May 16, 2024

- Weekly jobless claims higher than expected, lower than last week.

- Falling US Treasury yields weighing on US dollar.

- US dollar consolidating post-CPI losses.

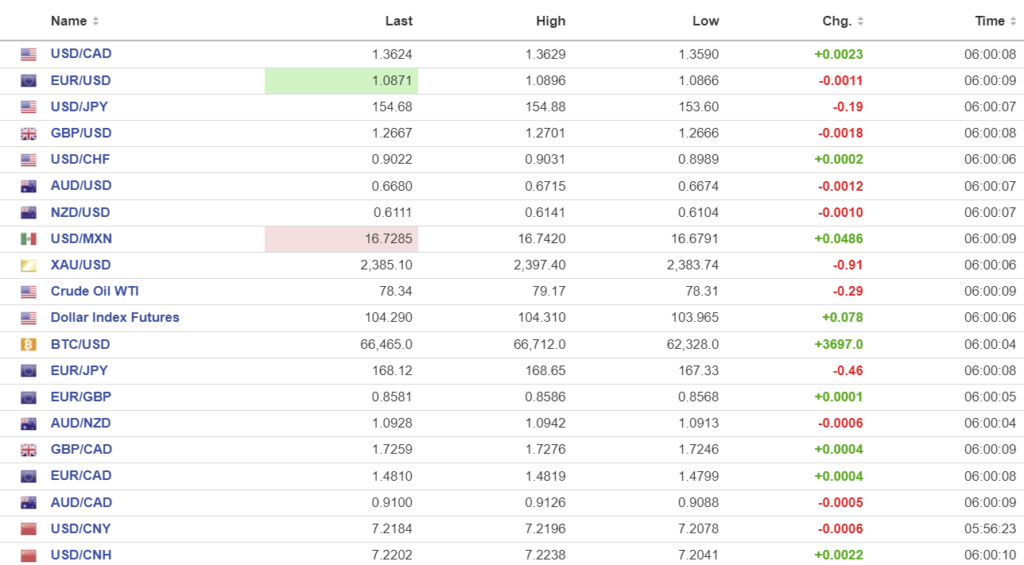

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3624, overnight range 1.3590-1.3635, close 1.3602

USDCAD is consolidating yesterday’s losses. The Canadian dollar started today’s session as the worst performing G-10 currency pair, rising just 0.04% between yesterday’s open and today which pales in the face of the 0.78% gain seen by NZDUSD.

The USDCAD losses were exacerbated by narrowing 10-year CAD/US interest rate differentials which moved from -83.5 last week to -74.2 this morning.

USDCAD downside is contained by technical support and expectations that the Bank of Canada will cut rates in June.

WTI oil prices are rangebound in a 78.20-79.17 range. Support from fears that wildfires in the Fort MacMurray area will disrupt crude shipments are offset by global economic growth concerns. The EIA reported a 2.5 million barrel drop in crude inventories, but that news was lost in the fall-out from the CPI data.

USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3660 and looking to revisit support in the 1.3590 area which was tested yesterday and overnight. A rally above 1.3660 shifts the focus to the 1.3740 level which is the top of the April downtrend channel.

The longer term uptrend line from February is at 1.3550 which is also the bottom of the April downtrend channel and where the 200 day moving average is located.

For today USDCAD support is at 1.3590 and 1.3560. Resistance is at 1.3660 and 1.3690. Today’s range is 1.3580-1.3680.

Chart: USDCAD 4 hour

Source: DailyFX

US data suggests economy is slowing

Markets were hoping for an upward surprise to weekly jobless claims but although claims rose by 2,000 above the forecast of 220,00 it was well below last weeks 232,000 increase. It would be a mistake to get overly excited about the impact of this data on the outlook for Fed rates.

April Housing Starts were lower than forecast but 5.7% higher than last month. Building permits fell 3% and the Philadelphia Manufacturing Survey showed activity in the region weakening.

FOMC policymakers Cleveland Fed President Loretta Mester, Atlanta Fed President Raphael Bostic and Vice Chair Barr, may shed some light on how the data affects their interest rate view, today.

Equity rally pauses

Asian equity indexes followed Wall Street’s lead and closed with big gains. Australia’s ASX 200 rallied 1.65% while Japan’s Nikkei 225 index gained 1.39%. Hong Kong’s Hang Seng climbed 1.59%, supported by talk of government support for property developers. European bourses are trading negatively. The French CAC 40 is down 0.45% and the UK FTSE 100 index is down 0.28%. S&P 500 futures are flat. The US 10-year Treasury yield is 4.338%.

EURUSD

EURUSD consolidated Wednesday’s rally in a 1.0866-1.0896 range and could rally further if US jobless claims rise more than expected. The ECB Financial Stability Review stated the obvious—that geopolitical tensions were a significant source of risk. It also said that “The near-term risk of a deep recession accompanied by rising unemployment – a major source of concern six months ago – is much lower from today’s perspective, and disinflation has proceeded in parallel.”

GBPUSD

GBPUSD gave up early gains and traded in a 1.2654-1.2701 range. Prices are supported by renewed optimism for US rate cuts earlier than expected which makes the prospect of a June Bank of England rate cut less of a negative for GBPUSD.

USDJPY

USDJPY chopped about in a 153.60-155.22 range and is close to the top of that band in NY trading the fall-out from Wednesday’s post-CPI data fades. The US 10-year yield dropped from 4.424% at yesterday’s NY open to 4.313% overnight then climbed to 4.344% in NY. Japan’s economy shrank 0.5% q/q in Q1 compared to 0.1% previously.

AUDUSD AND NZDUSD

AUDUSD rallied from 0.6674 to 0.6714 in the fall-out from Wednesday’s US CPI report the dropped to 0.6665 in NY. The currency saw some support on news that Australia gained 38,500 jobs in April (forecast 23,700). The unemployment rate rose to 4.0% from 3.9%.

NZDUSD traded in a 0.6101-0.6141 range overnight. Traders are looking ahead to Wednesday’s RBNZ meeting although it is not expected to be very exciting as officials will leave rates and monetary policy unchanged.

USDMXN

USDMXN drifted higher in a 16.6791-16.7420 range as the euphoria over the modest improvement in US inflation data faded. Hawkish comments from non-voting FOMC member Neel Kashkari helped to underpin prices as are concerns that Banxico may cut rates again in June.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

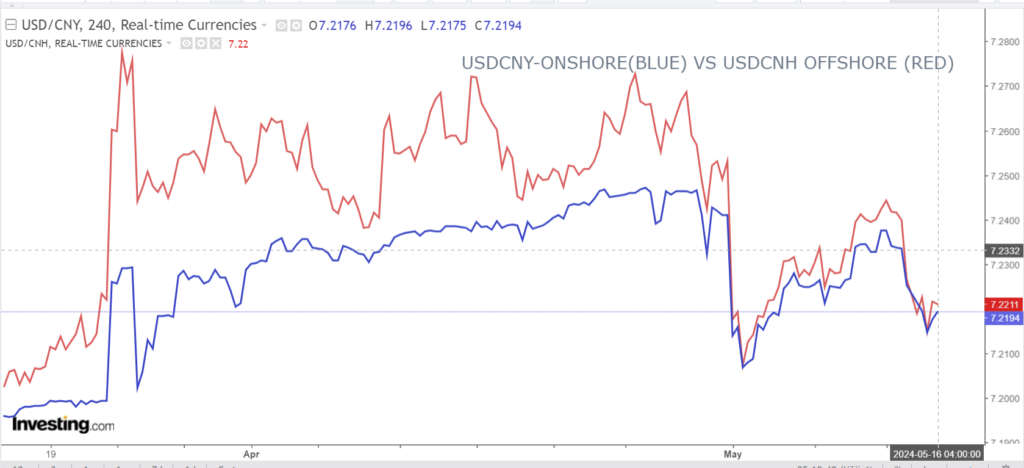

China Snapshot

PBoC fix: 7.1020 (forecast 7.2017) prev. 7.1049.

Shanghai Shenzhen CSI 300 rose 0.39% to 3640.36.

Property developer shares rise on reports that Chinese authorities were discussing buying unsold houses to ease the property crisis.

Chart: USDCNY and USDCNH

Source: Investing.com