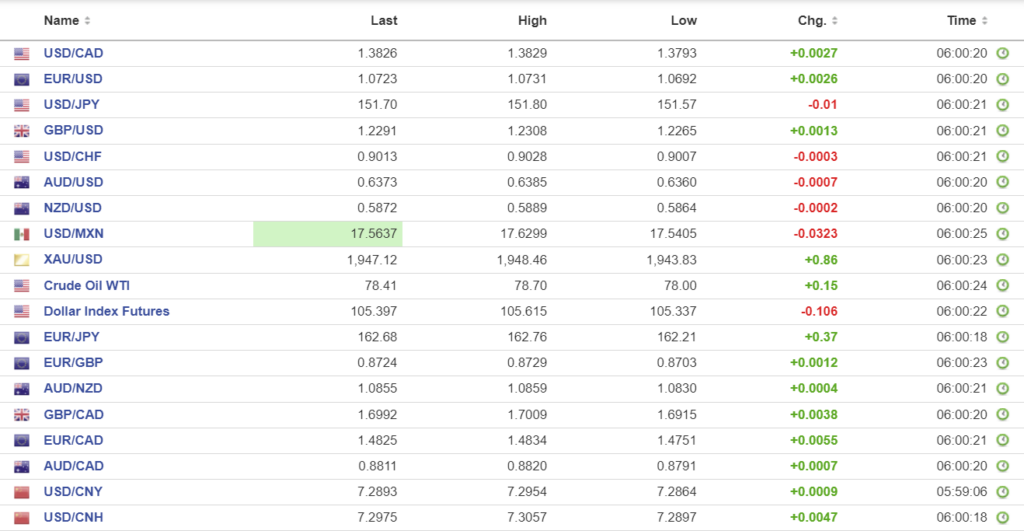

USDCAD Snapshot: open 1.3824-28, overnight range 1.3762-1.3840, close 1.3807

USDCAD started the NY session at the top of its overnight range then promptly fell through the overnight low of 1.3793, reaching 1.3762 in the wake of the US inflation report.

Headline, core, and super-core inflation reads rose less than expected which raised hopes that not only have US interest rates peaked, but rates could be cut as early as May 1, 2024.

Nevertheless, a more important reason for the USDCAD slide is positioning. The latest IMM Commitment of Traders data showed speculators were extremely short CAD (long US dollars), and todays USDCAD drop is due to some of those positions getting cut.

WTI oil prices added to overnight gains and rose from a pre-data low of $77.76/b to $78.83 afterwards. The International Energy Agency (IEA) bumped its forecasts for oil demand growth in 2023 and 2024 higher but warned of near term volatility because of the risk that near-term demand growth is set to slow.

There are no Canadian economic reports today.

USDCAD Technicals:

The intraday technicals flipped to bearish with the break below 1.3790 this morning and are looking for a test of support at 1.3740. If broken, USDCAD could drop to 1.3610. A break above 1.3850 would negate the downside and suggest further gains to 1.4000.

Longer-term, the uptrend from July remains intact above 1.3610.

For today, USDCAD support at 1.3740 and 1.3690. Resistance at 1.3790 and 1.3810. Today’s expected range is 1.3690-1.3790.

Chart: USDCAD hourly.

Source: Investing.com

G-10 FX recap

Today’s lower than expected US inflation data may put economists at UBS and Morgan Stanley in the winners circle. They are predicting that the first of a series of Fed rate cuts will occur beginning at the May 1, 2024, FOMC meeting.

US October CPI rose 3.2% y/y (forecast 3.3%, previous 3.7%) while Core-CPI rose 4.0% (forecast 4.1% y/y) Inflation may be heading in the right direction, but Fed officials have been adamant that rates may need to be restrictive for a prolonged period to get inflation to target. If they stick to that view, then the Goldman Sachs outlook that a rate cut will not happen until November 24 is more likely.

The US dollar plunged on the data. The US dollar index dropped from 105.46 to 104.50, the US 10-year Treasury yield fell to 4.46% from 4.62% and S&P 500 futures soared 1.33%.

Meanwhile, the President Biden/Xi Jinping meeting in San Francisco on Wednesday is providing fodder for those hoping that the two leaders will find a way to improve the deteriorating relationship between Washington and Beijing. No matter what happens, it won’t be a total loss, at least for SF residents. The city is spending a fortune, repaving roads, painting buildings, deep cleaning transit stations, and removing homeless camps that polluted the downtown core for years.

EURUSD spiked to 1.0823 from 1.0727 in the aftermath of the CPI report and has held on to the gains. Earlier, the ZEW Economic Sentiment survey showed economic sentiment in the Eurozone improved sharply in November. (EU ZEW 13.8 vs previous 2.3). The EURUSD intraday technicals are bullish above 1.0760 and looking for a break of 1.0850 to target 1.1000.

GBPUSD popped to 1.2430, post-CPI after drifting in a 1.2265-1.2308 range overnight. Prices saw a bit of support after UK wage growth data slowed less than expected (actual 7.9%, forecast 7.3%) which some analysts suggest will encourage the Bank of England to leave rates unchanged. The intraday GBPUSD technicals are bullish above 1.2340.

USDJPY fell like a stone, dropping to a post-CPI low of 150.58 from an overnight peak of 151.80.

AUDUSD rallied to 0.6467 after trading with a negative bias in a 0.6360-0.6385 overnight. range mainly The weaker than expected Westpac Consumer Sentiment reading (actual 79.9 vs October 82), was blamed on the latest RBA rate hike.

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1768, expected 7.2885, previous 7.1769.

Shanghai Shenzhen CSI 300 rose 0.7% to 3582.06.

Bloomberg reports that Private Equity firms in China are discounting investments by up to 30% as they try to exit the country.

Chart: USDCNY (onshore) vs USDCNH (offshore) 3 months

Source: Investing.com