This week sees announcements on monetary policy by a number of central banks,in particular the Reserve Bank of Australia (Feb 2nd) and the Bank of England (Feb 5th).The beginning of the month also brings the release of Purchasing Managers Index data on key sectors ( manufacturing,construction and services) of the members of the global economy.The first off,was China were manufacturing PMI disappointed at 49.8. Eurozone PMI releases were generally better than expected with the exception of Germany which was reported at 50.9. The week finishes with the release of employment data for January for the US economy.

The biggest mover in the FX space overnight was the Swiss Franc (-1.24%) after reports surfaced that the SNB may be intervening in the market and was targeting the EUR/CHF somewhere rate between 1.05-1.10 This morning will see the release of Personal Consumption Expenditure (PCE) index data, PMI and Personal income and spending & construction data for the US. Canadian RBC PMI data for January is expected at 52.27 ( previous 53.9).The Canadian dollar has benefitted overnight from a strong rally in crude,which at one point was trading through $50 a barrel,currently at $48.89 (+1.66%)

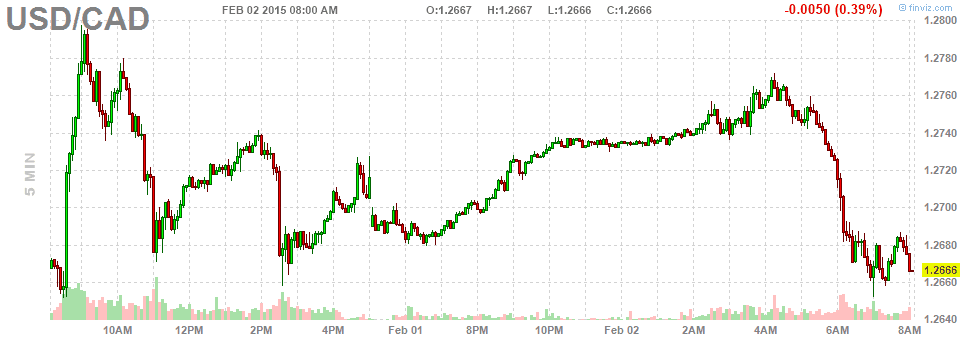

CAD Range 1.2773-1.2654 Currently 1.2683 RES 1.2814 1.2892 SUPP 1.2627 1.2523